ULTY's NAV Decay: A Structural Crisis in High-Yield ETF Design

The YieldMax Ultra Option Income Strategy ETF (ULTY) has long been marketed as a high-yield haven for income-starved investors. With a distribution rate exceeding 80% and a recent weekly payout of $0.0926 per share (implying an 85.60% annualized yield), it's no surprise that the fund has attracted attention. However, beneath the glitter of these payouts lies a structural crisis: persistent net asset value (NAV) decay driven by a combination of aggressive payout strategies, high fees, and volatile asset allocation.

The Illusion of Income: Return of Capital and NAV Erosion

ULTY's distributions are not what they seem. While the fund's 85.60% yield appears enticing, a significant portion—such as the 12.82% return of capital in the August 2025 payout—directly erodes the fund's NAV [1]. This practice, while legally permissible, effectively returns investors' own principal as income, creating a false sense of sustainability. As stated by a report from Making Cents Sense, “ULTY's yield is not indicative of total return. The fund's aggressive payout strategy includes return of capital, which reduces the NAV and may result in principal loss over time” [2].

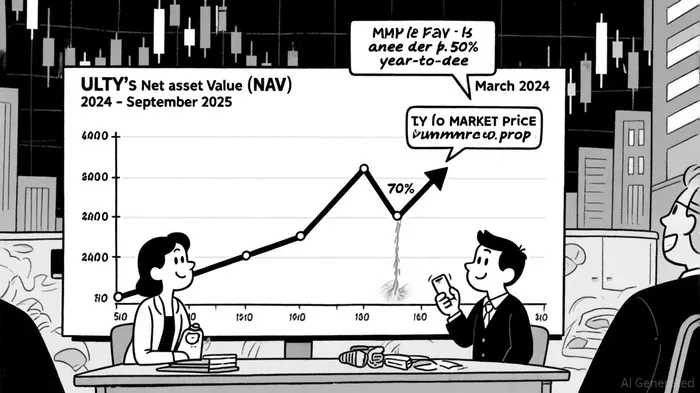

The consequences are stark. Between March 2024 and February 2025, ULTY's NAV plummeted nearly 70% [4], a collapse exacerbated by the compounding effect of return-of-capital distributions. Even after YieldMax retooled the strategy in early 2025—introducing weekly distributions and options collars—the fund's year-to-date price decline of 36.01% as of September 2025 underscores the fragility of its model [4].

Structural Challenges: Fees and Turnover as Accelerants

ULTY's structural challenges extend beyond its payout strategy. The fund carries a 1.30% expense ratio, significantly higher than the average for equity income ETFs [3]. Coupled with a 717% turnover rate, these costs accelerate NAV decay. High turnover not only increases transaction costs but also reduces the fund's ability to compound gains through long-term holding strategies. As 247WallSt notes, “ULTY's high fees and turnover rate exacerbate NAV erosion, making it a ticking time bomb for investors” [3].

Moreover, the fund's reliance on high-implied-volatility equities and options strategies introduces inherent risks. While collars and put spreads aim to mitigate downside risk, they also cap upside potential. This trade-off is particularly problematic in a market environment where volatility is both a blessing and a curse. For instance, ULTY's recent reduction in crypto exposure—a sector known for its volatility—may have been a risk-mitigation move, but it also signals a retreat from the very assets that fueled its initial gains [1].

A Misaligned Incentive Structure

ULTY's structural issues are compounded by a misalignment between its payout strategy and long-term value preservation. The fund's 12.22% cumulative NAV increase through August 31, 2025, is a positive sign, but this growth is time-dependent and contingent on favorable market conditions [2]. In a prolonged downturn, the fund's ability to sustain distributions—and its NAV—will be severely tested.

Critics argue that ULTY's model is inherently flawed. As Seeking Alpha highlights, “NAV erosion is a well-documented challenge for ULTYULTY--, as the fund frequently pays out distributions that reduce the NAV over time, especially if gains from option premiums and market appreciation do not fully offset these payouts” [1]. This dynamic creates a vicious cycle: declining NAVs force the fund to rely more heavily on return-of-capital distributions, further eroding the underlying assets.

Conclusion: A High-Risk Proposition

ULTY's structural challenges—aggressive payout strategies, high fees, and volatile asset allocation—make it a high-risk proposition for most investors. While the fund's options strategies and diversification efforts have mitigated some risks, they cannot overcome the fundamental flaws in its design. For investors seeking stable income, ULTY is not a core holding but a speculative bet with a high probability of principal loss.

As the market enters historically weaker September conditions, the pressure on ULTY's NAV will intensify. Investors must weigh the allure of high yields against the reality of structural decay—and ask whether the returns are worth the risk.

Comentarios

Aún no hay comentarios