US Tariff Surge Sparks Surplus, But Debt Crisis Looms: Navigating Fiscal Crosscurrents

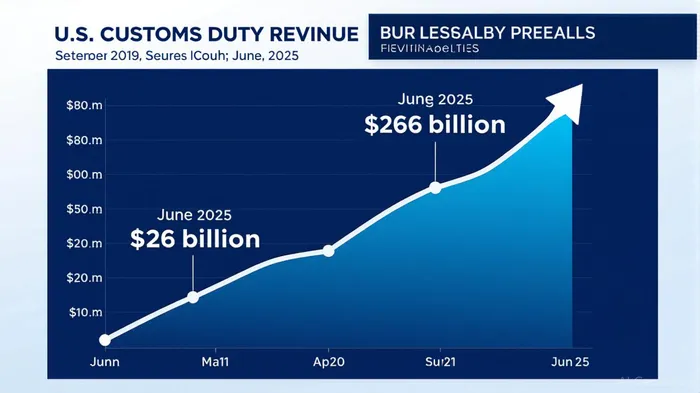

The U.S. Treasury's June 2025 report revealed an unexpected $27 billion federal budget surplus—the first monthly surplus in over five years—driven by record tariff revenues of $26.6 billion. This figure, nearly four times higher than June 2024's $6.6 billion, marks a dramatic pivot in fiscal policy. Yet, beneath the headline numbers lies a precarious dynamic: tariffs are fueling short-term revenue gains, but the $1.3 trillion annual deficit and $36.6 trillion national debt remain unresolved. For investors, this creates a paradoxical landscape—opportunities in sectors benefiting from tariff-driven spending, yet risks from the unresolved structural deficit.

The Tariff Tax Machine: A Temporary Lifeline

President Trump's aggressive tariff agenda—imposing 50% levies on Brazilian copper, 35% tariffs on Canadian goods, and plans for sector-specific duties on semiconductors and pharmaceuticals—has turned tariffs into the federal government's fourth-largest revenue source, accounting for 5% of total receipts (up from 2% in 2024). The June surplus was partly due to accelerated payments shifted to May (June 1 fell on a Sunday), but tariffs were the unsung hero.

The Treasury now projects tariff revenues could hit $300 billion by December 2025—nearly double 2024's $168 billion. If achieved, this would reduce reliance on debt issuance and lower interest costs, which alone consumed $921 billion in the first nine months of FY2025. However, analysts caution that tariffs' growth may stall as businesses adjust. Yale economist Ernie Tedeschi notes, “Front-loaded revenue gains could fade as companies shift supply chains or consumers absorb higher prices.”

Structural Deficits: The Elephant in the Room

Despite June's surplus, the fiscal year-to-date deficit through September 30, 2025, is still projected to hit $1.9 trillion—up 5% from 2024. Non-tariff revenue growth (e.g., income taxes) has stalled, while spending on healthcare, Social Security, and defense continues to climb. Meanwhile, the national debt now exceeds $36.6 trillion, with interest costs alone projected to hit $1.2 trillion in 2025.

The Congressional Budget Office (CBO) estimates that even if tariffs reach $300 billion, the decade-long deficit would still total $2.8 trillion—a fraction of the $36 trillion debt. As climbs above 120%, the risk of a fiscal reckoning grows.

Equity Market Implications: Play the Surge, Avoid the Surge

Investors should adopt a dual strategy: capitalize on tariff-driven sectors while hedging against fiscal uncertainty.

- Overweight Sectors Benefiting from Tariff Inflows:

- Defense & Logistics: Tariffs have boosted spending on military infrastructure (e.g., $1.3 trillion defense budget) and logistics firms handling increased trade volumes.

Copper & Metals: Companies like Freeport-McMoRanFCX-- (FCX) benefit from tariffs on Brazilian imports, though risks persist if global trade wars escalate.

Underweight Rate-Sensitive Equities:

- Tech & Consumer Discretionary: High multiples in sectors like semiconductors (e.g., AMDAMD--, NVDA) could crumble if tariffs trigger inflation or higher interest rates.

- Real Estate: Rising borrowing costs linked to fiscal tightening could pressure REITs and homebuilders.

The Bottom Line: A Fiscal High-Wire Act

The June surplus is a temporary triumph, not a solution. Tariffs have temporarily masked the deficit's growth, but without entitlement reforms or tax hikes, the $36 trillion debt will eventually demand austerity. Investors should treat tariff-driven gains as a tactical opportunity while preparing for volatility when fiscal reality resurfaces.

Recommendation: Maintain a 15% overweight in defense and logistics stocks, but keep 20% of equities in cash or short-term Treasuries to weather potential fiscal turbulence.

The tariff boom is a siren song—investors must heed the structural deficit's warning.

Comentarios

Aún no hay comentarios