Strategy's Bitcoin Treasury Model 2.0: Balancing Dividend Stability with Long-Term Bitcoin Conviction

In November 2025, StrategyMSTR-- Inc. (MSTR) unveiled its BitcoinBTC-- Treasury Model 2.0, a strategic pivot aimed at fortifying its balance sheet while maintaining its aggressive Bitcoin accumulation trajectory. At the core of this evolution is a $1.44 billion U.S. dollar reserve, funded through at-the-market equity offerings, designed to cover 21 months of preferred stock dividends and interest on outstanding debt. This move, while lauded for its short-term liquidity benefits, raises critical questions about the long-term sustainability of Strategy's Bitcoin-centric business model in a volatile market environment.

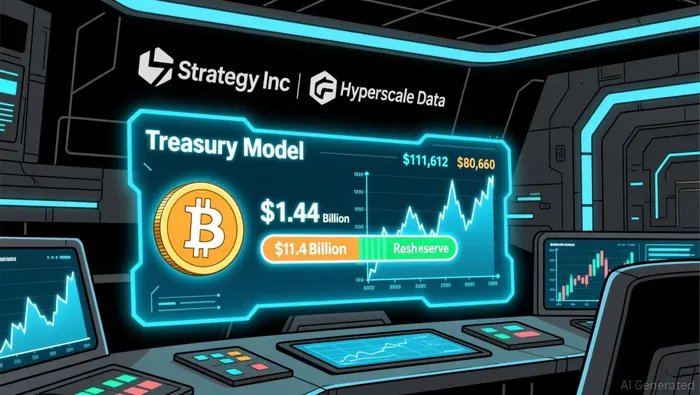

The Rationale Behind the $1.44B Reserve

Strategy's decision to establish a cash buffer reflects a calculated response to Bitcoin's recent price volatility. From $111,612 to $80,660, Bitcoin plummeted by November 21, 2025, eroding the company's projected earnings and net asset value (NAV). By insulating itself from forced Bitcoin sales, Strategy aims to preserve its 3.1% stake in the total Bitcoin supply-a position it views as foundational to its ambition to become a leading digital credit issuer according to the company's filings. The reserve also aligns with broader trends in the Digital Asset Treasury (DAT) sector, where firms like Hyperscale Data allocate 83% of their market capitalization to Bitcoin, underscoring the sector's reliance on crypto as a core asset.

However, the reserve's sustainability hinges on Strategy's ability to maintain its capital structure. The company's revised 2025 guidance, which assumes Bitcoin prices will range between $85,000 and $110,000, signals a tempered outlook. This contrasts with its earlier bullish assumptions and highlights the fragility of its leverage-driven model. While the reserve currently covers 21 months of obligations, the goal to extend this to 24 months implies ongoing reliance on ATM equity sales-a strategy that dilutes existing shareholders and amplifies earnings volatility.

Comparing Strategy to Peer DATs: Leverage vs. Diversification

Strategy's approach diverges from more conservative DATs, which prioritize capital preservation and diversified revenue streams. For instance, companies like BTCS and Galaxy Digital have adopted hybrid models that integrate staking, validator nodes, and DeFi yield generation to offset Bitcoin price swings. These strategies provide non-dilutive income, reducing the need for aggressive equity issuance. In contrast, Strategy's reliance on ATM programs and convertible bonds creates a perpetually dilutive structure, where equity holders face structural risks even as the company's Bitcoin holdings grow according to market analysis.

The Bitcoin Debt Coverage ratio-5.9x at $74,000-offers creditors a buffer against price declines according to analysis, but this metric does little to protect equity investors. As noted in a 2025 Skynet DAT report, DATs with robust custody arrangements and diversified revenue streams are better positioned to weather market downturns. Strategy's shift to institutional-grade custodians is a step in this direction, but its lack of active yield generation remains a vulnerability compared to peers according to industry reports.

Market Downturns and the NAV Premium Conundrum

The 2023–2025 Bitcoin bear market exposed critical weaknesses in DAT models. During this period, DAT stocks crashed 50–90% from 2025 peaks, compressing NAV premiums and forcing some firms to consider Bitcoin sales to meet obligations. Strategy's CEO acknowledged this risk, hinting at potential Bitcoin liquidations if financial pressures persist. While the company claims 71 years of dividend coverage at current Bitcoin prices according to financial analysis, this assumes a flat price trajectory-a scenario increasingly at odds with the asset's inherent volatility.

The DAT sector's survival during downturns depends on disciplined capital allocation and operational transparency. For example, firms leveraging Lightning Network-based payment rails to generate fee revenue have demonstrated resilience. Strategy's own foray into Bitcoin payments is a positive sign, but its scale remains modest compared to its total Bitcoin holdings. Without a diversified revenue base, the company's ability to sustain its NAV premium during prolonged downturns remains untested.

Conclusion: A Model in Transition

Strategy's Bitcoin Treasury Model 2.0 represents a pragmatic evolution, addressing immediate liquidity concerns while reinforcing its long-term Bitcoin conviction. The $1.44B reserve reduces the risk of forced sales and aligns with industry trends toward conservative treasury management according to market data. However, the model's reliance on ATM equity issuance and lack of active yield generation expose it to structural vulnerabilities. As the DAT sector matures, investors must weigh Strategy's aggressive Bitcoin accumulation against the risks of dilution and earnings volatility. For now, the company's ability to balance these competing priorities will determine whether its model is a sustainable innovation or a cautionary tale in the crypto-adjacent equity market.

Comentarios

Aún no hay comentarios