TaskUs' Abandoned Take-Private Deal: A Case Study in Shareholder Power and M&A Realities

The collapse of TaskUsTASK--, Inc.'s proposed $16.50-per-share take-private deal in October 2025 underscores a pivotal shift in corporate governance dynamics and investor risk assessment. This case study reveals how institutional shareholders, proxy advisory firms, and governance frameworks are reshaping the landscape of leveraged buyouts, particularly in high-growth sectors like AI-driven services.

Shareholder Resistance and Valuation Disputes

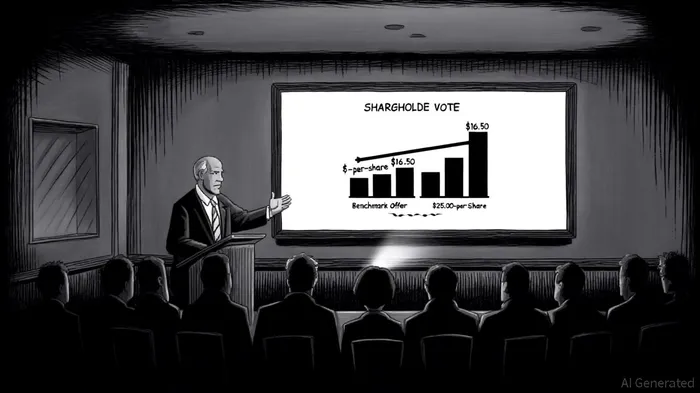

The deal, spearheaded by BlackstoneBX--, TaskUs co-founders, and key executives, was rejected by public stockholders at a 12-to-1 ratio, with 10,064,296 votes against versus 840,473 in favor, according to Panabee's TaskUs Stockholders Decisively Reject Take-Private Merger. This outcome reflects a stark disconnect between the Buyer Group's valuation and investor expectations. Think Investments, a major dissenting shareholder, argued the offer undervalued TaskUs by over 50%, citing a fair price of $25.00 per share, as the Panabee coverage noted. The firm highlighted the omission of relevant precedents, such as Capgemini's acquisition of WNS, which would imply a 12x LTM EBITDA multiple-far exceeding the fairness opinion's 6.8x median (per the Panabee article).

Proxy advisory firms amplified this skepticism. Institutional Shareholder Services (ISS) explicitly recommended rejecting the deal, emphasizing the valuation gap and urging revisions to compensate unaffiliated shareholders. Such recommendations carry significant weight, as ISS's influence on institutional voting behavior has been a focal point of regulatory debates, underscored by a House hearing testimony.

Corporate Governance and Fiduciary Dynamics

TaskUs' Board of Directors, including CEO Bryce Maddock and Co-Founder Jaspar Weir, maintained that the transaction aligned with long-term strategic goals, particularly AI integration in digital services, a position that ISS nevertheless questioned in its recommendation. However, the Special Committee's insistence on the deal clashed with investor demands for transparency. The board's governance guidelines, while emphasizing fiduciary responsibility, failed to address concerns over the sale process's fairness, a point highlighted in the Panabee coverage.

This tension highlights a broader trend: boards increasingly face scrutiny over their independence in self-dealing transactions. The TaskUs case demonstrates how minority shareholders can leverage proxy contests and advisory firm support to challenge control shifts, even when insider groups hold substantial stakes, as noted in TaskUs' results announcement.

M&A Implications: A New Era of Shareholder Scrutiny

The failed deal signals a recalibration of M&A risk assessment in 2025. For leveraged buyouts in the outsourcing sector, three key lessons emerge:

1. Valuation Precision: Acquirers must justify premiums against robust peer and precedent analyses. TaskUs' AI Services segment, which grew 65.5% YoY in H1'25 (reported in the Panabee coverage), exemplifies how high-growth assets demand higher multiples.

2. Shareholder Alignment: Deals requiring minority approval now face heightened hurdles. The absence of termination fees in TaskUs' agreement-despite months of proxy solicitation-underscores the financial risks of underestimating investor resistance, a point emphasized by ISS in its recommendation.

3. Regulatory and Governance Risks: Proxy advisory firms' growing influence complicates deal execution. Critics argue their opaque methodologies create conflicts of interest, yet their recommendations remain pivotal in shaping voting outcomes, as discussed in House hearing testimony.

Strategic Investor Takeaways

For investors, the TaskUs saga reinforces the importance of proactive engagement in governance and deal risk assessment. Key strategies include:

- Leveraging Proxy Advisors: Aligning with ISS or Glass Lewis can amplify dissent in contested transactions.

- Valuation Arbitrage: Identifying undervalued assets in AI-driven sectors, where growth metrics (e.g., TaskUs' AI Services) justify premium pricing.

- Board Accountability: Advocating for independent committees in self-tender offers to mitigate conflicts of interest.

- Timing of Entry: Historical data suggests that a buy-and-hold strategy initiated post-shareholder meetings tends to show positive returns only after 22-30 days, with an average cumulative abnormal return of +15% by day 30, according to the Panabee piece. Short-term (≤5 days) price movements show no significant directional bias, but the win rate improves to ~90% by day 30. Investors should consider holding positions for at least a month to capture potential upside.

As TaskUs pivots to an AI-centric strategy post-deal, the broader market will watch closely. The company's ability to capitalize on its digital services expertise-without the liquidity constraints of a private structure-may yet validate the skepticism that derailed the buyout. For now, the case serves as a cautionary tale: in an era of empowered shareholders, even well-connected buyout groups must earn their deals.

Comentarios

Aún no hay comentarios