The Uneven U.S. Consumer Recovery and Its Implications for Retail and Consumer Discretionary Sectors

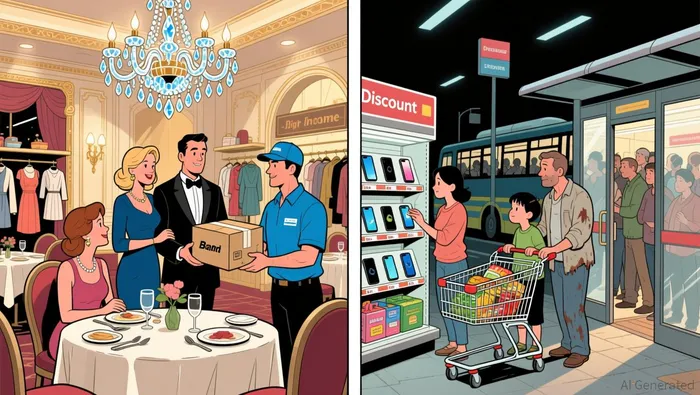

The U.S. consumer recovery post-pandemic has been anything but uniform. While high-income households have maintained robust spending power, lower- and middle-income consumers continue to grapple with inflationary pressures and tighter budgets. This divergence has created a fragmented landscape for the retail and consumer discretionary sectors, forcing businesses to adapt to shifting preferences and income-based spending dynamics. For investors, understanding these trends is critical to identifying opportunities and risks in a market where resilience and vulnerability coexist.

Income-Based Spending Dynamics: A Tale of Two Consumers

High-income households have emerged as the backbone of U.S. consumer spending, accounting for approximately 57% of total consumption from 2020 to mid-2025. Their financial resilience-bolstered by higher disposable incomes and asset returns-has shielded them from the full brunt of inflation and labor market volatility. In contrast, lower- and middle-income consumers have faced disproportionate challenges, particularly in essential categories like food and healthcare, and housing. By late 2025, 75% of consumers reported trading down in at least one spending category, yet splurging persisted among high-income individuals and Gen Z, with 76% of the latter group planning discretionary purchases. This duality reflects the "lipstick effect," where small indulgences-such as beauty, fashion, and dining-become priorities during economic uncertainty.

Notably, generational preferences are reshaping spending patterns. Gen Z's inclination toward fashion and dining contrasts with Boomers' focus on travel, while high-income millennials have driven "revenge spending" on experiences like concerts and dining. These trends underscore the need for retailers to segment their strategies by income and age, rather than adopting a one-size-fits-all approach.

Retailers are responding to these fragmented dynamics with targeted strategies. Gen Z, a key growth driver for clothing and fashion brands, has become a focal point for personalized marketing and omnichannel integration. Retailers are leveraging data analytics to track behaviors such as early-morning shopping windows and omnichannel spending patterns. Meanwhile, AI-powered tools are revolutionizing operations: demand forecasting, inventory management, and customer engagement have improved efficiency, with some retailers reporting 250% growth in sales and profit from AI-driven initiatives.

Retailers are responding to these fragmented dynamics with targeted strategies. Gen Z, a key growth driver for clothing and fashion brands, has become a focal point for personalized marketing and omnichannel integration. Retailers are leveraging data analytics to track behaviors such as early-morning shopping windows and omnichannel spending patterns. Meanwhile, AI-powered tools are revolutionizing operations: demand forecasting, inventory management, and customer engagement have improved efficiency, with some retailers reporting 250% growth in sales and profit from AI-driven initiatives.

Price sensitivity remains a dominant theme, with 75% of consumers trading down in 2025. To address this, retailers are offering early bird deals, flexible payment options, and loyalty programs. For example, JPMorgan notes that Gen Z's preference for integrated online and in-store experiences has spurred investments in BOPIS (Buy Online, Pick Up In Store) and curbside services. These innovations not only cater to convenience-driven consumers but also mitigate the erosion of brand loyalty, as 39% of Gen Z and millennials have abandoned traditional brands in favor of value-aligned alternatives.

Consumer Discretionary Sector: E-Commerce and the Rise of the Solo Economy

The consumer discretionary sector has undergone a permanent digital transformation, with over 90% of U.S. and Chinese consumers engaging in online shopping monthly. This shift is driven by a desire for convenience and speed, exemplified by the 40% of U.S., U.K., and German consumers using grocery delivery weekly. The sector's evolution also reflects a broader "solo economy," where consumers spend more time on self-directed activities like fitness, hobbies, and social media.

However, the sector faces headwinds. The housing market remains a drag, with existing home sales declining in the first half of 2025 due to high mortgage rates. Conversely, travel and dining have rebounded strongly, particularly among high-income demographics. For investors, this duality highlights the importance of sector diversification: while home-related categories face challenges, experience-driven industries like hospitality and entertainment are poised for growth.

Investment Implications: Navigating the Fragmented Landscape

For investors, the uneven recovery underscores the need to prioritize companies that can navigate income-based spending dynamics and technological shifts. Retailers with strong AI and data analytics capabilities-such as those leveraging generative AI for demand forecasting-are well-positioned to capitalize on evolving consumer behaviors. Similarly, e-commerce platforms and omnichannel retailers that cater to Gen Z and millennials' preference for convenience and personalization offer long-term growth potential.

Conversely, sectors reliant on lower-income consumers-such as housing and certain retail categories-remain vulnerable to inflationary pressures and wage stagnation. Investors should also monitor the stock market's influence on consumer spending, as real PCE growth in late 2025 aligned closely with asset price movements.

Conclusion

The U.S. consumer recovery is a mosaic of resilience and fragility, shaped by income disparities and generational preferences. Retailers and consumer discretionary firms that adapt through personalization, technology, and agility will thrive in this fragmented environment. For investors, the key lies in identifying companies that not only respond to current trends but also anticipate the next wave of consumer behavior. As the market continues to evolve, those who align with the rhythms of the "uneven recovery" will find themselves at the forefront of growth.

Comentarios

Aún no hay comentarios