Strathcona's Montney Divestiture: A Blueprint for Energy Sector Resilience in 2025

The energy sector’s evolution toward capital discipline has never been clearer. Strathcona Resources’ $2.84 billion sale of its Montney assets to Tourmaline Oil Corp. marks a defining moment in this shift, signaling a strategic reorientation toward portfolio optimization as the primary driver of shareholder value. This transaction is not merely a reallocation of assets—it is a masterclass in how energy firms can thrive in volatile markets by prioritizing efficiency, reducing risk, and focusing capital on high-margin opportunities. For investors, this deal underscores a critical thesis: companies that execute disciplined asset swaps will outperform peers in commodity-sensitive environments.

The Deal: A Win-Win in Strategic Alignment

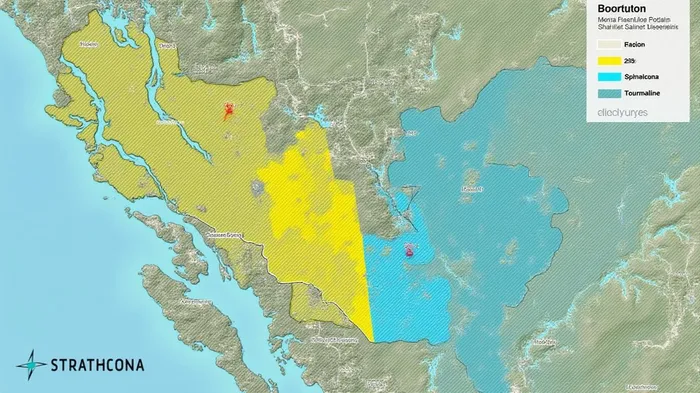

Strathcona’s sale of a 51% operated working interest in the Montney play to Tourmaline—alongside 1,247 net sections of land and 2,500 drilling locations—exemplifies the power of strategic divestiture. By offloading non-core assets, Strathcona has redirected capital toward debt reduction and high-potential exploration, while Tourmaline secures a low-cost, accretive position in one of North America’s most prolific unconventional basins.

The transaction’s structure is equally telling. Tourmaline, a Montney specialist, gains operational control and scale, while Strathcona reduces its debt burden and sharpens its focus on core areas. This synergy aligns with the sector’s broader trend: energy firms are increasingly treating assets as fungible tools, not sacred holdings.

Why This Matters: Capital Discipline as a Competitive Advantage

Strathcona’s move exemplifies the new energy economy’s mantra: focus, focus, focus. In an era of ESG pressures, fluctuating oil prices, and investor demands for returns, companies can no longer afford sprawling portfolios. The data confirms this shift:

-

-

By exiting non-core positions, Strathcona has freed itself to allocate capital to projects with superior returns. Meanwhile, Tourmaline’s acquisition of a mature, scalable asset positions it to capitalize on the Montney’s remaining resource potential. This is a win-win that exemplifies strategic portfolio optimization at scale.

The Investment Thesis: Prioritize Firms with Clear Optimization Strategies

The actionable takeaway for investors is unequivocal: prioritize energy companies that actively prune non-core assets and reinvest in high-margin opportunities. Strathcona’s deal creates a template:

1. Debt Reduction: A lighter debt load improves financial flexibility and resilience during downturns.

2. Operational Focus: Concentrating on core plays amplifies execution efficiency and reduces dilution from marginal projects.

3. Buyer Synergy: Acquirers like Tourmaline benefit from accretive, low-cost assets that boost production and margins.

Conclusion: The New Energy Landscape Demands Disciplined Players

Strathcona’s Montney sale is more than a transaction—it is a strategic pivot toward a future where capital discipline and portfolio focus are non-negotiable. In a sector rife with volatility, firms that systematically optimize their assets will dominate. Investors who back these companies now will be positioned to capture outsized returns as the energy market rewards resilience over ambition.

The writing is on the wall: the era of the undisciplined energy conglomerate is over. The winners in 2025 and beyond will be those who, like Strathcona, recognize that less can be more—and act decisively.

Act now to capitalize on this emerging trend.

Comentarios

Aún no hay comentarios