TSX's Record Highs Amid Rate Cut Expectations: How Monetary Policy Tailwinds Are Reshaping Equity Valuations and Positioning Canadian Equities for Outperformance

The Toronto Stock Exchange (TSX) has surged to record highs in 2025, driven by a confluence of factors including expectations of aggressive monetary easing from the Bank of Canada (BoC) and the U.S. Federal Reserve (Fed). As investors brace for a pivotal policy decision on September 17—when the BoC is widely expected to cut its overnight rate by 25 basis points—the market is recalibrating its expectations for equity valuations and sector performance. This analysis explores how monetary policy tailwinds are reshaping Canadian equity valuations and why the TSX is uniquely positioned to outperform global benchmarks like the S&P 500.

Monetary Policy Tailwinds and Equity Valuations

Central bank rate cuts have historically acted as a catalyst for equity markets, particularly for rate-sensitive sectors. According to a report by Reuters, the TSX has averaged a 12.8% gain one year after the last BoC rate hike in previous cycles, underscoring the index's responsiveness to monetary easing [1]. This trend is amplified in 2025, as both the BoC and Fed signal dovish stances. The BoC's recent reductions—from 5% in June 2024 to 3.75% by October 2024—have already created a favorable environment for sectors like financials and real estate, which thrive on lower borrowing costs [6].

The impact on valuations is evident. As of September 2025, the TSX's trailing P/E ratio stands at 19.42, above its 5-year average of 17.38 [2]. Within the index, Canadian banks have seen their P/E ratios expand from 12.6x in September 2024 to 15.1x in September 2025, reflecting optimism about improved lending activity and margin stability [6]. For example, Royal Bank of CanadaRY-- (RY) trades at a TTM P/E of 15.24, near its 10-year high, as investors anticipate rate cuts to boost net interest margins [5].

Sector Rotation and Structural Advantages

The TSX's composition—weighted toward financials, energy, and materials—positions it to benefit disproportionately from rate cuts. Unlike the S&P 500, which is dominated by technology stocks (e.g., the “Magnificent Seven” accounting for 35% of the index), the TSX's exposure to cyclical sectors aligns with the economic stimulus provided by monetary easing [3]. For instance, energy and materials sectors have seen valuation expansion as lower rates reduce discount rates for future cash flows, making capital-intensive projects more attractive [1].

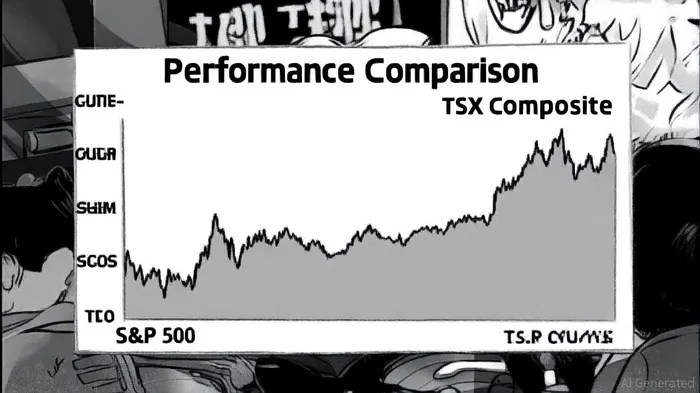

Comparative analysis with the S&P 500 reveals further advantages. While the S&P 500's trailing P/E of 28.21 as of August 2025 suggests overvaluation [6], the TSX's forward P/E remains lower, offering a margin of safety for investors. This undervaluation is partly due to the TSX's broader exposure to sectors like utilities and real estate, which trade at bond-like yields and benefit from lower discount rates [3].

Global Context and Outperformance Potential

Historically, the TSX has outperformed the S&P 500 during rate-cut cycles, particularly in periods of economic uncertainty. A 2025 analysis by ATB Financial notes that the TSX's sensitivity to commodity prices and its concentration in high-dividend sectors make it a compelling alternative to U.S. tech-driven indices [1]. For example, during the 2020 pandemic-driven rate cuts, the TSX rebounded faster than the S&P 500, aided by its exposure to energy and materials [4].

The current environment mirrors this dynamic. While the S&P 500's performance is increasingly concentrated in a narrow group of stocks, the TSX's diversified sector exposure allows it to capitalize on broader economic tailwinds. Analysts at Valuetrend highlight that Canadian equities could see further gains if the BoC continues its rate-cut trajectory, with additional 68.9 basis points of easing priced in for 2025 [5].

Risks and Considerations

Despite the bullish case, risks remain. The Canadian dollar's 7.7% depreciation against the U.S. dollar in 2024 highlights the vulnerability of Canadian equities to divergent monetary policies [2]. Additionally, while rate cuts stimulate growth, they also raise inflation risks, which could force central banks to pivot sooner than expected. Investors must also monitor sector-specific challenges, such as the energy sector's exposure to global demand fluctuations.

Conclusion

The TSX's record highs in 2025 are not merely a function of short-term optimism but a reflection of structural advantages and monetary policy tailwinds. With central banks poised to cut rates, the index's high-dividend sectors and cyclical exposure position it to outperform global benchmarks. While risks persist, the combination of undervaluation, sector rotation, and policy support makes the TSX an attractive destination for investors seeking long-term growth.

Comentarios

Aún no hay comentarios