Strategic Shifts in Emerging Market Banking: HSBC's Sri Lankan Retail Exit and the Rise of Local Competitors

In a strategic move reshaping Sri Lanka's banking landscape, HSBCHSBC-- has agreed to divest its retail banking operations to Nations Trust Bank (NTB) for Rs. 18 billion, a transaction expected to conclude by mid-2026[5]. This exit, part of HSBC's global strategy to streamline operations and focus on high-growth markets, underscores a broader trend of foreign banks recalibrating their presence in emerging economies. For investors, the deal raises critical questions about the implications of such exits for local financial systems, competitive dynamics, and long-term profitability.

Strategic Drivers Behind HSBC's Exit

HSBC's decision to exit Sri Lanka's retail banking sector aligns with its broader strategic pivot. Over the past three years, the bank has exited markets in the U.S., Canada, and Bahrain, redirecting capital toward private credit and high-growth regions like Asia and the Middle East[4]. According to a report by Banking Gateway, HSBC's CEO Georges Elhedery emphasized the need to build a “more competitive, scalable, financing-led model” in investment banking, leveraging expertise in Asia[4]. This shift reflects a global industry trend: foreign banks increasingly retreating from low-margin markets in favor of regions with stronger growth potential.

The Sri Lankan exit is framed as a rationalization of resources. HSBC's corporate and institutional banking operations remain intact, but its retail business—serving 200,000 customers with accounts, credit cards, and loans—will transition to NTB[1]. This move allows HSBC to reduce operational complexity while retaining access to Sri Lanka's corporate sector, a critical differentiator in an era of cost-cutting.

NTB's Competitive Positioning and Financial Strength

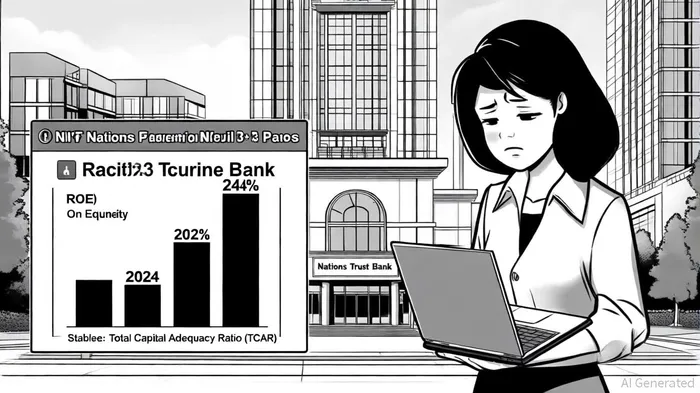

NTB, a long-standing player in Sri Lanka's banking sector, is well-positioned to absorb HSBC's retail operations. The bank reported a 46% year-over-year increase in Profit After Tax (PAT) to Rs. 17 billion in 2024, alongside a 24% Return on Equity (ROE)—a testament to its capital efficiency[2]. Its Total Capital Adequacy Ratio (TCAR) of 22.6% and Tier I Capital of 21.47% far exceed regulatory requirements, providing a buffer for absorbing HSBC's customer base and associated risks[2].

NTB's commitment to retaining all HSBC retail staff and ensuring a seamless customer transition further strengthens its appeal[5]. By acquiring a diversified portfolio of accounts and premium banking clients, NTB gains immediate scale, potentially accelerating its market share growth. For investors, this acquisition represents a strategic inflection point: NTB's robust balance sheet and operational discipline position it to capitalize on HSBC's exit without overleveraging.

Broader Trends in Foreign Bank Exits

HSBC's move is emblematic of a larger pattern. Empirical studies indicate that foreign bank entries in emerging markets initially stimulate financial development by enhancing efficiency and competition[3]. However, as economies mature, the marginal benefits of foreign presence diminish, and local banks increasingly dominate. Sri Lanka's case aligns with this trajectory: NTB's strong financial metrics suggest it can fill the void left by HSBC without relying on foreign capital inflows.

Yet, the implications are not unilaterally positive. Foreign banks often act as liquidity buffers during crises, drawing on global networks to stabilize local systems[3]. Their exits could, in theory, amplify vulnerability to external shocks. However, Sri Lanka's regulatory environment—marked by strict capital adequacy requirements—mitigates this risk. NTB's pledge to maintain regulatory ratios[1] further reinforces confidence in the sector's resilience.

Investment Implications and Future Outlook

For investors, HSBC's exit highlights two key opportunities. First, local banks like NTB are likely to benefit from increased market share and cross-selling potential. With HSBC's 200,000 retail customers now under its umbrella, NTB could see a material boost in fee income and loan growth. Second, the transaction underscores the growing importance of regional players in emerging markets. As foreign banks retreat, local institutions with strong governance and capitalization—like NTB—are poised to dominate, offering attractive long-term value.

However, risks persist. The integration of HSBC's operations will test NTB's management bandwidth, and regulatory delays could disrupt timelines[1]. Additionally, while Sri Lanka's banking sector is resilient, macroeconomic headwinds—such as inflation or currency volatility—remain potential drag factors.

In conclusion, HSBC's divestment from Sri Lanka's retail banking sector is a microcosm of a global shift. As foreign banks prioritize high-growth markets, local institutions with robust fundamentals are emerging as key beneficiaries. For investors, the challenge lies in identifying those with the capacity to scale and innovate—a category in which NTB appears well-positioned.

Comentarios

Aún no hay comentarios