Unlocking Non-Traditional Income: Analyzing Nuveen Churchill Direct Lending's Strategy in a Low-Yield Environment

In an era where traditional fixed-income assets struggle to deliver meaningful returns, investors are increasingly turning to alternative strategies to unlock non-traditional income. Nuveen Churchill Direct LendingNCDL-- Corp. (NCDL) stands out as a compelling case study in this pursuit. By leveraging its expertise in private credit and a disciplined approach to middle-market lending, NCDLNCDL-- has positioned itself to generate attractive risk-adjusted returns despite the challenges of a low-yield environment.

A Strategic Focus on Senior Secured Loans

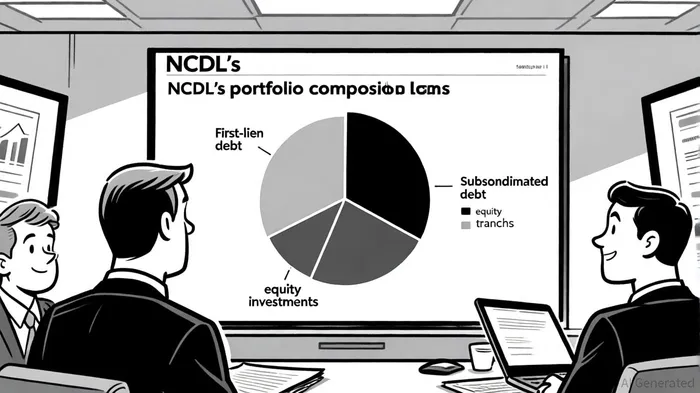

NCDL's investment strategy centers on providing senior secured loans to private equity–owned U.S. middle-market companies. According to NCDL's first-quarter 2025 results, as of March 31, 2025, approximately 90.5% of NCDL's portfolio was allocated to first-lien debt, with 7.8% in subordinated debt and 1.7% in equity investments. This structure prioritizes downside protection while still capturing upside potential through subordinated and equity tranches.

The company's partnership with Churchill Asset Management-a division of Nuveen and TIAA-further enhances its competitive edge. Churchill's deep expertise in underwriting and sourcing deals allows NCDL to access a pipeline of high-quality opportunities that are often overlooked by larger institutional players. This specialization is critical in a low-yield environment, where incremental returns depend on identifying undervalued assets and managing credit risk effectively.

Diversification as a Risk Mitigator

NCDL's portfolio is highly diversified, spanning 210 portfolio companies across 26 industries, with an average position size of just 0.5%, according to the same press release. This fragmentation reduces concentration risk and ensures that no single investment can significantly impact the overall portfolio. The weighted average internal risk rating of 4.1 (on a scale where lower numbers indicate higher risk) underscores the company's conservative underwriting standards.

However, diversification alone is not enough. NCDL's ability to optimize its capital structure has been a key driver of performance. In the first quarter of 2025, the company issued $300 million in unsecured notes and refinanced a collateralized loan obligation (CLO), reducing borrowing costs and extending maturities, as noted in its Q1 results. These actions highlight NCDL's proactive approach to managing liquidity and interest rate sensitivity-a critical advantage in a tightening credit market.

Performance in a Challenging Yield Landscape

Despite its strategic advantages, NCDL faces headwinds. The weighted average yield of its debt and income-producing investments fell to 10.10% in Q1 2025, down from 11.55% a year earlier, the press release reported. This decline reflects tighter spreads on new investments and the drag from falling base interest rates. Yet, the company has maintained a consistent distribution of $0.45 per share, supported by a net investment income of $0.53 per share in the same period.

The resilience of NCDL's income stream is partly attributable to its disciplined capital allocation. By focusing on first-lien debt-where recovery rates in default scenarios are typically higher-the company minimizes the risk of income disruption. As of March 31, 2025, only two portfolio companies were on non-accrual status, representing a mere 0.4% of the total portfolio, which reinforces the robustness of NCDL's underwriting process.

The Path Forward

Looking ahead, NCDL's ability to adapt to evolving market conditions will be crucial. The company has signaled its intent to leverage Churchill's sourcing model and scale to identify new opportunities, particularly in sectors where private credit demand is surging. Additionally, its flexibility to access junior capital and private equity co-investments provides a buffer against potential liquidity constraints, according to the Q1 disclosure.

For income-focused investors, NCDL offers a unique blend of yield, diversification, and risk management. While the broader fixed-income market remains constrained by low rates, NCDL's focus on middle-market direct lending provides a pathway to non-traditional income without sacrificing capital preservation.

Comentarios

Aún no hay comentarios