The Recent TSX Rally: Can Higher Metal Prices Sustain the Momentum in Resource Stocks?

The Toronto Stock Exchange (TSX) has experienced a remarkable rally in 2025, driven by surging demand for commodities and a global shift toward clean energy. The S&P/TSX Composite Metals & Mining Index, for instance, surged by 80% year-to-date by late September 2025, fueled by record-high gold prices and robust demand for critical minerals like copper and lithium [3]. However, as investors weigh the sustainability of this momentum, the interplay between valuation metrics, sector rotation, and reaccelerating commodity demand emerges as a critical lens for analysis.

Drivers of the Rally: Green Energy and Industrial Demand

The reacceleration of commodity demand in 2025 has been shaped by two primary forces: the green energy transition and industrial activity. Gold, now trading above US$3,800 an ounce, has benefited from its role as a safe-haven asset amid geopolitical uncertainties, while base metals like copper and nickel are in high demand for electric vehicle (EV) production and renewable energy infrastructure [1]. According to a report by the Australian Office of the Chief Economist (AOCE), global industrial activity-particularly in Asia and Europe-has driven infrastructure investments, further boosting demand for industrial metals [5].

Meanwhile, the energy transition has created a structural tailwind for resource stocks. Companies like Teck ResourcesTECK-- and Barrick Gold are capitalizing on the need for critical minerals, while traditional energy firms such as Suncor Energy and Enbridge are diversifying into green energy projects [1]. This shift aligns with government incentives for renewable energy, which are expected to sustain demand for raw materials in the coming years [4].

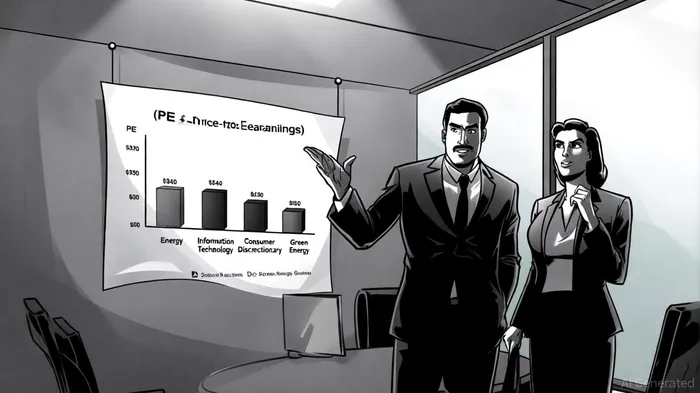

Valuation Metrics: Undervalued or Overlooked?

Despite the strong performance of resource stocks, their valuation metrics suggest a more cautious outlook. The Canadian Metals and Mining Industry has a price-to-earnings (PE) ratio of 60.9x, significantly lower than its 3-year average of 286x, indicating investor skepticism about long-term growth potential [1]. Similarly, the price-to-sales (PS) ratio of 6.3x is below its 3-year average of 8.2x, hinting at potential undervaluation [1].

In contrast, sectors like Information Technology and Consumer Discretionary command higher valuations. The Information Technology sector, for example, has a PE ratio of 40.65 as of July 2025, driven by AI adoption and cloud computing innovations [1]. The Consumer Discretionary sector, which rebounded strongly in 2025, has a PE ratio of 29.21, reflecting robust consumer demand [1]. This divergence underscores a broader market rotation from growth-oriented tech stocks to value-driven resource sectors, as investors seek exposure to hard assets amid inflationary pressures and a weakening U.S. dollar [5].

Sector Rotation and Macroeconomic Shifts

The 2025 TSX rally also reflects a strategic reallocation of capital across sectors. Resource stocks have outperformed as investors pivot away from overvalued U.S. equities and into commodities, which are seen as hedges against macroeconomic volatility [5]. Meanwhile, the energy transition has spurred demand for critical minerals, creating a virtuous cycle of investment in mining and energy firms [1].

However, this rotation is not without risks. While the green energy sector has a PE ratio of 23.43, suggesting optimism about its growth trajectory [3], base metals remain vulnerable to industrial demand shortfalls. For instance, copper and aluminum prices are projected to grow moderately in 2025, but any slowdown in global manufacturing could dampen their performance [5]. Additionally, the Canadian Metals and Mining Industry's market capitalization of CA$747.4 billion, though substantial, faces margin pressures in agriculture and other commodity sub-sectors [2].

Sustainability of the Momentum

The question of whether higher metal prices can sustain the TSX rally hinges on two factors: the resilience of commodity demand and the alignment of valuations with long-term growth. While the green energy transition and industrial activity provide a structural tailwind, short-term risks such as U.S. tariff policies and geopolitical de-escalation could disrupt trade flows and pricing [3].

Moreover, gold's expected decline in 2025 compared to its previous performance raises concerns about the sustainability of its price surge [5]. Investors must also contend with the sector's high volatility, as seen in the 30% year-over-year decline in commodity value pools in 2025 [2].

Conclusion: A Balanced Approach

For investors, the TSX rally presents both opportunities and challenges. Resource stocks appear undervalued relative to their fundamentals, particularly in the context of reaccelerating demand for critical minerals. However, the sector's exposure to macroeconomic and geopolitical risks necessitates a diversified approach. As the energy transition gains momentum, thematic investments in precious metals and clean energy materials may offer a balance between growth and stability.

In the coming months, the TSX is projected to continue its upward trajectory, with forecasts of 1.2% growth in October 2025 and 0.4% in December 2025 [4]. Whether this momentum endures will depend on how well the sector navigates the interplay of valuation metrics, sector rotation, and the evolving demand landscape.

Comentarios

Aún no hay comentarios