Unlocking Hidden Gold: How Slowing U.S. Home Prices Signal the Best Real Estate Opportunities of 2025

The U.S. housing market is undergoing a seismic shift. After years of frenzied price growth, a slowdown in 2025 has created a landscape of stark regional disparities—and rare opportunities for investors who act decisively. While national price appreciation has cooled to a meager 1.2% in Q2 (down from 3.4% in Q1), this isn’t a universal slump. Instead, it’s a buyer’s market in select submarkets where strategic investors can secure undervalued assets poised for recovery.

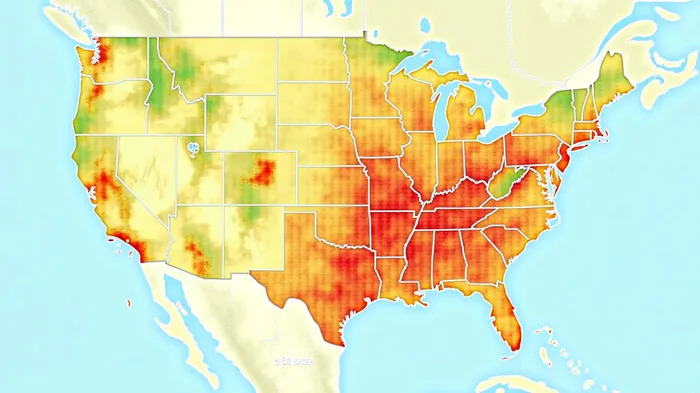

Regional Divergence: Where to Buy—and Where to Flee

The slowdown isn’t uniform. Northeast and Midwest markets—such as Boston, Lincoln, Nebraska, and parts of Cheshire—remain bright spots, with prices growing 3–4% annually despite high mortgage rates. These regions thrive on constrained inventory, strong job markets, and demand for quality education-driven neighborhoods.

Meanwhile, the Sunbelt and South face a reckoning. Cities like Denver, Miami, and Phoenix have seen price growth plummet to near-zero or even negative territory. Denver’s prices dropped to a 0.5% annual increase in Q2, down from 5% in Q1, while Miami’s prices fell 0.5%—their first decline since 2020. The culprit? Overbuilding and affordability shocks.

- Key Data:

- Inventory Crisis: The South’s housing starts dropped 14.2% month-over-month in March, yet existing inventory remains 20% above pre-pandemic levels.

This divergence means investors should avoid Sunbelt exurbs but pounce on Northeast and Midwest opportunities—especially in fixer-flipper properties and multifamily units in supply-constrained areas.

Interest Rates: The Double-Edged Sword

Mortgage rates averaging 7.2% in Q2 (up from 6.1% in Q1) have crimped demand, but they also clear the field for informed buyers. The “lock-in effect”—where 80% of homeowners are “out-of-the-money” on their mortgages—has frozen inventory, creating scarcity in prime markets.

- Action Item: Focus on markets where price corrections outpace rate hikes. For instance, coastal Florida homes now trade at 12.8% below their 2022 peaks, offering discounts that offset high borrowing costs.

Rental Demand: The Multifamily Play

While single-family homes struggle in overbuilt regions, multifamily housing is a stealthy growth engine. Rents in urban centers like Boston and Denver have risen 8% annually, driven by resilient office demand and a shift back to cities post-pandemic.

- Why It Works: Multifamily assets in job-rich hubs (e.g., tech corridors in Boston’s Route 128) offer steady cash flows.

- Risk Mitigation: Avoid speculative developments in Sunbelt suburbs. Target stabilized markets with 10+ year occupancy trends.

Fixer-Flippers: The Undervalued Gold Mine

In undervalued regions like Tampa, Florida, or Riverside, California, distressed homes—often priced 15–20% below market—present a renovation arbitrage opportunity. These properties can be flipped for 10–15% profits post-upgrades, especially in areas with improving job markets.

- Tip: Prioritize neighborhoods with strong school districts or walkability, as these factors drive post-recovery demand.

Why Act Now?

The window is narrow. The Federal Reserve’s May 2025 policy signals suggest rates could rise further to 7.85% by year-end, but even a small dip to 6.5% could ignite demand. Investors who move now can secure assets at discounted prices before the following trends reverse:

1. Inventory Correction: Overbuilt regions may stabilize by late 2025, narrowing price gaps.

2. Policy Shifts: Zoning reforms and federal land-use changes could unlock supply in constrained markets, pushing prices upward.

Your Playbook for 2025

- Buy in Resilient Markets: NortheastNECB-- and Midwest metros with constrained inventory (e.g., Boston, Lincoln, NE).

- Target Multifamily in Urban Cores: Focus on markets with rising office occupancy and tech job growth.

- Flip in Undervalued Sunbelt Areas: Renovate distressed homes in regions with underlying demand (e.g., Florida’s interior cities).

- Avoid Overbuilt Regions: Steer clear of coastal South Florida and Texas exurbs until inventory clears.

Conclusion: The Slowdown Is the Setup

The 2025 housing slowdown isn’t an end—it’s a reset. For investors who analyze regional disparities, capitalize on interest-rate volatility, and seize undervalued assets now, this is the best chance in a decade to build long-term wealth. Act swiftly, or risk missing the next wave of recovery.

The market is speaking. Are you listening?

Comentarios

Aún no hay comentarios