UWM Holdings' $1 Billion Senior Notes Offering and Its Strategic Implications for Growth

UWM Holdings' recent $1 billion senior notes offering—upsized from an initial $600 million—represents a calculated move to optimize its capital structure and fortify its position in a challenging mortgage market. The 6.250% senior notes due 2031, priced at par and guaranteed by its wholly owned subsidiary United Wholesale Mortgage, will be used to refinance maturing 5.5% senior notes in November 2025, reduce borrowings under its mortgage servicing rights (MSR) facilities, and fund working capital needs [1]. This refinancing strategy, coupled with the company's robust Q2 2025 performance, underscores a strategic pivot to navigate a rising-rate environment while maintaining growth momentum.

Capital Structure Optimization: Balancing Leverage and Stability

UWM's decision to extend debt maturities to 2031 reflects a deliberate effort to align its liabilities with long-term asset durations, a critical consideration in a market where short-term refinancing risks have intensified. By replacing the 5.5% notes due in late 2025 with longer-dated, higher-yielding debt, the company secures a more stable funding profile. However, this comes at the cost of increased leverage: its non-funding debt-to-equity ratio rose to 1.90 as of June 30, 2025, from 0.91 a year earlier [1]. While this elevation in leverage may raise eyebrows, it is offset by the company's $2.2 billion in available liquidity, including $490 million in cash and borrowing capacity under secured and unsecured credit lines [1]. This liquidity buffer provides flexibility to manage near-term obligations or pursue strategic opportunities without overexposing the balance sheet.

The offering also highlights UWM's ability to access capital at competitive rates despite its elevated leverage. The 6.25% coupon, while higher than the 5.5% on the maturing notes, reflects broader market conditions where borrowing costs have risen in response to Federal Reserve tightening. Yet, the fact that the offering was upsized to $1 billion—from $600 million initially—demonstrates strong investor demand, suggesting confidence in UWM's operational resilience and growth trajectory [1].

Market Positioning in a Rising-Rate Environment

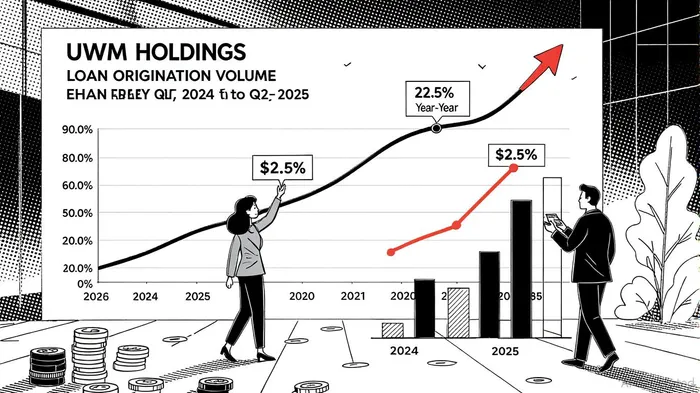

UWM's strategic initiatives have positioned it to thrive even as mortgage rates climb. In Q2 2025, the company reported a 22.5% year-over-year increase in loan origination volume, reaching $39.7 billion [2]. This growth is driven by its aggressive adoption of AI-powered tools such as the LE Optimizer (LEO) and the virtual assistant “Mia,” which streamline underwriting processes and enhance borrower engagement. These innovations not only reduce operational costs but also enable UWMUWMC-- to maintain its dominance in the wholesale mortgage channel, where speed and efficiency are paramount [2].

The rising-rate environment, while challenging for mortgage lenders due to reduced refinancing activity, has paradoxically benefited UWM by compressing competition. As smaller players struggle with margin pressures, UWM's scale and technological edge allow it to capture market share. The proceeds from the senior notes offering will further bolster this advantage by reducing reliance on short-term financing and freeing up capital for innovation.

Strategic Flexibility and Long-Term Growth

With $2.2 billion in liquidity, UWM is well-positioned to navigate near-term uncertainties. The company can use its financial flexibility to reinvest in technology, expand its wholesale network, or explore strategic acquisitions. Notably, its Q2 2025 net income of $314.5 million [2] provides a strong foundation for such initiatives. The extended maturity of the new debt also insulates the company from immediate refinancing pressures, allowing it to focus on long-term value creation.

However, investors should remain cautious about the trade-offs inherent in UWM's leveraged approach. While the debt-to-equity ratio of 1.90 is manageable given its liquidity, any further rate hikes or economic downturns could strain cash flows. The company's reliance on technology to drive efficiency will be critical in mitigating these risks.

Conclusion

UWM Holdings' $1 billion senior notes offering is a masterstroke in capital structure optimization, balancing the need for long-term stability with the flexibility to invest in growth. By refinancing short-term debt, leveraging its liquidity, and deploying cutting-edge tools, UWM is not only weathering the current rising-rate environment but also positioning itself to outperform in a post-hike landscape. For investors, the key takeaway is clear: UWM's strategic agility and financial discipline make it a compelling play in the evolving mortgage market, albeit with a watchful eye on leverage management.

Comentarios

Aún no hay comentarios