Thruvision Group's 2025 Earnings Underperformance: A Strategic Crossroads for Long-Term Resilience

A Stark Earnings Reality

Thruvision Group's Full Year 2025 results paint a grim picture of operational distress. According to a report by Yahoo Finance, the company reported revenue of £4.16 million, a 47% decline from £7.8 million in FY 2024 [1]. This was accompanied by a net loss of £4.60 million—a 62% increase in losses year-over-year—and an EPS of £0.028, worsening from £0.019 in FY 2024 [1]. Analysts had projected revenue of £5.5 million and an EPS of £0.034, meaning Thruvision missed expectations by 24% and 17%, respectively [1]. These figures underscore a company struggling to adapt to market dynamics while balancing liquidity constraints.

Strategic Initiatives: A Race Against Time

Faced with declining cash reserves—projected to last until May 2025 if no new orders materialize—Thruvision has launched a formal strategic review process [3]. The company is exploring options such as equity raises, strategic partnerships, or a full sale, with financial advisors Investec Bank and Raymond James overseeing the process [3]. This urgency is compounded by the fact that Thruvision's FY25 interim results revealed a 51% drop in H1 revenue to £1.9 million compared to £3.5 million in the same period in 2024 [2].

Despite these challenges, the company has identified pockets of growth. Retail Distribution revenue doubled to £1.6 million in FY25, accounting for 85% of total sales [2]. Meanwhile, the Aviation sector remains a focal point, with demand driven by the TSA National Mandate for advanced screening solutions [2]. However, these opportunities remain unsecured, and the Board has emphasized that the £15 million in potential contracts for FY26 hinges on successful negotiations [3].

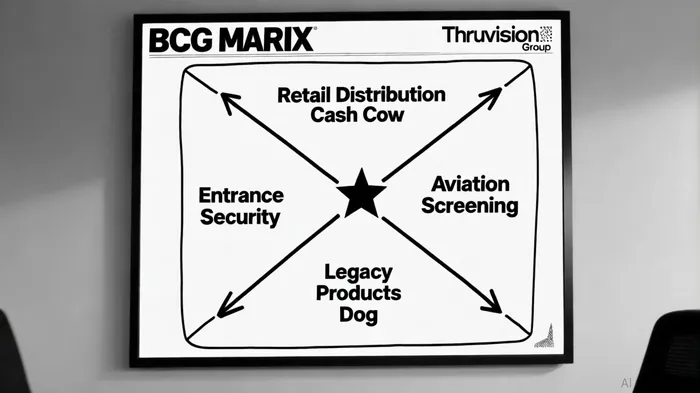

BCG Matrix: A Framework for Strategic Clarity

Thruvision's application of the BCG Matrix offers a structured approach to resource allocation amid uncertainty. The framework categorizes business segments into four quadrants:

1. Stars: High-growth, high-market-share segments like Aviation Screening, which aligns with the TSA mandate and requires sustained investment to dominate a growing market [4].

2. Cash Cows: Retail Distribution, which generated £1.6 million in FY25, represents a high-market-share, low-growth segment that could fund innovation in other areas [4].

3. Question Marks: Entrance Security, while in a high-growth market, holds low market share and demands strategic investment to determine its viability [4].

4. Dogs: Legacy products with minimal profitability are candidates for divestment to streamline operations [4].

This analysis highlights Thruvision's prioritization of high-potential segments while acknowledging the need to phase out underperforming areas. However, the company's limited cash reserves constrain its ability to invest aggressively in Stars or Question Marks, creating a delicate balancing act.

Operational Resilience: A Mixed Outlook

Thruvision's resilience hinges on its ability to execute its strategic review and secure near-term contracts. The appointment of 10 Value-Added Resellers (VARs), including Sensormatic, has strengthened its sales pipeline [2], but this alone may not offset the revenue shortfall. The company's reliance on external financing or a sale underscores its vulnerability to market volatility.

Yet, the Board's emphasis on technological innovation—particularly in Aviation—suggests a long-term vision aligned with industry trends. If Thruvision can leverage its expertise in screening solutions to capture TSA-driven demand, it may yet pivot from a cash-burn scenario to a growth trajectory.

Conclusion: A High-Risk, High-Reward Proposition

Thruvision Group's FY25 results reflect a company at a crossroads. While the earnings underperformance and liquidity constraints raise red flags, the strategic initiatives and BCG-driven prioritization offer a roadmap for recovery. Investors must weigh the risks of operational failure against the potential rewards of a successful pivot in high-growth markets. For now, the company's survival depends on securing capital or a strategic buyer—and the clock is ticking.

Comentarios

Aún no hay comentarios