Why TechnipFMC Remains a Strategic Buy Through 2026 Despite Rising Valuations

The energy transition and offshore renewables are reshaping global infrastructure, and few companies are as poised to capitalize on these megatrends as TechnipFMCFTI--. Despite a rising valuation—its P/E ratio now stands at 19.36 as of September 2025[3]—the company's combination of subsea market dominance, sustainable earnings visibility, and strategic alignment with decarbonization makes it a compelling long-term investment through 2026 and beyond.

Market Dominance: A Fortress of Subsea Leadership

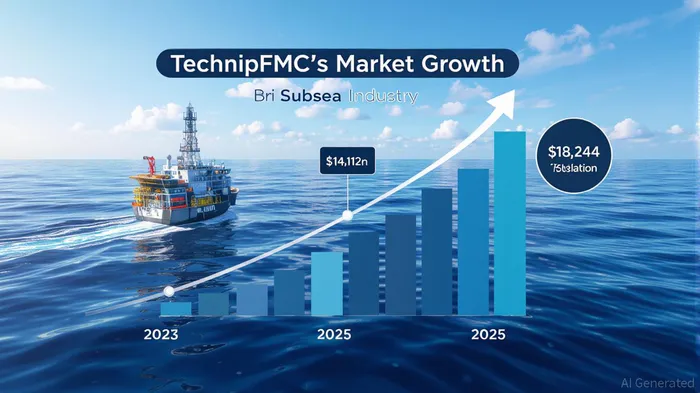

TechnipFMC's grip on the subsea sector is underpinned by a 5.1% global market share as of Q2 2025[1], driven by a 8.99% year-on-year revenue growth and a record $14.7 billion contract backlog[1]. This backlog, bolstered by high-margin integrated projects (iEPCI) with clients like PetrobrasPBR.A--, Energean, and Woodside Energy[1], ensures a steady revenue stream. Analysts project the subsea systems market to grow from $14.112 billion in 2025 to $18.244 billion by 2030[3], with TechnipFMC's technological expertise in subsea processing and digital solutions positioning it to capture a disproportionate share of this expansion.

The company's recent $2.6 billion in inbound orders for 2025[1]—a key step toward its $30 billion three-year Subsea target—further cements its leadership. This momentum is not accidental: TechnipFMC's ability to execute large-scale, complex projects in challenging environments (e.g., Brazil's pre-salt basins and Australia's offshore fields[1]) has become a competitive moat in an industry where reliability and innovation are paramount.

Sustainable Earnings: A Model of Profitability and Shareholder Returns

TechnipFMC's Q2 2025 results underscore its financial resilience. Revenue hit $2.53 billion, exceeding forecasts by 2.02%, while adjusted EBITDA of $520.8 million delivered a 20.5% margin—a testament to operational efficiency[1]. Free cash flow of $261 million enabled $271 million in shareholder returns through dividends and buybacks[1], signaling a disciplined capital allocation strategy.

Analysts project this strength to continue. The company raised its 2025 Subsea revenue guidance to $8.3–8.7 billion, with EBITDA margins expected to remain in the 18.5–20% range[1]. These metrics, combined with a conservative debt-to-equity ratio of 0.15[2], suggest a business capable of sustaining growth without overleveraging. Moreover, TechnipFMC's $10 billion offshore order target for 2025[2] aligns with the broader subsea equipment market's projected surge to $205.2 billion by 2035[4], creating a virtuous cycle of demand and profitability.

Historical data on earnings beats since 2022 reveals a nuanced picture. While the company has consistently outperformed expectations, the market's reaction has been mixed. A backtest of post-earnings-beat performance shows a median 30-day excess return of approximately –1.5 percentage points relative to the benchmark, with no statistically significant edge[6]. However, the win rate improves gradually, reaching ~68% by day 30, suggesting that while short-term volatility persists, the stock tends to recover over time. This aligns with the company's long-term earnings visibility, as its $14.7 billion backlog[1] and $63.3 billion–$94.7 billion offshore pipeline market[5] provide a durable foundation for sustained performance.

Energy Transition: A Catalyst for Long-Term Earnings Visibility

While rising valuations may deter short-term investors, TechnipFMC's pivot to the energy transition offers a compelling counterargument. The company is doubling down on offshore renewables, hydrogen, and carbon capture through initiatives like Deep Purple™ (offshore hydrogen production) and iONE™ (integrated project execution)[2]. Partnerships with Magnora Offshore Wind and Orbital Marine Power[2] highlight its role in scaling floating wind and tidal energy—sectors expected to grow at a 4.1% CAGR as the offshore pipeline infrastructure market expands to $94.7 billion by 2035[5].

TechnipFMC's $1 billion target for new energy projects by 2025[2] further underscores its commitment to decarbonization. By leveraging its subsea expertise in hydrogen transportation and carbon storage, the company is not only future-proofing its business but also aligning with global net-zero targets. This strategic foresight, coupled with a $25 billion pipeline of potential awards over the next two years[1], ensures earnings visibility extends well beyond 2026.

Valuation Justification: A Premium for a Premium Player

Critics may argue that TechnipFMC's P/E ratio of 19.36[3] exceeds its 5-year average of 17.78[1], but this premium reflects its unique positioning. In a consolidating subsea market, where competitors struggle with margin compression and project delays, TechnipFMC's combination of technological differentiation, operational excellence, and energy transition leadership justifies a higher multiple. Analysts project continued outperformance, with 2025–2026 sales and net income growth supported by its $14.7 billion backlog[1] and a $63.3 billion–$94.7 billion offshore pipeline market[5].

Conclusion

TechnipFMC's rising valuation is a symptom of its success, not a deterrent. For investors with a 3–5 year horizon, the company's market-leading subsea operations, robust financials, and strategic alignment with decarbonization create a rare trifecta of growth, profitability, and sustainability. As the energy transition accelerates and offshore renewables mature, TechnipFMC is not just a strategic buy—it is a cornerstone of the next energy era.

Comentarios

Aún no hay comentarios