Unlocking Long-Term Value in Healthcare Real Estate: A Closer Look at Medical Properties Trust's Strategic Resilience

The healthcare real estate sector has long been a barometer for economic resilience, and Medical Properties TrustMPW-- (MPW) offers a case study in navigating turbulence while positioning for long-term value creation. According to MPW's Q2 results, the company faced a challenging second quarter of 2025 marked by a net loss of ($0.16) per share and impairment charges totaling $111 million, yet its strategic moves-including a €702.5 million 10-year loan at a 5.1% fixed rate-underscore its commitment to stabilizing its balance sheet and capitalizing on the sector's enduring demand.

Financial Performance: Navigating Impairments and Growth

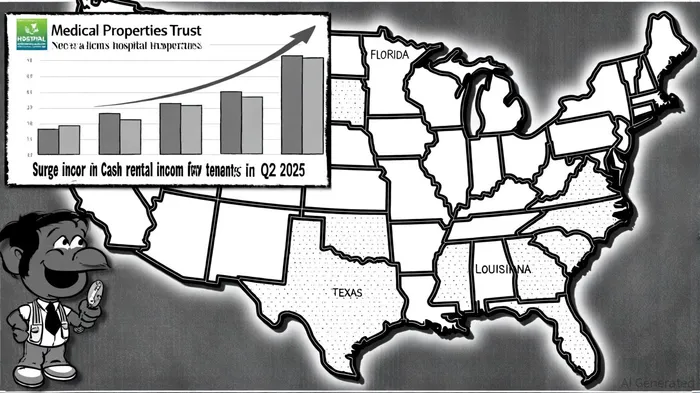

MPW's Q2 2025 results reflect the dual pressures of legacy liabilities and forward-looking investments. The $111 million in impairment charges, tied to the sale of PHP Holdings and Prospect Medical Group bankruptcy transactions, masked a critical positive: cash rental income from new tenants surged to $11 million in Q2, up from $3.4 million in Q1. This trend suggests progress in re-tenanting underperforming assets, a strategy that could drive annualized pro rata cash rent above $1 billion by 2026.

However, the company's broader financial health remains fragile. MarketBeat's financials show a 2024 net loss of ($4.02) per share, and a debt-to-equity ratio of 2.00 is highlighted by StockAnalysis ratios, which underscores structural risks. Yet, the recent 10-year non-amortizing loan-a rare feat in today's high-interest environment-demonstrates investor confidence in the sector's fundamentals. As stated by MPW's management, "The hospital real estate sector remains a critical component of healthcare infrastructure, and our ability to secure long-term, fixed-rate financing positions us to weather near-term volatility."

Dividend Sustainability: A Balancing Act

MPW's dividend cuts-most notably a 73% reduction in Q2 2025-have raised questions about its ability to reward shareholders. The Q1 2025 payout ratio of 266.67% was unsustainable, but normalized and adjusted funds from operations (AFFO) metrics show more manageable ratios of 57.14% and 44.44%, respectively. This discrepancy suggests that while the dividend is currently constrained by short-term accounting headwinds, the underlying cash flow generation remains intact.

The key to restoring dividend credibility lies in MPW's re-tenanting strategy. The 29% increase in interest expenses from a $2.5 billion secured notes issuance is a near-term drag, but the $17 million in scheduled third-quarter collections indicates momentum. If this trend continues, the company could reduce its payout ratio to a more sustainable range by mid-2026.

Portfolio Strength and Sector Positioning

MPW's portfolio of 392 properties and 39,000 licensed beds spans nine countries, with a strong focus on U.S. inpatient rehabilitation facilities. These assets are benefiting from a structural shift in healthcare demand: rising surgical volumes and an aging population. Three tenants, including HonorHealth and College Health, are already self-funding capital spending, signaling improved operator stability.

The company's geographic diversification also provides a buffer. While billed rent declined 3% year-to-date, collections in Florida, Texas, and Louisiana remained robust, reflecting the resilience of essential healthcare services. As one analyst noted, "MPW's ability to secure rent from replacement operators in high-demand regions is a testament to the inelasticity of hospital real estate."

The Path Forward: Risks and Opportunities

MPW's long-term value proposition hinges on its ability to execute its re-tenanting strategy while managing debt. The $2.5 billion secured notes issuance has increased interest burdens, but the 5.1% fixed rate on its recent European loan provides a model for future financing. Investors should monitor the company's progress toward $1 billion in annualized cash rent by 2026, a target that could justify a re-rating of its stock.

Risks remain, including further impairments and regulatory shifts in healthcare delivery. Yet, the sector's structural tailwinds-aging demographics, rising healthcare costs, and the need for specialized infrastructure-suggest that MPW's challenges are not unique but rather part of a broader industry recalibration.

Conclusion

Medical Properties Trust is at a crossroads. Its recent financial struggles are undeniable, but the company's strategic focus on re-tenanting, long-term financing, and geographic diversification positions it to unlock value in a sector that remains critical to the U.S. economy. For investors with a multi-year horizon, MPW's discounted valuation and asset-heavy model could offer compelling upside-if management can stabilize operations and restore confidence in its dividend.

Comentarios

Aún no hay comentarios