Why Teladoc Deserves Patience Now: Too Early to Buy, Too Risky to Sell

Teladoc Health, Inc. TDOC is a pioneer and global leader in the telemedicine industry. It has a broad international presence, serving clients, supporting medical operations, and reaching members worldwide. It operates through two main segments — Integrated Care and BetterHelp. It serves markets across North America, South America, Europe, Asia-Pacific and the Middle East.

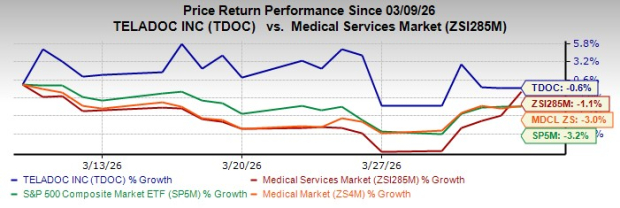

The stock has fallen 0.6% over the past month compared with the industry’s 1.1% decline. The Zacks Medical sector and the S&P 500 composite have decreased 3% and 3.2%, respectively, in the said time frame.

Image Source: Zacks Investment Research

Zack’s Rank and Valuation of TDOC

Teladoc Health currently carries a Zacks Rank #3 (Hold).

From a valuation standpoint, the stock appears to be trading at a discount. With a market capitalization of approximately $940.2 million, the stock has a forward Price-to-Sales ratio of 0.37X, which is below the industry average of 0.44X, indicating a lower valuation compared to its peers. The company currently holds a Value Score of A.

Image Source: Zacks Investment Research

Where Do Estimates for TDOCTDOC-- Stand?

The consensus estimate for 2026 earnings is pegged at 86 cents per share, suggesting anupward revision of 1 cent over the past 30 days. The consensus estimate for 2026 revenues is pegged at $2.5 billion. TDOC beat on earnings in each of the trailing four quarters, delivering an average surprise of 29.4%.

Teladoc Health, Inc. Price, Consensus and EPS Surprise

Business Tailwinds for TDOC

Teladoc Health has evolved from a basic telehealth provider into a more comprehensive healthcare platform. It has expanded services like Primary360 and introduced cardiometabolic and preventive care programs.

Offerings such as Prism and Wellbound allow the company to move beyond one-time consultations toward continuous care. This creates a stronger ecosystem where members are more likely to stay engaged. At the same time, acquisitions like Catapult Health and UpLift are helping build a leaner, more global platform that is approaching a key inflection point for profitability.

Innovation, especially in artificial intelligence, remains central to Teladoc’s strategy. Platforms like Prism and Clarity use AI to highlight recommended screenings and streamline workflows, improving both efficiency and care quality. These tools enable the company to resolve most member concerns in a single visit.

Teladoc is steadily moving beyond simple video consultations to become a more integrated, data-driven clinical partner. Its upcoming AI-based solutions for hospital staff safety also open up higher-margin and B2B revenue opportunities.

TDOC’s growth strategy is balanced between acquisitions and international expansion. While the U.S. market is becoming saturated, international revenues continue to grow at a solid pace, rising 12% in 2025 and outperforming domestic growth. The transition of BetterHelp toward an insurance-based model is expected to unlock additional revenue streams. Recent acquisitions further strengthen Teladoc’s capabilities and expand its global reach.

On the financial side, TeladocTDOC-- is showing improved discipline. Total expenses declined 22.2% year over year in 2025, driven by workforce optimization and a reduced real estate footprint. This has helped protect margins and support Adjusted EBITDA, which is projected to reach up to $308 million in 2026. Overall, these efforts point to a clearer and more credible path toward profitability.

Key Risks to Consider

Despite its growth potential, there are a few concerns that investors should consider.

The BetterHelp segment, once a key growth driver for Teladoc HealthTDOC--, has become a concern. In 2025, segment revenues declined 9%. Although the company is shifting toward an insurance-reimbursed model to improve affordability, the transition is still in its early stages. If this move does not offset ongoing churn in the market, the segment could continue to weigh on overall valuation.

TDOC faces rising competition in the virtual care space from major players, which could put pressure on pricing. Profit remains volatile, with an accumulated deficit of $16.4 billion as of 2025, caused by heavy investments in customer acquisition, provider networks and technology development.

Conclusion

Given the mix of positives and risks, a wait-and-see approach appears prudent for Teladoc Health. Investors may want to closely track progress on profitability, stabilization in the BetterHelp segment, and overall growth trends before making a decisive move.

Key Picks

Some better-ranked stocks in the broader Medical sector are Phibro Animal Health Corporation PAHC, Catalyst Pharmaceuticals, Inc. CPRX and InnovAge Holding Corp. INNV, each sporting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Phibro Animal Health's 2026 earnings is pegged at $3.03 per share, which moved up 1 cent over the past 30 days, indicating 45% year-over-year growth. The consensus estimate for 2026 revenues is pinned at $1.5 billion, indicating 14.5% year-over-year growth. PAHC beat earnings estimates in each of the trailing four quarters, delivering an average surprise of 20.2%.

The Zacks Consensus Estimate for Catalyst Pharmaceuticals’ 2026 earnings is pinned at $2.87 per share, which moved north 5 cents over the past 30 days. CPRX beat earnings estimates in each of the trailing four quarters, delivering an average surprise of 35.2%. The consensus estimate for 2026 revenues is pegged at $628.7 million, suggesting 6.7% year-over-year growth.

The Zacks Consensus Estimate for InnovAge's 2026 earnings is pegged at 25 cents per share, which has remained stable over the past 30 days, indicating 213.6% year-over-year growth. The consensus estimate for 2026 revenues is pinned at $944.5 million, indicating 10.6% year-over-year growth. INNV beat earnings estimates in three of the trailing four quarters and missed once, delivering an average surprise of 87.5%.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Catalyst Pharmaceuticals, Inc. (CPRX): Free Stock Analysis Report

Phibro Animal Health Corporation (PAHC): Free Stock Analysis Report

Teladoc Health, Inc. (TDOC): Free Stock Analysis Report

InnovAge Holding Corp. (INNV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios