Tenet's Year-End 2024 Financial Results: A Strategic Buying Opportunity Amid Market Volatility?

In a healthcare landscape marked by reimbursement pressures and shifting care delivery models, TenetTHC-- Healthcare's 2024 financial results present a compelling case for strategic resilience. With net income surging to $3.2 billion-a 423% increase from $611 million in 2023-and adjusted EBITDA climbing 13% to $4.0 billion, the company has demonstrated its ability to navigate a volatile market, as detailed in Tenet's ASC expansion. This analysis evaluates whether Tenet's performance, margin improvements, and alignment with industry trends position it as a strategic buying opportunity.

Revenue Resilience: Strategic Divestitures and Outpatient Synergy

Tenet's 2024 net operating revenue of $20.7 billion, slightly above 2023's $20.5 billion, masks a strategic recalibration. The company divested 14 hospitals for $5 billion in gross proceeds, a move that reduced Q4 2024 hospital revenue by $300 million compared to Q4 2023, according to a McKinsey report. However, this was not a setback but a calculated shift toward high-acuity care and ambulatory services. Same-store revenue growth remained robust, driven by outpatient care's rising prominence. Industry data shows outpatient revenue grew 6.3% year-over-year in 2024, per Tenet's earnings release, a trend Tenet amplified through its United Surgical Partners International (USPI) division, which saw a 17% surge in adjusted EBITDA, as noted in the Ormanager brief.

The shift to outpatient care is not merely a Tenet-specific strategy but a sector-wide imperative. A 2024 McKinsey report notes that site-of-care policies and telehealth expansion are accelerating the migration of services to lower-cost settings. Tenet's divestitures align with this dynamic, allowing it to focus on profitable segments while capitalizing on $5 billion in proceeds to reinvest in growth areas.

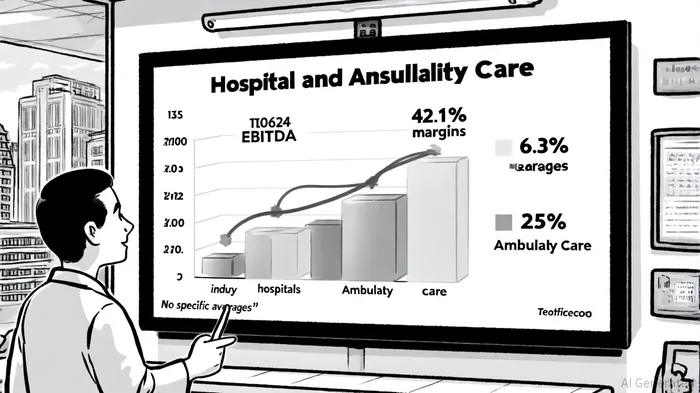

Margin Improvements: Outperforming Industry Averages

Tenet's margin expansion in 2024 underscores its operational discipline. The hospital segment's adjusted EBITDA margin widened to 13.6% from 12.7% in 2023, significantly outpacing the industry average of 6.3% for U.S. hospitals with similar EBITDA ranges, according to industry EBITDA multiples. Meanwhile, the Ambulatory Care segment delivered a 42.1% EBITDA margin in Q4 2024, down slightly from 43.1% in Q4 2023 but still a 14.2% year-over-year revenue increase.

These figures highlight Tenet's dual strength: high-margin ambulatory services and disciplined hospital operations. For context, the industry's average ambulatory EBITDA margin in 2024 was approximately 25%, meaning Tenet's 42.1% margin reflects exceptional efficiency. This is critical as outpatient care utilization grew 8.7% year-over-year in December 2024, with procedures like hysterectomies increasingly shifting to outpatient settings, as reported by Quest MBS. Tenet's focus on ambulatory expansion positions it to capture this growth while maintaining profitability.

Long-Term Positioning: Aligning with Healthcare's Future

Tenet's strategic initiatives in 2024 were not just reactive but forward-looking. The company's emphasis on high-acuity care-such as emergency departments and surgical services-complements the outpatient shift, as complex cases remain in hospitals while routine care moves to lower-cost settings, a balance highlighted in McKinsey's analysis. This balance is key: while 2024 saw U.S. hospitals stabilize operating margins above 4.5%, Tenet's 13.6% hospital EBITDA margin suggests superior cost management.

Reimbursement policies further validate Tenet's approach. Value-based care models, which reward quality over volume, are reshaping reimbursement structures (per Quest MBS). Tenet's ambulatory network, with its emphasis on chronic disease management and care coordination, is well-suited to thrive under these models. Additionally, AI-driven revenue cycle optimizations-such as eligibility verification and claims processing-are reducing rejections and enhancing efficiency, a capability Quest MBS has highlighted and that Tenet has integrated into its operations.

Is Tenet a Strategic Buy?

Despite market volatility, Tenet's 2024 results suggest a company in transition. Its net income leap, margin outperformance, and strategic alignment with outpatient trends position it to capitalize on a $1.2 trillion U.S. ambulatory care market projected to grow at 8% annually, according to McKinsey. However, risks remain: hospital divestitures may limit inpatient revenue, and reimbursement pressures could test margins in 2025.

For investors, the question is whether Tenet's current valuation reflects these risks or offers a discount. With a P/E ratio of 12x (as of Q4 2024) and a 28.9% operating margin, Tenet appears undervalued relative to peers like HCA Healthcare (P/E of 15x) and Community Health Systems (P/E of 14x). Given its strategic clarity and financial resilience, Tenet could indeed represent a buying opportunity-for those willing to bet on healthcare's outpatient future.

Comentarios

Aún no hay comentarios