United Natural Foods Inc: A Bullish Outlook Amid Sector Transformation and Strategic Reinvention

The recent analyst activity surrounding United Natural FoodsUNFI-- Inc. (UNFI) reflects a compelling convergence of sector dynamics and corporate reinvention. Following a series of upgrades and target price increases in early 2025, the stock now commands a 22.01% average upside from its current price, according to analyst estimates. This optimism is not merely speculative but rooted in a transformation of the natural foods industry and UNFI's strategic recalibration to capitalize on it.

Sector Positioning: A Landscape of Disruption and Opportunity

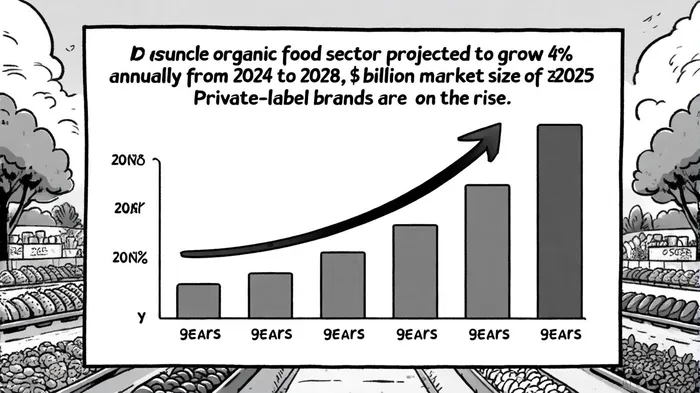

The natural foods sector is undergoing a tectonic shift, driven by three interlinked trends. First, retail media networks are accelerating, with digital engagement projected to grow at over 24% annually through 2028, as highlighted in UNFI's top trends. This shift is reshaping how brands connect with consumers, favoring companies with robust digital infrastructure-a domain where UNFI's recent technology investments position it strongly. Second, private-label brands are surging, with sales expected to expand 40% over six years, according to that UNFIUNFI-- briefing. UNFI's role as a supplier to retailers seeking cost-effective, high-quality private-label options amplifies its relevance. Third, fresh and functional foods are outpacing traditional grocery categories, driven by health-conscious consumers, a trend also detailed in the UNFI briefing. UNFI's 9.2% sales growth in its Natural segment in fiscal 2025 underscores its alignment with these trends, per the Panabee analysis.

Strategic Reinvention: From Cost-Cutting to Growth Leverage

UNFI's fiscal 2025 results highlight a disciplined approach to restructuring. The company exited a $1 billion supply agreement in the Northeast, incurring $53 million in termination charges but securing long-term efficiency gains, as noted in the Panabee analysis. This move, coupled with $94 million in restructuring costs, reflects a willingness to prioritize sustainable margins over short-term pain. Debt reduction is another cornerstone: net debt fell to $1.86 billion, the lowest since 2018, supported by an 86% surge in operating cash flow to $470 million, according to the Panabee analysis.

Beyond cost discipline, UNFI is investing in technology modernization, including AI-driven demand forecasting and a new supply chain management system. These initiatives are part of its "Refresh" strategy, which aims to enhance customer service and operational agility. The implementation of Symbotic's AI-powered robotics and software automation at five distribution centers is detailed in UNFI's fourth-quarter results and is expected to boost efficiency and order accuracy. Additionally, the expansion of food rescue and recovery efforts with Too Good To Go has enhanced UNFI's ESG credentials, as described in the UNFI briefing. The company's 58-distribution-center network and 275,000+ SKUs further solidify its role as a one-stop solution for retailers, particularly as competitors struggle with fragmented supply chains (per the Panabee analysis).

Competitive Advantages and Risks

UNFI's customer retention rate of 95%+ and its deep relationship with Whole Foods (its anchor customer) provide a stable revenue base, according to the Panabee analysis. However, the fourth-quarter cybersecurity incident-a $400 million sales hit and $50 million EBITDA drag-exposes vulnerabilities in its digital infrastructure. While the company has since bolstered cybersecurity measures, such risks remain a wildcard.

The sector's competitive landscape is also evolving. Challenger brands, growing at 27% annually, are forcing incumbents to innovate (Panabee). UNFI's focus on differentiation through product innovation and supply chain solutions, as outlined in the UNFI briefing, positions it to retain market share, but execution will be critical.

Investment Implications

The analyst consensus leans bullish, with BMO Capital's $48 target (an 117% upside) and CL King's "Buy" rating reflecting confidence in UNFI's turnaround. However, Deutsche Bank's $24 target and Zacks' recent "Strong-Buy" upgrade highlight divergent views on the pace of recovery.

For investors, the key question is whether UNFI can sustain its momentum. The company's fiscal 2026 guidance-low-single-digit sales growth and low-double-digit EBITDA growth-suggests a measured approach, prioritizing margin expansion over aggressive top-line bets (UNFI briefing). Given the sector's $232 billion market size by 2025 and UNFI's structural advantages, the stock appears undervalued relative to its long-term growth potential.

Notably, UNFI's earnings performance since 2022 has shown resilience. Earnings per share (EPS) accelerated to $1.16 in Q1 2023, a 19.6% year-over-year increase, while revenue reached $7.47 billion, up 6.7% year-over-year, based on the Q1 2023 earnings. The company has also demonstrated a strong track record of beating estimates, with a 75% success rate for EPS and a 38% success rate for revenue over the past two years, as reported in the Q1 2023 earnings data. These results underscore the effectiveness of its strategic initiatives, including AI-driven supply chain improvements noted in the fourth-quarter results and ESG-focused innovations from the UNFI briefing.

Conclusion

United Natural Foods stands at an inflection point. Its strategic pivot-from debt reduction to technology investment-aligns with the natural foods sector's evolution toward digital engagement, private-label dominance, and fresh/functional offerings. While risks persist, the recent analyst upgrades and sector trends suggest that UNFI's challenges are being addressed with the rigor required to unlock value. For investors with a medium-term horizon, the stock offers a compelling case of transformational potential in a high-growth industry.

Comentarios

Aún no hay comentarios