Tanger (SKT): A Quality REIT at a Fair Price Amid Downgrade and Strategic Moves

Tanger Inc. (NYSE: SKT) has navigated a turbulent retail real estate landscape with resilience, even as recent credit spread widening and macroeconomic headwinds have cast a shadow over its investment-grade profile. For income-focused investors, the question remains: Is SKTSKT-- a compelling opportunity at its current valuation, or does its downgraded risk profile justify caution?

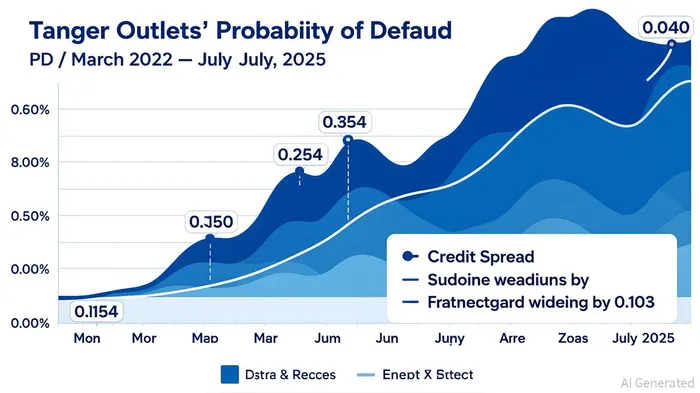

Credit Risk: A Mixed Bag of Macro Sensitivity and Operational Resilience

Tanger's credit profile remains a tug-of-war between macroeconomic vulnerabilities and operational strengths. As of July 2025, the company's probability of default (PD) has recovered to 0.040, a marked improvement from the 0.254 peak in April 2023[1]. However, its credit spread has widened by 0.103, placing it in the top 49th percentile of the bond universe in terms of risk[1]. This divergence highlights a critical nuance: while Tanger's fundamentals have stabilized, market sentiment remains cautious.

The company's exposure to external factors is a double-edged sword. A negative correlation with the S&P 500 (-0.425) means rising equity markets could bolster its creditworthiness[1]. Conversely, a stronger U.S. dollar (positive exposure of 0.331) and rising oil prices (0.160) pose risks[1]. These sensitivities underscore the importance of macroeconomic trends in shaping Tanger's credit trajectory.

Financial Performance: Strong Leasing and Guidance Uplift

Despite these risks, Tanger's operational execution has been robust. For Q2 2025, the company reported core FFO of $0.58 per share, exceeding expectations and driving a revised full-year guidance range of $2.24–$2.31 per share[2]. Same-center net operating income (NOI) grew by 5.3% year-over-year, and occupancy rates held steady at 96.6%[2]. These metrics reflect disciplined leasing and a focus on high-traffic outlet centers, which remain resilient amid broader retail sector struggles.

Institutional ownership also provides a tailwind, with Vanguard Group and Northern TrustNTRS-- increasing stakes in Q1 2025[2]. However, the 39.3% stake reduction by Vident Advisory LLC and a 5.2% trimming by Raymond James FinancialRJF-- Inc. signal caution among some investors[2].

Notably, a backtest of SKT's performance following earnings beats since 2022 reveals a 71% win rate within 30 days, peaking on day 8, though excess returns remain statistically insignificant. This suggests that while Tanger's operational strength drives positive guidance, the market does not consistently reward these events with sustained price momentum. Investors should focus on long-term fundamentals rather than short-term volatility.

Strategic Moves: Diversification and Margin Expansion

Tanger's long-term strategy to mitigate risk includes a pivot toward mixed-use properties and higher-margin developments. By diversifying its tenant base and integrating residential and commercial spaces, the company aims to reduce reliance on discretionary retail spending[1]. This approach aligns with broader industry trends, as outlet centers increasingly serve as anchors for lifestyle-driven destinations.

Moreover, Tanger's dividend yield of 3.4% remains attractive in a rising interest rate environment[2]. While the payout ratio appears sustainable given its 96.6% occupancy and $101.7 million Q2 NOI[2], investors should monitor leverage metrics as the company executes its growth plans.

Valuation and Peer Comparison: A Fair Price Amid Sector Volatility

Tanger's valuation appears reasonable when compared to peers. Its Z-spread of 1.2% places it below the average range of 0.678%–13.969% for the period August 2021–July 2025[1], suggesting it trades at a discount relative to its historical risk profile. While credit spreads have widened, the company's BBB- (S&P) and Baa3 (Moody's) ratings[3] indicate a stable, investment-grade foundation.

However, TangerSKT-- lags peers like Pine Tree, which has seen credit spread tightening[1]. This gap highlights the need for continued execution on cost controls and tenant diversification to close the performance divide.

Conclusion: A Quality REIT for Patient Investors

Tanger Outlets is not without risks—its macroeconomic sensitivities and recent credit spread widening warrant careful monitoring. Yet, its strong operational performance, strategic diversification, and attractive dividend yield position it as a quality REIT at a fair price. For investors with a medium-term horizon and a tolerance for sector volatility, SKT offers a compelling blend of income and growth potential.

As always, the key lies in balancing the company's credit profile with its execution capabilities. With a positive outlook from S&P and Fitch[3], and a management team focused on margin expansion, Tanger's story is far from over.

Comentarios

Aún no hay comentarios