Tesla's Long-Term Value: Navigating Financial Realities and Market Hype

Tesla's Long-Term Value: Navigating Financial Realities and Market Hype

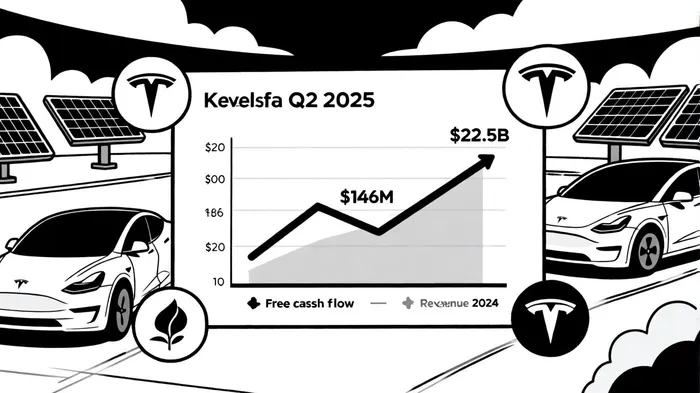

In the ever-shifting landscape of high-growth tech stocks, TeslaTSLA-- Inc. (TSLA) remains a case study in the tension between financial fundamentals and market narrative. The company's Q2 2025 earnings report, released on July 23, 2025, underscored this duality: a 12% year-over-year revenue decline to $22.5 billion and a free cash flow of just $146 million-down 89% from the prior year-contrast sharply with bullish bets on its Robotaxi rollout and energy business expansion, according to Tesla's Q2 report. For investors, the challenge lies in reconciling these numbers with the market's enduring fascination with Tesla's vision.

The Financial Fundamentals: A Mixed Bag

Tesla's financials reveal a company grappling with macroeconomic headwinds and pricing pressures. Automotive revenue fell 16% to $15.79 billion in Q2 2025, driven by a 14% drop in vehicle deliveries to 384,122 units and a 70% plunge in regulatory credit revenue to $439 million, according to a Deep Dive analysis. Gross margins contracted to 19.6% from 22.3% in Q2 2024, as CEO Elon Musk and CFO Vaibhav Taneja cited "tariff pressures" and "soft average selling prices" in CNBC coverage. Meanwhile, capital expenditures surged to $2.39 billion, eroding free cash flow and raising questions about the sustainability of its aggressive investments in AI, robotics, and global Supercharger expansion reported in Tesla's Q2 report.

Yet Tesla's balance sheet retains a veneer of strength. The company ended the quarter with $36.8 billion in cash and investments, Drive Tesla Canada reported, in its coverage of the quarter's highlights (Drive Tesla Canada). Its leverage ratio improved to 0.65, with a debt-to-equity ratio of 0.09-a stark contrast to its 1.6 ratio in 2020, per FinancialModelingPrep. These metrics suggest a deleveraged, resilient entity, but they also highlight a paradox: Tesla is burning cash to fund speculative bets while maintaining a fortress balance sheet.

The Market Narrative: Betting on the Future

The market's response to Tesla's Q2 results was telling. Despite missing EPS estimates by $0.03 and reporting a revenue shortfall, the stock rallied 3% in after-hours trading, buoyed by a delivery beat and optimism over cost discipline reported in Tesla's Q2 report. Analysts like Morgan Stanley's Adam Jonas raised price targets to $305, citing "strong European demand" and the potential of Tesla's robotics initiatives, MarketDrafts noted (MarketDrafts). Wedbush and MarketDrafts emphasized the company's leadership in EVs and Full Self-Driving (FSD) adoption, with the latter setting a $1,500 price target.

This optimism hinges on Tesla's ability to monetize its software and hardware innovations. The launch of Robotaxi in Austin, Texas, and plans to cover half the U.S. population by year-end were highlighted in Drive Tesla Canada's coverage, coupled with a 35% quarter-over-quarter growth in FSD subscriptions noted in Tesla's Q2 report, painting a picture of a company transcending its automotive roots. Meanwhile, the energy business-despite a 7% revenue decline-showed gross profit resilience, hinting at long-term synergies between EVs and renewable energy as Drive Tesla Canada discussed.

Historical data on Tesla's earnings releases provides further context. An earnings backtest of TSLA's price movements following earnings announcements from 2022 to 2025 reveals that the stock has historically outperformed in 71% of events, with an average abnormal return of +18.2% by day 30 post-release. The strongest momentum typically emerges around days 18–20, suggesting a short-term continuation effect. However, this pattern is based on a limited sample of seven events, and single-name volatility remains a risk.

The Dissonance Between Numbers and Narrative

The disconnect between Tesla's financials and market enthusiasm raises critical questions. On one hand, the company's operating income plummeted 42% to $923 million, with net income of $1.17 billion representing the lowest quarterly figure since 2020, according to Tesla's Q2 report. On the other, Wall Street's fixation on "disruption" and "first-mover advantage" has led to a valuation that assumes these innovations will scale rapidly. Deutsche Bank's $355 price target, for instance, rests on the success of the "Model Q" and Cybertruck, despite these products not yet contributing meaningfully to revenue, as noted by FinancialModelingPrep.

This optimism also ignores structural risks. The expiration of U.S. federal EV tax credits, intensifying competition from Chinese EV makers, and the high cost of scaling Optimus robots to 100,000 units annually were all cited in MarketDrafts' analysis and other commentary. UBS's "sell" rating, anchored to overvaluation concerns and discussed in Tesla's Q2 report, reflects skepticism about whether Tesla's current price reflects realistic growth assumptions.

Conclusion: A Calculated Gamble

Tesla's long-term value proposition rests on its dual identity: a cash-generative automaker and a speculative tech play. The financial fundamentals suggest a company in transition, with near-term profitability under pressure but a strong liquidity position. The market narrative, however, demands belief in a future where Robotaxis, FSD subscriptions, and Optimus robots generate revenue streams that dwarf today's automotive sales.

For investors, the key is to assess whether Tesla's strategic bets align with its financial capacity. The company's $36.8 billion cash hoard provides a buffer, but it cannot indefinitely subsidize losses in unproven markets. As Zacks Investment Research notes, Tesla's expansion into robotics and AI-while visionary-ranks it as a "#4 (Sell)" stock, underscoring the risks of overreach.

In the end, Tesla's sustainability will depend on its ability to balance innovation with profitability. The Q2 2025 report is a reminder that even the most audacious visions must eventually reconcile with the arithmetic of free cash flow.

Comentarios

Aún no hay comentarios