Trump's Policies and Social Security's Future: How Retirees Can Navigate the Storm

Here's the deal: Social Security is at a crossroads, and the policies enacted under the Trump administration have thrown both a lifeline and a grenade into the mix. On one hand, tax relief for seniors has offered short-term relief. On the other, reforms like the repeal of the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) have accelerated the program's financial unraveling. For retirees and pre-retirees, the message is clear: the clock is ticking, and your asset allocation strategy needs to reflect the looming reality of benefit cuts and inflation-linked COLAs that may not keep pace with real-world costs.

Let's start with the Trump-era changes. The "One Big Beautiful Bill Act" (OBBBA), signed in July 2025, reduced federal taxes on Social Security benefits for Americans aged 65 and older. While this provided immediate relief to millions, it also created a temporary revenue shortfall for the program. The Social Security Administration estimates this tax break will expire by 2028, but the damage to the program's long-term finances is already baked in.  Meanwhile, the "Social Security Fairness Act" repealed WEP and GPO, boosting benefits for public-sector workers and their spouses. Sounds great, right? Not so fast. According to the 2025 Trustees Report, these changes pushed the projected insolvency date of the OASI trust fund from 2033 to 2034 and worsened the 75-year deficit by 0.14% of taxable payroll.

Meanwhile, the "Social Security Fairness Act" repealed WEP and GPO, boosting benefits for public-sector workers and their spouses. Sounds great, right? Not so fast. According to the 2025 Trustees Report, these changes pushed the projected insolvency date of the OASI trust fund from 2033 to 2034 and worsened the 75-year deficit by 0.14% of taxable payroll.

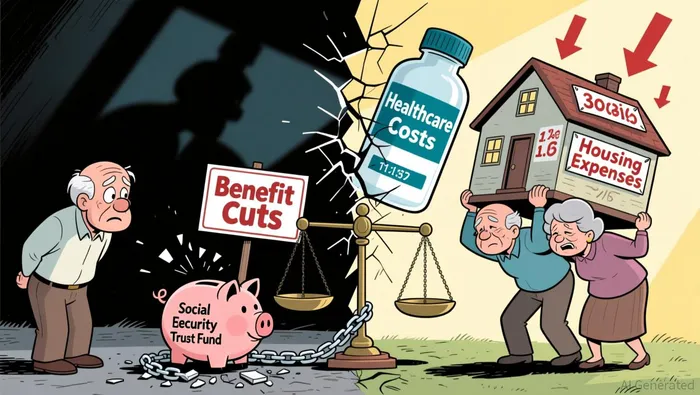

The math is grim. By 2034, Social Security will only cover 77% of scheduled benefits. And let's not forget the broader demographic headwinds: an aging population, a shrinking worker-to-beneficiary ratio and declining birth rates are all straining the system. For retirees, this means the safety net is fraying. A typical couple retiring in 2033 could face $25,000 in lifetime benefit cuts due to insolvency.

Now, let's pivot to the silver lining: inflation-linked COLAs. The 2025 adjustment was 2.5%, and 2026 is projected at 2.8% according to the Social Security Administration. But here's the rub-these increases are based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), which doesn't fully capture the inflation retirees actually face, especially in healthcare and housing. For example, Medicare Part B premiums are set to rise by $21.50 in 2026, directly eroding the value of the COLA.

So, what's the takeaway for investors? Diversification is no longer optional-it's existential. Retirees must build portfolios that hedge against both inflation and longevity. Here's how:

- Delay Social Security Benefits: Every year you wait to claim (up to age 70) increases your monthly payout by roughly 8%. This is a guaranteed, inflation-adjusted annuity from the government according to financial experts.

- Prioritize Growth-Oriented Assets: With interest rates low and cash returns dwindling, retirees should allocate a portion of their portfolio to equities, particularly dividend-paying stocks and sectors like healthcare and technology according to financial advisors.

- Stress-Test Your Plan: Assume Social Security benefits could be cut by 23% in 2034. If your portfolio can't handle that scenario, you're underprepared.

- Tax-Efficient Withdrawals: Coordinate withdrawals from IRAs, 401(k)s, and Roth accounts to minimize tax drag, especially as benefit taxation rules evolve according to financial planners.

The bottom line? Trump's policies have bought time but not a solution. Retirees must act now to insulate themselves from the inevitable. As the old saying goes, "Don't put all your eggs in one basket"-especially when that basket is Social Security.

Comentarios

Aún no hay comentarios