Texas Capital Soars 20.5% in a Year: Should You Buy the Stock Now?

Shares of Texas Capital Bancshares, Inc. TCBI have gained 20.5% in the past year, outperforming the industry’s 8.6% growth.

When comparing the company’s price performance with its peers,BOK Financial Corporation BOKF and Cullen/Frost Bankers, Inc. CFR, it appears that while the TCBITCBI-- stock has underperformed Cullen/Frost, it has outperformed BOK FinancialBOKF-- in the past year. Shares of CFRCFR-- and BOKFBOKF-- have gained 5.6% and 21.1%, respectively, during the same period.

Price Performance

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Let’s examine whether Texas CapitalTCBI-- stock still offers upside potential despite its recent price gains. To assess this, a closer look at the company’s fundamentals and growth outlook is needed.

What Supports Texas Capital Stock?

Potential Fed’s Rate Cut to Support NII: The Federal Reserve reduced interest rates by 100 basis points in 2024 and by 75 basis points through three cuts in 2025. At its March 2026 Federal Open Market Committee (FOMC) meeting, the Fed maintained the target federal funds rate at 3.50%-3.75%, weighing rising inflation pressures from higher energy costs. Nevertheless, the central bank’s ‘dot plot’ suggests a potential rate cut in 2026, which could bring the federal funds rate closer to 3.4%. As such, the lower policy rates are expected to encourage borrowing activity and support net interest income (NII) growth for banks such as Texas Capital, BOK Financial and Cullen/Frost.

Coming back to TCBI, its NII has shown steady improvement, with a five-year compound annual growth rate (CAGR) of 3.43% through 2025. As such, lower borrowing costs and an increase in lending activity are expected to support TCBI’s NII growth in the upcoming period.

Strategic Expansion to Drive Growth: Texas Capital is making steady progress on its 2021 strategic plan aimed at enhancing operating efficiency. As part of this initiative, the company agreed in 2024 to acquire a portfolio with approximately $400 million in committed exposure to healthcare companies, supporting its multi-year effort to expand the corporate banking and healthcare vertical. In April 2025, it also partnered with Axxess to integrate its RevNow revenue cycle management product with Axxess RCM. The integration accelerates payment reconciliation for home health and hospice providers, reducing manual processing from weeks to just 24 hours, enhancing operational efficiency and providing additional support to its healthcare clients.

The company continues to expand its investment banking offerings, building a base of repeatable revenues that support future earnings. It is also implementing technology-driven process improvements to enhance customer experience, reduce risk and improve efficiency.

Further expansion efforts include the 2024 introduction of Texas Capital Direct Lending and the January 2025 launch of Texas Capital Securities’ Equity Research team. These initiatives broaden service offerings, strengthen revenue potential and provide a platform to grow the Institutional Services business. Collectively, they are expected to enhance operating efficiency, with management targeting mid-to-high single-digit growth in adjusted total revenues for 2026.

The Zacks Consensus Estimate for TCBI’s 2026 and 2027 revenues is pegged at $1.35 billion and $1.45 billion, which indicate year-over-year growth rates of 7.8% and 6.9%, respectively.

Revenue Estimates

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Balance Sheet Strength Supports Growth: The company continues to show resilience despite a challenging environment. Its net loans held for investment grew at a seven-year CAGR of nearly 1%, while total deposits rose 3.6% CAGR through 2025. With a relationship-driven business model, ongoing client acquisition and expanding fee-based offerings, TCBI is well-positioned to drive further loan and deposit growth in the upcoming period.

Strong Liquidity and Capital Position: Texas Capital remains financially resilient, backed by a solid liquidity base and manageable debt. As of Dec. 31, 2025, the company held $2.09 billion in liquid assets, while total debt (including long-term and short-term borrowings) stood at $950.6 million. Its times-interest-earned ratio rose to 10.5 in the fourth quarter of 2025, reflecting a healthy capacity to service debt.

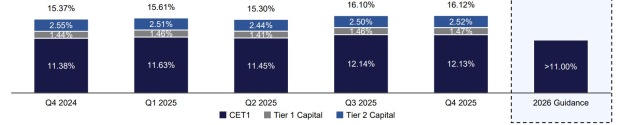

The company’s capital ratios remain robust, with a total capital ratio of 16.1% and a common equity tier 1 (CET1) ratio of 12.1%, well above regulatory requirements. CET1 is expected to remain above 11% in 2026, providing flexibility for growth initiatives and shareholder returns. With a strong liquidity position and well-capitalized balance sheet, Texas Capital is well-positioned to sustain operations and navigate potential economic challenges.

Capital Ratios Trend

Image Source: Texas Capital Bancshares, Inc.

Robust Capital Distribution: On Dec. 1, 2025, the company’s board of directors approved a new share repurchase program authorizing up to $200 million of its outstanding common stock through Dec. 31, 2026. As of Dec. 31, 2025, the full $200 million remained available. Supported by a strong capital base, ample liquidity and ongoing client acquisition, Texas Capital’s share repurchase program is sustainable and underscores its ability to pursue opportunistic growth while delivering shareholder value.

What’s Hurting TCBI’s Growth

Rising Non-Interest Expenses: Texas Capital has continued to experience a gradual increase in non-interest expenses, with a five-year CAGR of 1.8% from 2020 to 2025. While investments in technology, process enhancements and workforce compensation are aimed at improving efficiency and supporting long-term growth, ongoing tech spending and higher compensation costs are expected to keep expenses elevated. Management expects adjusted non-interest expense to increase at a mid-single-digit rate in 2026, which may constrain near-term earnings growth.

Expense Trend

Image Source: Zacks Investment Research

Credit Quality Pressures: Deterioration in credit quality remains a challenge for Texas Capital. Its non-performing assets grew at a three-year CAGR of 21.1% through 2025, while net charge-offs rose sharply at a four-year CAGR of 79.3%. Rising criticized assets, particularly in multi-family and office real estate loans, combined with ongoing market uncertainty, are likely to keep credit quality pressures elevated in the near term, potentially impacting financial performance.

Analyzing TCBI’s Earnings Estimates & Valuation

The Zacks Consensus Estimate for Texas Capital’s 2026 earnings is pegged at $7.61 per share, which indicates year-over-year growth of 11.9%. The consensus mark for 2027 earnings is $8.29 per share, suggesting a rise of 8.9%.

Over the past 60 days, the earnings estimates for both 2026 and 2027 have been revised upward.

Estimate Revision Trend

Image Source: Zacks Investment Research

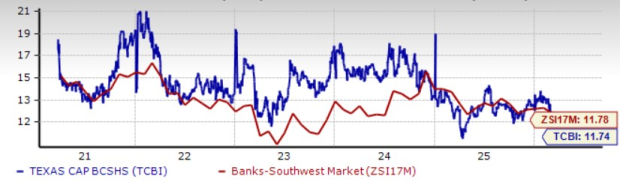

In terms of valuation, TCBI stock appears inexpensive relative to the industry. The company is currently trading at a 12-month trailing price-to-earnings (P/E) ratio of 11.74X, which is lower than the industry’s 11.78X.

Price-to-Earnings F12 M

Image Source: Zacks Investment Research

Meanwhile, Cullen/Frost holds a P/E ratio of 12.60X, while BOK Financial’s P/E ratio stands at 12.50X.

How to Approach the TCBI Stock Now

Texas Capital faces near-term headwinds from rising non-interest expenses, elevated credit quality pressures, and gradual margin constraints. Nevertheless, the bank is positioned to benefit from steady NII growth given lower funding costs and improved loan demand. Also, continued expansion across its corporate banking, healthcare and investment banking segments will support its top-line expansion.

With a strong liquidity position, robust capital ratios and a sustainable share repurchase program, the company’s fundamentals remain solid enough to navigate macroeconomic challenges and pursue strategic growth initiatives while delivering long-term shareholder value. Further, attractive valuation and favorable earnings estimates reinforce the stock’s upside potential.

Hence, investors may consider buying TCBI stock at current levels, given its potential upside and ability to generate steady long-term returns.

The company currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power, you'll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Access the Report Free Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Texas Capital Bancshares, Inc. (TCBI): Free Stock Analysis Report

BOK Financial Corporation (BOKF): Free Stock Analysis Report

Cullen/Frost Bankers, Inc. (CFR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios