UDR: A Value Play in a Resilient Apartment REIT Sector

The apartment REIT sector has long been a cornerstone of income-focused portfolios, but 2025 has tested its resilience. While industrial and data center REITs have surged on supply constraints and tech-driven demand[1], apartment REITs face headwinds from softening rental growth and higher mortgage rates[2]. Yet within this challenging landscape, UDRUDR--, Inc. (NYSE: UDR) emerges as a compelling value play.

A Sector in Transition

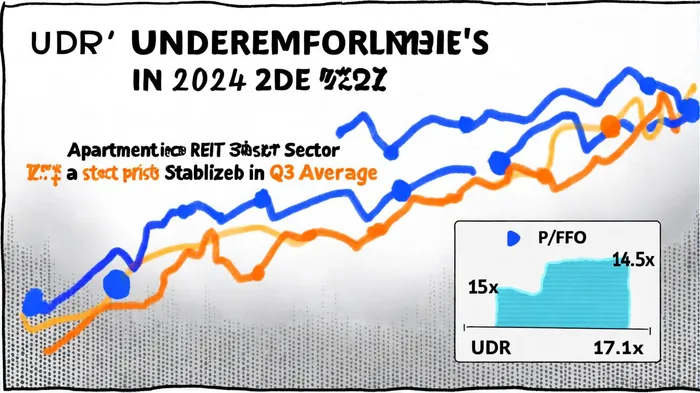

The apartment REIT sector's average P/FFO ratio has contracted to 17.1x as of September 2025, down from historical highs of 26.19x[3]. This reflects investor caution amid macroeconomic uncertainties. However, UDR trades at a 14.5x P/FFO multiple, calculated using its September 19, 2025, stock price of $37.56 and Q3 2025 FFO per share of $0.54[4]. This 15% discount to the sector average suggests undervaluation, particularly when considering UDR's strong fundamentals.

UDR's Strategic Advantages

UDR's focus on high-barrier-to-entry markets—such as Phoenix, Raleigh, and Nashville—positions it to outperform in a fragmented recovery. These Sun Belt cities have seen robust population growth and job creation, offsetting some of the sector's broader challenges[5]. In Q1 2025, UDR reported 2.6% same-store revenue growth and 77% year-over-year net income per share, outpacing consensus estimates[6].

The company's limited exposure to rent-stabilized housing in New York City—a drag on many coastal peers—further insulates it from regulatory headwinds[7]. Meanwhile, UDR's conservative leverage profile (debt-to-equity below 40%)[8] ensures it can weather interest rate volatility without compromising dividend sustainability.

Navigating Sector-Wide Challenges

Apartment REITs face a dual threat: softening demand from affordability constraints and a 17.2% discount to NAV for office peers[9]. Yet UDR's 4.47% dividend yield[10] and updated 2025 guidance (FFOA per share of $2.49–$2.55)[11] suggest management remains confident in long-term cash flow generation. Analysts have raised full-year 2025 EPS estimates to $2.52, reflecting optimism about UDR's ability to adapt to shifting market conditions[12].

The Case for Value Investors

For value investors, UDR's combination of undervaluation and operational strength is rare. While the sector's 17.1x P/FFO ratio implies skepticism about future growth, UDR's 14.5x multiple discounts its potential. Historical data shows apartment REITs typically trade at a 16.98x median P/FFO over five years[13], suggesting UDR could see re-rating if macroeconomic conditions stabilize.

Moreover, UDR's recent leasing performance—April 2025 spreads outpacing peers by 1.2%—demonstrates pricing power in a competitive market[14]. This bodes well for FFO per share growth, which is critical for justifying a higher valuation multiple.

Risks and Considerations

UDR's Sun Belt strategy is not without risks. Rising construction activity in markets like Phoenix could erode rental growth, and a prolonged rate hike cycle may delay a full recovery. However, UDR's conservative balance sheet and focus on high-demand submarkets mitigate these risks better than most peers.

Conclusion

UDR's undervaluation relative to the apartment REIT sector, coupled with its strategic positioning and operational discipline, makes it a compelling long-term investment. While the sector faces near-term headwinds, UDR's fundamentals suggest it is well-positioned to outperform as market conditions normalize. For value investors seeking exposure to residential real estate, UDR offers a rare blend of affordability and resilience.

Comentarios

Aún no hay comentarios