Teva's Uzedy Expansion into Bipolar I Disorder: A Catalyst for Market Access and Revenue Growth in Psychiatric Therapeutics

The U.S. Food and Drug Administration's (FDA) October 2025 approval for UZEDY® (risperidone) extended-release injectable suspension for the maintenance treatment of bipolar I disorder (BD-I) marks a pivotal moment for Teva PharmaceuticalsTEVA-- and its biopharmaceutical partner, Medincell. This expansion into BD-I-a condition affecting approximately 1% of U.S. adults-positions UZEDY as a transformative therapy in psychiatric therapeutics, leveraging its proprietary SteadyTeq™ technology to address unmet needs in long-acting injectable (LAI) treatment adherence and safety.

Market Access Acceleration: Technology, Safety, and Dosing Flexibility

UZEDY's approval for BD-I is underpinned by its unique value proposition. Unlike traditional LAIs, which often carry risks such as Post-Injection Delirium/Sedation Syndrome (PDSS), UZEDY's BEPO® (Bio-Erosion Particle) technology ensures controlled drug release, achieving therapeutic concentrations within 6–24 hours post-injection, which eliminates the need for post-injection monitoring-a critical advantage for both providers and payers (as noted in the Business Insider report). Business Insider also noted that the FDA's decision relied on Model-Informed Drug Development (MIDD) methodologies, integrating prior risperidone data for BD-I and long-term safety results from the RISE and SHINE Phase 3 trials for schizophrenia, as detailed in a MedPath report.

The drug's dosing flexibility-three once-monthly options (50 mg, 75 mg, 100 mg)-further enhances its appeal. For patients with BD-I, who often struggle with medication adherence due to symptom variability, UZEDY's subcutaneous administration and extended dosing intervals reduce the burden of frequent clinic visits. Deloitte's market access framework emphasizes the importance of aligning therapeutic value with stakeholder expectations, and UZEDY's profile directly addresses payer priorities: reduced hospitalizations, improved patient outcomes, and cost efficiency, evidenced by UZEDY's $117M revenue in its first full year.

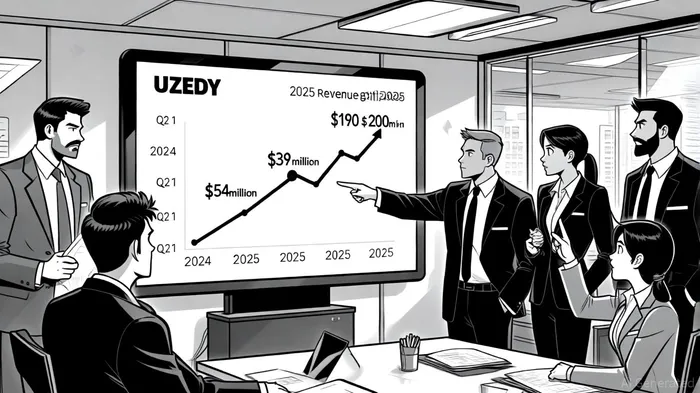

Revenue Upside: From Schizophrenia to Bipolar I

Teva's commercial performance underscores UZEDY's rapid market adoption. In 2024, the drug generated $117 million in revenue, with Q4 sales alone reaching $43 million-exceeding initial forecasts, according to a CentralCharts report. For 2025, the revenue outlook has been raised to $190–$200 million, driven by the BD-I expansion and strong Q1 and Q2 results ($39 million and $54 million, respectively). This trajectory reflects not only clinical demand but also strategic payer engagement, including formulary placements and value-based contracts.

Medincell, which holds mid- to high-single-digit royalties on UZEDY sales and is eligible for $105 million in commercial milestones, further amplifies the financial upside, as noted in a Fierce Pharma article. Meanwhile, Teva's broader schizophrenia portfolio is set to benefit from UZEDY's success, with plans to file a New Drug Application (NDA) for a long-acting injectable olanzapine formulation (TEV-749/mdc-TJK) in Q4 2025. Analysts project this could drive peak sales of $1.5–$2 billion for the combined portfolio by 2030.

Navigating Pricing Dynamics in a Post-IRA Landscape

The Inflation Reduction Act (IRA) introduces pricing pressures for high-cost therapies, but UZEDY's market positioning remains resilient. While the drug is not classified as a high-cost product, its value-based pricing strategy aligns with payer expectations for cost-effectiveness and patient affordability. As noted in a LinkedIn analysis, manufacturers must avoid price hikes exceeding inflation to avoid rebate penalties under the IRA-a challenge UZEDY appears well-equipped to navigate given its strong clinical differentiation.

Strategic Implications for Teva's 2030 Vision

UZEDY's success is central to Teva's ambition to achieve $5 billion in innovative medicine sales by 2030. Alongside Austedo (for Huntington's disease) and Ajovy (for migraine), UZEDY represents a cornerstone of the company's transition from a generic drugmaker to a leader in specialty therapeutics. The BD-I approval not only expands UZEDY's addressable market but also validates Teva's ability to innovate in psychiatry-a sector with limited therapeutic advances in recent decades.

Conclusion

Teva's expansion of UZEDY into BD-I exemplifies how cutting-edge drug delivery technologies and strategic market access planning can unlock significant revenue potential. With a robust clinical profile, favorable payer dynamics, and a clear path to commercial scalability, UZEDY is poised to redefine treatment standards in psychiatric care while delivering substantial returns for investors.

Comentarios

Aún no hay comentarios