Succession and Strategy Shifts in U.S. Equities Research: Leadership Transitions and Market Dynamics

The U.S. equities research landscape in 2025 is undergoing a profound transformation, driven by strategic recalibrations and leadership transitions at major financial institutionsFISI--. These shifts reflect a broader industry response to macroeconomic volatility, technological disruption, and evolving investor demands. As firms like Goldman SachsGS--, JPMorganJPM--, and BlackRockBLK-- realign their priorities, the implications for investment strategies and market dynamics are becoming increasingly pronounced.

Leadership Transitions and Strategic Realignment

Goldman Sachs' January 2025 leadership reshuffle exemplifies this trend. By appointing Kunal Shah and Anthony Gutman as co-CEOs of GoldmanGS-- Sachs International, the firm signaled a commitment to leveraging experienced leadership in volatile markets[1]. This move aligns with a sector-wide preference for older, seasoned executives, as the average age of incoming CEOs in 2024 reached 55.7[1]. Goldman's strategic focus on private credit and international markets underscores its ambition to expand into high-growth sectors while reinforcing its global competitiveness[5]. Similarly, JPMorgan's promotion of Jennifer Piepszak to COO and the appointment of Co-CEOs for its Commercial & Investment Bank reflect a deliberate effort to enhance operational efficiency and leadership continuity[4]. These changes are paired with physical expansion into high-wealth markets and digital innovation, such as virtualCYBER-- advisory services[3].

BlackRock and Vanguard have also navigated significant leadership transitions. Vanguard's appointment of Salim Ramji, its first external CEO, marks a departure from internal succession norms, bringing expertise in investment management and wealth advisory[2]. Meanwhile, BlackRock's strategic pivot toward diversification—emphasizing liquid alternatives, international equities, and AI-driven nowcasting—highlights its response to investor concerns over concentration risks and valuation pressures[3].

Market Dynamics: Beyond the "Magnificent 7"

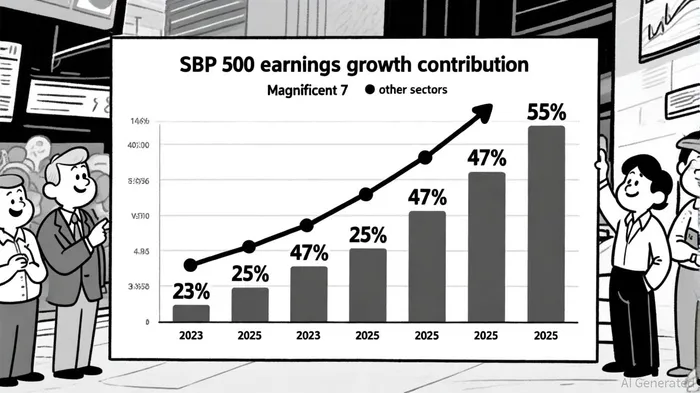

The strategic shifts at these firms are not occurring in isolation. The U.S. equity market itself is witnessing a broadening of leadership. In 2023, the "Magnificent 7" accounted for 63% of S&P 500 earnings growth, but this share fell to 47% by mid-2024[3]. This decline, while not signaling the end of the tech giants' dominance, reflects growing opportunities in sectors like healthcare, industrials, and energy. For instance, JPMorgan's Spring 2025 outlook notes that AI and energy transition spending are fueling diversification, with non-tech firms leveraging technology to enhance profitability[4]. BlackRock's advocacy for low-volatility strategies and defensive equities further underscores the need for portfolios to adapt to a more fragmented market[2].

However, challenges persist. Fiducient warns of "full valuations, concentration risks, and potential reinflation," urging a shift toward active management and alternatives to mitigate fragility[5]. This caution is echoed by Aswath Damodaran, who observes that traditional value and small-cap premiums are no longer delivering expected returns, with momentum increasingly concentrated in a narrow set of stocks[1].

The Role of Research Methodologies

Leadership changes have also spurred methodological innovations in equities research. Goldman Sachs' elevation of leaders with expertise in private credit and institutional fintech signals a shift toward alternative asset coverage[1]. Similarly, JPMorgan's integration of high-frequency data and real-time insights into its research frameworks reflects a broader industry trend toward agility and responsiveness[4]. These changes are critical in an environment where geopolitical risks, such as new tariffs, and technological disruptions demand rapid recalibration[3].

Conclusion

The interplay between leadership transitions and strategic shifts in U.S. equities research is reshaping both institutional approaches and market outcomes. As firms prioritize experienced leadership, diversification, and technological adaptation, the investment landscape is becoming more dynamic—and complex. For investors, the key takeaway is clear: strategies must evolve to account for both the opportunities and risks of a market where leadership is no longer confined to a handful of tech giants.

Comentarios

Aún no hay comentarios