Stratus Properties (STRS): A High-Growth Real Estate Play in a Premium Valuation

In the high-cost development environment of 2025, Stratus PropertiesSTRS-- (STRS) stands at a crossroads. The company's valuation metrics, growth initiatives, and financial health paint a complex picture: a firm with a compelling land portfolio and strategic asset monetization efforts, yet burdened by unprofitability and elevated debt costs. This analysis evaluates whether STRS's current valuation reflects its growth potential or overstates its prospects in a sector grappling with inflationary pressures.

Valuation Realism: A Tale of Contradictions

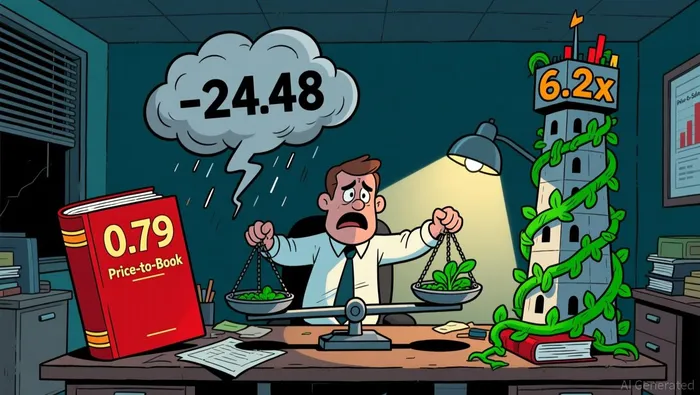

Stratus Properties trades at a Price-to-Book (P/B) ratio of 0.79, significantly below the US Real Estate industry average of 2.85. This suggests the market is discounting the company's balance sheet, likely due to its unprofitability. Indeed, STRS's Price-to-Earnings (P/E) ratio is -24.48, reflecting a loss per share of -$1.02 in Q4 2025 according to financial data. However, the company's Price-to-Sales (P/S) ratio of 6.2x is more than double the industry average of 3.2x, indicating a premium valuation for revenue. This divergence highlights a valuation paradox: investors are paying up for STRS's top-line growth while discounting its profitability.

The Enterprise Value/EBITDA (EV/EBITDA) ratio of -47.6x further underscores the company's unprofitability. While this metric is meaningless in a negative EBITDA context, it contrasts sharply with the industry's 21.27x average according to industry analysis. For STRSSTRS--, the premium P/S ratio may reflect optimism about its land development pipeline, but the negative EV/EBITDA signals skepticism about its ability to translate revenue into sustainable cash flows.

Growth Initiatives: Monetizing Assets in a High-Cost World

Stratus has adopted a dual strategy to navigate the high-cost environment: monetizing stabilized assets and optimizing debt. In 2025, the company sold the H-E-B-anchored Kingwood Place mixed-use development for $60.8 million, generating $26 million in pre-tax proceeds. Additional retail property sales, including Lantana Place and West Killeen Market, added $34.7 million in liquidity. These transactions not only improved cash flow but also funded a $25 million share repurchase program, signaling confidence in the stock's undervaluation.

To address rising interest costs, STRS refinanced or extended key loans at reduced rates, including those for The Saint June and Jones Crossing projects. This maneuver lowered near-term debt servicing burdens, though the company's total debt remains at $219.12 million according to financial data, with an interest coverage ratio of -16.47 according to financial metrics. While the real estate industry's average interest coverage ratio improved to 7.11 in Q2 2025 according to market analysis, STRS's negative ratio highlights its vulnerability to further rate hikes.

The company's 1,500-acre land portfolio, including projects like Holden Hills and The Saint Julia, offers long-term upside. However, elevated construction and labor costs-coupled with inflationary pressures-threaten to erode margins unless STRS can pass these costs to tenants or buyers.

Financial Health: A Delicate Balance

Stratus's debt-to-equity ratio of 0.66 appears moderate, but its negative earnings and interest coverage ratio paint a fragile financial profile. The company's recent shift from a P/E ratio of 86.5 in December 2024 to -24.48 in Q4 2025 according to financial data reflects deteriorating profitability, likely driven by development delays and rising input costs. While the real estate sector's average interest coverage ratio of 7.11 according to industry benchmarks suggests peers are better positioned to service debt, STRS's reliance on asset sales for liquidity raises questions about its long-term capital structure.

Conclusion: A High-Risk, High-Reward Proposition

Stratus Properties embodies the duality of a high-growth real estate play: a compelling land portfolio and strategic asset monetization efforts, juxtaposed with a premium valuation and precarious financial health. The company's P/B discount hints at undervaluation, but its P/S premium and negative EV/EBITDA suggest the market is pricing in aggressive revenue growth rather than profitability.

For investors, the key question is whether STRS can execute its development pipeline profitably in a high-cost environment. The recent share repurchase program and debt refinancing efforts are positive steps, but they must be paired with operational improvements to justify the current valuation. Until STRS demonstrates consistent profitability and stronger interest coverage, its premium P/S ratio may remain a speculative bet rather than a realistic assessment of intrinsic value.

Comentarios

Aún no hay comentarios