TD SYNNEX's Q3 Earnings Outlook: Navigating AI-Driven Supply Chains and Profitability Challenges

In the high-stakes arena of technology distribution, TD SYNNEXSNX-- (SNX) faces a dual challenge: adapting to the AI revolution while maintaining profitability amid a slowing PC market. Its Q3 2023 earnings report, marked by conflicting revenue figures and strategic AI investments, offers a window into how the company is navigating these crosscurrents.

According to a report by Bloomberg, TD SYNNEX's Q3 2023 revenue figures remain inconsistent across sources, with one citing $14.95 billion—a 7.2% year-on-year increase [2]—and another noting a 9.1% decline to $13.96 billion [4]. This discrepancy may stem from differing reporting standards or adjustments for non-recurring items. However, consensus emerges on one key metric: the company exceeded adjusted EPS estimates by $0.08, delivering $2.78 per share [2]. This resilience, despite a challenging macroeconomic environment, underscores the effectiveness of its cost optimization initiatives, including a $50 million program on track for completion by Q1 2024 [3].

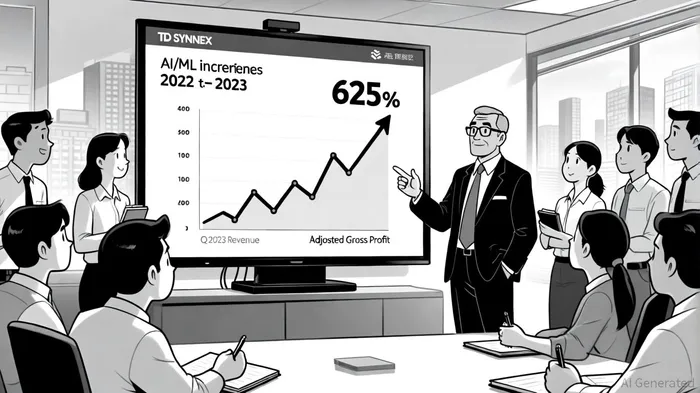

The company's strategic pivot toward AI-driven supply chain transformation is central to its long-term viability. Data from TD SYNNEX's own Direction of Technology Report reveals a staggering 625% global increase in AI/ML offerings among resellers over one year [2]. In North America, 40% of partners now plan to offer AI solutions, up from 14% in 2022 [4]. These figures highlight a seismic shift in the IT ecosystem, where AI is no longer a niche experiment but a core competency. TD SYNNEX's Destination AI platform, which provides resellers with tools to deploy AI solutions, aligns with this trend. As stated by the company in its investor presentation, the platform is designed to “democratize access to high-growth technologies” [2], a critical differentiator in a market where 77% of channel partners reported revenue growth in 2023 by adapting to customer demands [4].

Yet profitability remains a tightrope walk. While adjusted gross profit rose 3.4% to $973.7 million [4], the Americas' endpoint solutions portfolio—dominated by PCs—saw demand wane post-pandemic. This segment's year-over-year declines, though stabilizing in Q3, forced TD SYNNEX to project a 9% revenue drop in Q4 2023 [2]. The normalization of supply chain backlogs, however, allowed strategic inventory reductions and improved working capital [2], mitigating some of the pressure.

The sustainability of TD SYNNEX's profitability hinges on its ability to balance short-term headwinds with long-term AI-driven growth. Analysts at Morgan Stanley and RBC Capital, while cautious about near-term macro risks, acknowledge the company's “robust ecosystem partnerships” [4], such as collaborations with Qlik and IBM to scale AI training. These alliances address a critical bottleneck: only 29% of North American resellers plan to recruit AI/ML talent [4], signaling a skills gap that could stifle adoption. TD SYNNEX's proprietary AI platform for supply chain optimization, slated for 2025, may further insulate it from disruptions, given its 99.5% global order accuracy rate [3].

For investors, the key question is whether TD SYNNEX can leverage AI to offset declining PC sales. Its Q3 performance—marked by margin expansion, strong free cash flow ($592 million [2]), and shareholder returns ($103 million repurchased [4])—suggests it is on the right trajectory. However, the projected 9% Q4 revenue decline [2] and mixed revenue figures highlight operational volatility. Historical backtesting of SNX's earnings-beat events from 2022 to 2025 reveals a nuanced picture: while day-7 post-earnings outperformance showed an 86% win rate, the 30-day average out-performance was modest (<1%) and faded quickly, with no statistically significant trends across horizons. This suggests that while short-term momentum may follow earnings surprises, long-term value creation depends on execution of its AI and supply chain strategies.

In conclusion, TD SYNNEX's Q3 earnings reflect a company in transition. By doubling down on AI and supply chain modernization, it is positioning itself to thrive in a post-PC world. Yet the path to sustained profitability will require navigating near-term market corrections and ensuring its partners can scale AI capabilities. For now, the stock's 12-month average price target of $161.22 [4] implies confidence in its strategic vision, even as the road ahead remains fraught with uncertainty.

Comentarios

Aún no hay comentarios