Trade War Spillovers: How China's Dairy Tariffs on the EU Signal Shifting Import Dynamics and Opportunities in Global Dairy Exports

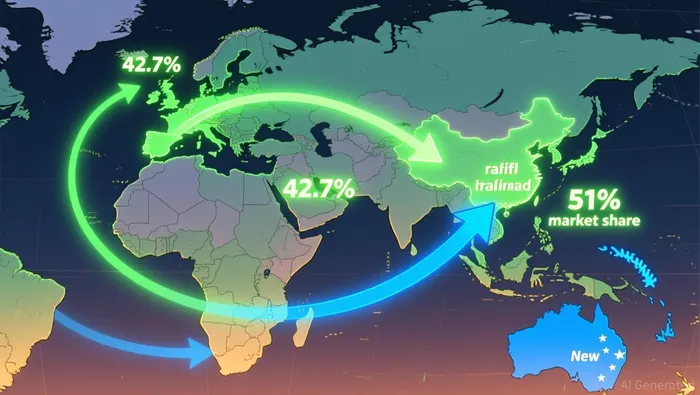

The global dairy industry is undergoing a seismic shift as China's retaliatory tariffs on EU dairy exports-part of a broader trade dispute-reshape supply chains and open new avenues for emerging markets. These tariffs, which reached provisional rates of up to 42.7% in August 2024, are not merely a political maneuver but a recalibration of China's dairy import strategy, favoring high-value products over commodity-grade goods. For investors, this signals a critical inflection point: the EU's dominance in China's dairy market is waning, while countries like New Zealand and Australia are capitalizing on their competitive advantages.

EU's Defensive Stance and the Tariff Blow

China launched an anti-subsidy investigation into EU dairy exports in June 2024, targeting products subsidized under the EU's Common Agricultural Policy (CAP) and national programs in countries like Ireland and France. The provisional duties, averaging 30%, hit key EU dairy exporters-France, Ireland, and the Netherlands-hard, with Ireland alone losing €359 million in annual exports to China. The European Commission has defended these subsidies as compliant with international rules, but the tariffs have already disrupted supply chains, forcing EU dairy firms to seek alternative markets.

This trade friction reflects deeper political tensions. The fragmented EU post-2024 elections has hindered a unified response to China, leaving member states to navigate the crisis individually. Meanwhile, China's dairy production is projected to grow 3.2% in 2024, reducing its reliance on EU imports and further amplifying the impact of these tariffs.

China's Shifting Import Preferences: Quality Over Quantity

China's dairy import dynamics are evolving rapidly. While total imports in H1 2024 fell 14.1% year-on-year to 1.19 million tonnes, demand for high-fat, value-added products like butter and cheese surged. Butter imports rose by nearly 6,000 tonnes in 2024, and cream imports increased 12.7%. This shift aligns with China's growing urban middle class, which prioritizes premium dairy products for health and lifestyle reasons.

The decline in powdered milk imports-whey down 36%, skimmed milk powder 9.5%-reflects China's push for self-sufficiency, with domestic production rising to 85% of demand in 2024. However, this does not eliminate import needs; rather, it narrows the focus to specialized, high-margin goods. By 2025, China's dairy imports had rebounded 6% year-on-year, driven by butter and cheese, with sweet whey powder imports alone up 30%.

Winners in the New Landscape: New Zealand and Australia Lead

New Zealand has emerged as the clear beneficiary of this reallocation. With a 51% market share in China's dairy imports, it leverages its free trade agreement (FTA) for duty-free access, outpacing competitors like the EU and the U.S. China's dairy import data shows a clear shift in demand patterns. Australia, too, is gaining ground, particularly in cheese and whey exports, as Chinese buyers seek alternatives to EU products.

The U.S., despite facing its own tariffs, retains a niche in low-cost commodity exports, but its market share is shrinking. The UK, meanwhile, has seen minimal gains, with its 1% share of China's dairy imports in 2024 remaining stagnant amid trade policy volatility. This underscores the importance of trade agreements and product differentiation in capturing Chinese demand.

Emerging Market Strategies and Investment Opportunities

For emerging markets, the key to accessing China's dairy demand lies in aligning with its premiumization trend. Producers must focus on high-value products like cheese, butter, and specialty whey, which command higher margins and align with China's evolving tastes. Additionally, supply chain resilience-diversifying export routes and securing long-term contracts-will be critical amid ongoing trade uncertainties.

Investors should also monitor China's domestic dairy sector, which is consolidating into large, efficient operations. This trend, driven by improved feed conversion ratios and herd management, could further reduce import volumes for commodity products but create opportunities for partners in value-added processing and innovation.

Conclusion: A Market in Transition

China's dairy tariffs on the EU are more than a trade spat; they signal a strategic pivot toward self-reliance and premiumization. For global dairy exporters, this means rethinking supply chains and product portfolios to meet China's new demands. Countries with FTA advantages, like New Zealand, and those capable of producing high-value dairy goods will dominate the next phase of this market. Investors who recognize this shift early stand to benefit from a sector poised for structural transformation.

Comentarios

Aún no hay comentarios