UK Construction Sector Contraction and Housing Market Stagnation: Investment Risk and Recovery Opportunities in Post-Budget Real Estate and Infrastructure

The UK construction sector has navigated a turbulent three-year period, marked by sharp contractions, policy-driven cost pressures, and uneven regional recovery. While the 2025 Autumn Budget introduced measures to stabilize infrastructure investment and address labor shortages, it also exacerbated affordability challenges and regulatory complexities. For investors, the sector presents a paradox: structural risks coexist with targeted opportunities in green energy, regional development, and government-backed projects.

Investment Risks: Policy Pressures and Market Volatility

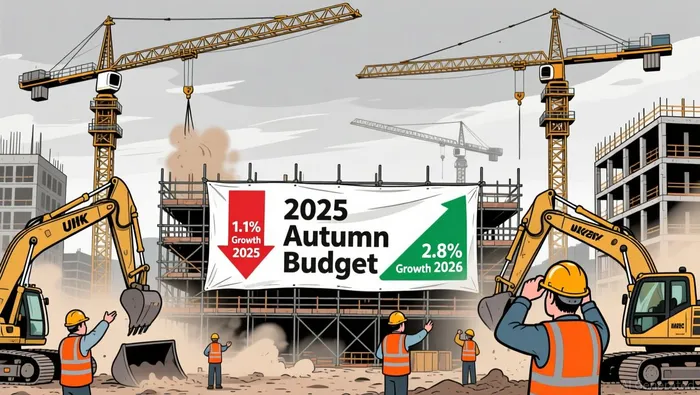

The 2025 budget's emphasis on fiscal consolidation has introduced headwinds for the construction sector. A 4.1% increase in the National Living Wage for workers aged 21 and over, coupled with an 8.5% rise for 18–20-year-olds, has raised input costs for firms operating on narrow margins. According to the Construction Products Association (CPA), these wage hikes, combined with tax rises and spending cuts, have forced industry groups to revise growth forecasts downward-projecting 1.1% growth in 2025 and 2.8% in 2026, significantly below earlier expectations.

Affordability challenges in the housing market further compound these risks. Despite a 25% increase in housing starts in Q1 2025 compared to Q2 2024, London's housing registrations fell by 59% annually, driven by delays in high-density projects and regulatory scrutiny under the Building Safety Regulator. The introduction of a mansion tax on homes over £2 million, alongside unchanged Stamp Duty, has dampened developer confidence, with the CPA warning of potential stalling in housing investment.

Affordability challenges in the housing market further compound these risks. Despite a 25% increase in housing starts in Q1 2025 compared to Q2 2024, London's housing registrations fell by 59% annually, driven by delays in high-density projects and regulatory scrutiny under the Building Safety Regulator. The introduction of a mansion tax on homes over £2 million, alongside unchanged Stamp Duty, has dampened developer confidence, with the CPA warning of potential stalling in housing investment.

Material and labor costs remain stubbornly elevated. Tender price inflation is projected to stay between 2–4% for buildings and 4–6% for infrastructure in 2025, driven by persistent labor shortages and capacity constraints in specialist trades. Meanwhile, material costs for metals and energy, though stabilized compared to previous years, remain above long-term averages, squeezing profit margins according to JLL.

Recovery Opportunities: Infrastructure and Regional Divergence

Amid these challenges, the 2025 budget allocated £890 million for the Lower Thames Crossing and £13 billion in flexible funding for skills development and infrastructure projects across seven English regions according to ICE. These investments, coupled with planning reforms-including the reintroduction of mandatory housing targets and the recruitment of 350 additional planners-aim to accelerate approvals for housing and commercial projects as Burges Salmon notes. The Office for Budget Responsibility forecasts a rise in housing supply, suggesting that these measures could mitigate some of the sector's structural bottlenecks according to the same analysis.

Regional disparities highlight recovery potential. The South and Midlands are experiencing a resurgence in commercial office activity, driven by return-to-office trends and inward migration outside London according to JLL. Meanwhile, the North of England is normalizing warehouse construction after a post-pandemic surge, while the £108 billion water sector pipeline is expected to drive civil engineering growth focused on water quality and leak reduction as Glenigan reports.

Government-backed infrastructure projects, particularly in energy and transport, offer long-term resilience. The 10-year infrastructure strategy, published in June 2025, emphasizes long-term funding certainty and streamlined project delivery, with a focus on green energy, rail, and social infrastructure. For instance, solar and nuclear projects are attracting capital despite policy uncertainties, while the Northern Powerhouse Rail and Docklands Light Railway extension received notable commitments according to Lexology.

Sustainability and ESG-Driven Growth

Environmental regulations are reshaping the sector's trajectory. Mandatory carbon emissions reporting and digital product passports are pushing firms toward low-carbon designs and verified environmental product declarations (EPDs), particularly for materials like steel and aluminum as Glenigan notes. While these changes add compliance costs, they also open avenues for innovation in green construction and retrofitting.

Investors are increasingly prioritizing structurally resilient sectors, such as logistics, data centers, and industrial real estate, driven by e-commerce growth and digital infrastructure demands according to Brown Jacobson. Decentralized investment in regional development is gaining traction, with 47% of respondents anticipating growth outside London according to the same report.

Conclusion: Cautious Optimism Amid Uncertainty

The UK construction sector's path to recovery remains uneven. While infrastructure and energy sub-sectors offer growth, private housing and commercial construction face affordability and demand headwinds. The success of the 2026 recovery will hinge on the government's fiscal choices, with risks of contraction if tax rises disproportionately impact households and businesses as The FIS reports.

For investors, the key lies in balancing short-term risks with long-term opportunities. Targeted investments in government-backed infrastructure, green energy, and regional development-coupled with strategic risk mitigation in labor and supply chains-could yield resilience in an otherwise volatile market. As the sector navigates policy shifts and cost pressures, adaptability will be paramount.

Comentarios

Aún no hay comentarios