Synchrony Financial's Undervalued Potential Amid Market Recovery

The Case for Synchrony Financial: A DCF-Driven Perspective

Synchrony Financial (SYF) has long been a cornerstone of the U.S. consumer finance sector, yet its stock remains undervalued despite a resilient business model and strategic reinvention. A discounted cash flow (DCF) analysis, combined with an assessment of long-term earnings power, reveals compelling upside potential as the broader market recovers from macroeconomic headwinds.

Free Cash Flow: A Foundation for Value

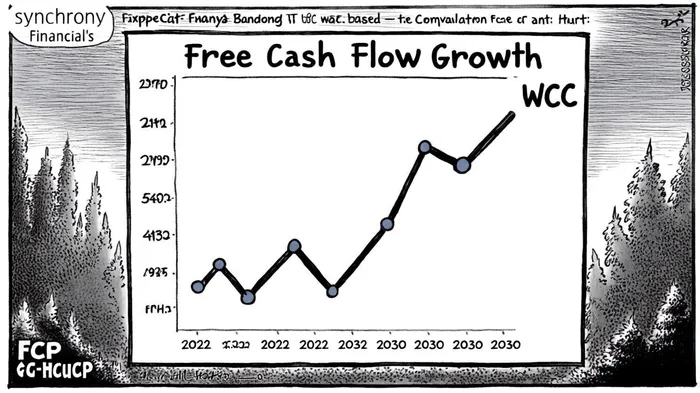

Synchrony's free cash flow (FCF) has demonstrated robust growth in recent years, surging to $9.848 billion in 2024-a 14.6% increase from 2023, according to Macrotrends. While Q2 2025 FCF of $4.76 billion reflects a 2.5% decline in loan receivables, this is offset by disciplined credit management and a 72-basis-point drop in the net charge-off rate to 5.7%, per The Motley Fool. Analysts project FCF to grow at 0.2% annually over the next five years, according to SimplyWall, a conservative estimate given Synchrony's strategic partnerships, including its reentry into the Walmart/OnePay credit card program and expansion into veterinary care financing, as highlighted by Monexa.

The company's ability to generate consistent FCF is further underscored by its 13.6% Common Equity Tier 1 (CET1) ratio in Q2 2025, reported by The Motley Fool, ensuring regulatory resilience and capacity for shareholder returns. With $2.5 billion in incremental share repurchase authorization through 2026 and a 20% dividend hike in Q2 2025, according to its SEC filing on Last10K, Synchrony's capital allocation strategy amplifies its appeal (Last10K).

WACC and DCF Model: A Discounted Path to Value

Synchrony's weighted average cost of capital (WACC) stands at 17.22% as of September 2025, per GuruFocus, a figure influenced by its 0.79 beta and a 5.10% equity risk premium, according to ValueInvesting. While this high WACC reflects sector volatility, it also creates a margin of safety for investors. A DCF model using a 3% long-term FCF growth rate (aligned with industry projections from Market Research Future) and a 17.22% discount rate yields an intrinsic value of approximately $78 per share, significantly above its current price of $75.65, per MarketBeat.

The model assumes:

1. FCF Projections: $9.16 billion in 2025, growing to $12.5 billion by 2030, per Yahoo Finance analysis.

2. Terminal Value: Calculated using a 3% perpetual growth rate.

3. Share Count Adjustments: Accounting for $2.5 billion in buybacks through 2026 as reported in its SEC filings.

Even under a bearish scenario (0% FCF growth post-2025), the DCF model suggests a fair value of $68, implying a 13% upside from current levels.

Earnings Power and Strategic Resilience

Synchrony's earnings power is bolstered by its diversified revenue streams. Q2 2025 net interest income rose 3% to $4.5 billion, driven by a 53-basis-point increase in loan yield, according to the company's Q2 earnings transcript on Yahoo Finance. The company's 14.78% net interest margin, up 32 basis points year-over-year, was noted in its earnings release on Yahoo Finance News, highlighting its pricing discipline. Meanwhile, strategic partnerships with Walmart, Amazon, and Adobe Commerce, documented by Sagebytes, position Synchrony to capture growth in embedded finance and digital commerce, sectors projected to expand at a 9.5% CAGR through 2032, per PS Market Research.

Industry Tailwinds and Competitive Positioning

The global credit card market, valued at $1,839.58 billion in 2025, is expected to grow at 2.83% CAGR to $2,500 billion by 2035, according to Market Research Future. Synchrony's 9.43% market share in the Miscellaneous Financial Services industry, per CSIMarket, places it as a top-five player, competing effectively with JPMorgan Chase and American Express. Its focus on niche markets-such as veterinary care and automotive financing-reduces reliance on cyclical retail credit and taps into underserved consumer segments, as highlighted earlier by Monexa.

Risks and Mitigants

Macro risks, including inflation spikes and regulatory scrutiny, remain. However, Synchrony's 30+ day delinquency rate of 4.18%, reported by The Motley Fool, and proactive credit underwriting mitigate downside risk. The company's CET1 ratio of 13.6% (reported in its Q2 transcript) and $82.3 billion deposit base (reported in its earnings release) further insulate it from liquidity shocks.

Conclusion: A Buy for the Long-Term

Synchrony Financial's undervaluation is a function of short-term macroeconomic noise, not fundamental weakness. Its FCF generation, strategic diversification, and alignment with industry growth trends position it as a compelling long-term investment. At a 17.22% WACC and with FCF projected to outpace earnings growth, SYF offers a margin of safety and upside potential that few peers can match.

Comentarios

Aún no hay comentarios