Is Twilio (TWLO) a Buy, Hold, or Sell Amid Mixed Earnings Outlook and Valuation Signals?

In the high-stakes arena of cloud communications, TwilioTWLO-- (TWLO) has long been a bellwether for innovation and growth. Yet, as the company navigates a complex mix of earnings surprises, valuation extremes, and shifting analyst expectations, investors are left to parse whether its current trajectory signals a contrarian opportunity or a cautionary tale.

Earnings Performance: Growth, Profitability, and Guidance Woes

Twilio's Q2 2025 results underscored its resilience in a competitive market. Revenue surged 13% year-over-year to $1.23 billion, driven by a 14% increase in communications revenue to $1.15 billion [1]. Non-GAAP income from operations hit a record $220.5 million, up 26% annually, while free cash flow expanded 33% to $263.5 million [1]. These figures reflect operational discipline and customer loyalty, with a 108% Dollar-Based Net Expansion Rate and 10% year-over-year growth in active customer accounts [1].

However, the company's guidance for Q3 2025—revenue of $1.245–$1.255 billion and non-GAAP EPS of $1.01–$1.06—fell short of expectations. Analysts had previously forecast Q3 EPS of $1.15, and the revised range now implies a 12% earnings contraction [2]. This downgrade, coupled with gross margin pressures from a messaging-driven revenue mix and elevated R&D spending, triggered an 11% premarket stock price drop post-earnings [2].

Analyst Estimate Revisions: A Tale of Two Narratives

The Zacks Consensus EPS estimate for Twilio rose 0.58% over 30 days, hinting at cautious optimism [2]. Yet, the earnings beat of $1.19 (versus $1.05) was swiftly followed by a guidance downgrade, leading to one positive and one negative EPS revision in the past 90 days [2]. This duality reflects a market grappling with Twilio's dual identity: a high-growth innovator in AI-driven communications and a company facing margin compression in a maturing market.

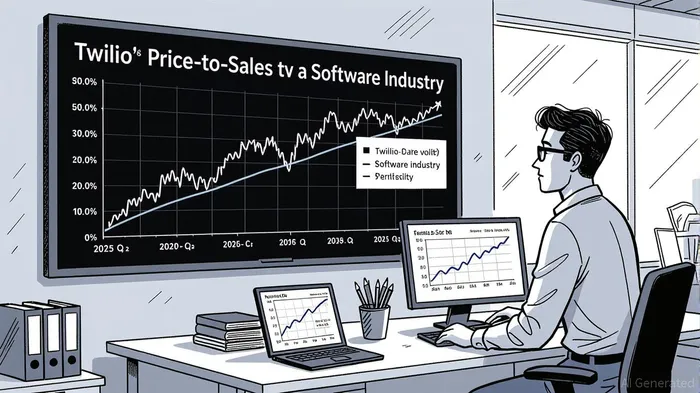

Valuation Metrics: Premium Pricing Amid Industry Comparisons

Twilio's valuation metrics remain extreme by historical and industry standards. Its P/E ratio of 770.80 and EV/EBITDA of 70.16 place it in the 90th percentile of Software industry multiples [3]. While its forward P/S ratio of 3.39 is below the industry average of 5.65, it still ranks worse than 58.65% of peers, with a median of 2.56 [3]. The EV/Revenue ratio of 3.23, though lower than its peak of 37.74 in 2015, remains above the industry median of 2.54 [3].

Market Reaction and Strategic Moves: Contrarian Cues

The post-earnings price drop initially signaled investor unease, but Twilio's stock showed signs of recovery as analysts raised price targets to $144, citing confidence in AI integration and strategic partnerships [2]. Share repurchases of $176.7 million under its $2 billion buyback program also signaled management's conviction in undervaluation [1]. For contrarians, this volatility presents a paradox: high valuations suggest overconfidence, while operational strength and AI-driven innovation hint at underappreciated long-term potential.

Contrarian Investment Thesis: Buy, Hold, or Sell?

Twilio's case embodies the classic contrarian dilemma. On one hand, its valuation metrics are unsustainable for a company with 9–10% organic growth guidance, far below its historical 20–30% rates. On the other, its profitability milestones, customer retention, and AI-driven product roadmap suggest a transition from a speculative growth story to a durable cash-flow generator.

For investors with a 3–5 year horizon, Twilio's current price may represent a buying opportunity if the stock corrects further, particularly if gross margin pressures abate and AI adoption accelerates. However, those averse to volatility or seeking near-term returns should consider a hold, given the elevated multiples and guidance risks.

Conclusion

Twilio's Q2 results and valuation extremes paint a nuanced picture. While the company's fundamentals remain robust, the market's mixed signals—optimism in earnings, skepticism in guidance, and premium pricing—demand a disciplined approach. For contrarians, patience and a focus on long-term innovation may outweigh short-term volatility.

Comentarios

Aún no hay comentarios