Systemic Vulnerabilities in Alternative Credit Strategies: A Cautionary Outlook for Institutional Investors

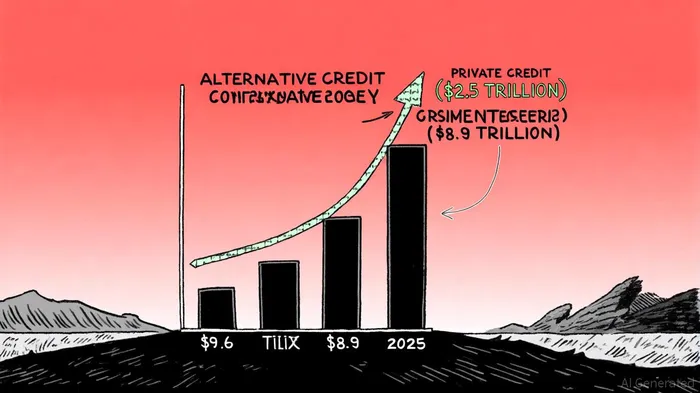

Institutional investors have increasingly turned to alternative credit strategies to diversify away from traditional fixed-income assets, driven by the allure of higher yields and uncorrelated returns. By 2025, alternative credit has ballooned to $9.6 trillion, surpassing the investment-grade corporate credit universe, according to a WTW report. However, this rapid expansion has introduced systemic vulnerabilities that demand closer scrutiny. As private credit-a subset of alternative credit-now rivals traditional bank lending and public debt markets, a CFA Institute post warns, its opaque structures, high leverage, and sector-specific risks are amplifying corporate bankruptcy exposures for institutional portfolios.

Leverage and Liquidity: A Double-Edged Sword

Private credit funds, including business development companies (BDCs) and direct lending vehicles, have grown into a $2.5 trillion industry, the CFA Institute notes. These strategies often employ high leverage to amplify returns, with some BDCs raising leverage caps to levels that regulators now view as precarious, the CFA Institute adds. For instance, subscription credit facilities and note-on-note financings-tools used to optimize capital deployment-have increased the fragility of private credit portfolios, as a National Law Review article explains. When combined with the sector's limited liquidity, this creates a perfect storm: during economic downturns, funds may struggle to roll over maturing debt or access central bank liquidity, which is typically reserved for traditional financial institutions, the CFA Institute warns.

The Federal Reserve and the International Monetary Fund (IMF) have flagged this as a systemic risk, particularly as private credit's interconnectedness with traditional banks grows. Many private credit funds rely on bank funding lines, and if these institutions extend riskier loans or overleverage their balance sheets, the entire financial system could face contagion, WTW notes.

Transparency and Valuation Challenges

Alternative credit's opacity is another critical vulnerability. Unlike public bonds, private loans are not traded on open markets, making valuations subjective and prone to mispricing. This lack of transparency becomes especially problematic during crises, when asset values plummet and redemption pressures mount, the CFA Institute observes. For example, Canadian institutional funds, which allocate up to 11% of their portfolios to alternative credit, face heightened risks if their private debt holdings are overvalued or concentrated in high-yield sectors, Nuveen finds. Foundations, too, are exposed: 5% of their assets are often tied to private debt and real asset financing, which may lack the safeguards of public markets, Nuveen reports.

Sector-Specific Vulnerabilities

High-yield debt, emerging market credit, and infrastructure financing-popular segments of alternative credit-are particularly susceptible to corporate bankruptcy risks. High-leverage firms in these sectors face amplified vulnerability in competitive banking environments, especially after deregulation, WTW observes. For instance, the recent rate-hike cycle has increased borrowing costs for private equity-backed companies, which are often highly leveraged and sensitive to interest rate fluctuations, Nuveen says. Infrastructure projects, meanwhile, rely on long-term cash flows that could be disrupted by economic shocks or regulatory shifts.

Regulatory Scrutiny and the Path Forward

Regulators are beginning to act. The SEC has intensified its focus on private credit firms, probing valuation practices, conflicts of interest in bank partnerships, and disclosures to retail investors, the National Law Review reported. The Fed and BIS have also called for stricter oversight to mitigate systemic risks, the CFA Institute outlines. However, these efforts lag behind the pace of market growth. As WTW notes, 27% of fixed-income portfolios are now allocated to alternative credit, a share that is expected to rise further in 2025.

For institutional investors, the challenge lies in balancing the benefits of alternative credit-diversification, income generation-with its inherent risks. Diversifying across sectors and leveraging sophisticated risk management tools may help, but the sector's structural weaknesses-leverage, liquidity constraints, and valuation opacity-remain unresolved.

Conclusion

Alternative credit strategies have redefined institutional investing, but their systemic risks cannot be ignored. As the market continues to expand, investors must weigh the promise of higher returns against the potential for corporate bankruptcies, liquidity crises, and regulatory backlash. The coming years will test whether this asset class can evolve into a stable pillar of institutional portfolios-or if its vulnerabilities will trigger a broader financial reckoning.

Comentarios

Aún no hay comentarios