Strategic Realignment and Market Resilience: The Toro Company's Path Forward in Golf, Grounds, and Irrigation

The Toro Company's recent leadership transitions and strategic realignment have positioned it as a formidable player in the golf, grounds, and irrigation sectors, even amid macroeconomic headwinds. As the company navigates shifting consumer demand and operational challenges, its focus on innovation, productivity, and sustainability is reshaping its competitive edge.

Leadership Shifts and Strategic Priorities

In a pivotal move, Grant M. Young was appointed group vice president of Golf, Grounds, and Irrigation, signaling The Toro Company's commitment to consolidating leadership in its high-growth professional markets, as reported in a Yahoo Finance article. This restructuring aligns with CEO Richard M. Olson's emphasis on "innovation, productivity, and resilience" to drive long-term profitability, according to the company's Q3 results. Young's role underscores the company's intent to accelerate R&D in next-generation technologies, including electric and autonomous equipment, which are critical to capturing market share in increasingly sustainability-conscious industries, per a SWOT analysis.

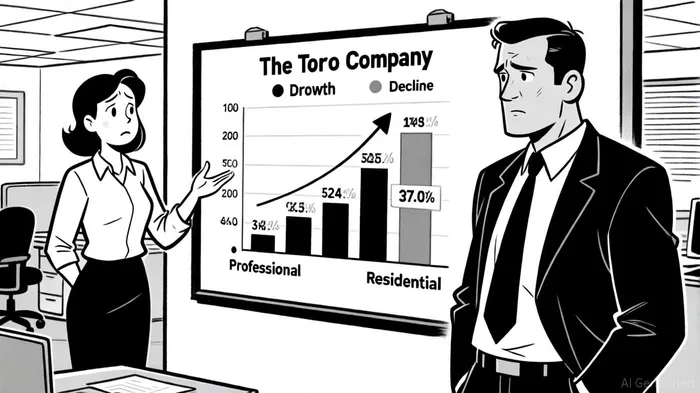

The third-quarter fiscal 2025 results highlight the effectiveness of this strategy. The Professional segment, which includes golf and grounds, delivered 6% growth in adjusted earnings and 250 basis points of margin expansion, outperforming the Residential segment's struggles with weak homeowner demand (according to the company's Q3 results). This divergence reflects a deliberate shift toward professional markets, where demand for underground construction and commercial-grade equipment remains robust.

Operational Efficiency and Cost Discipline

The AMP productivity program, a cornerstone of The Toro Company's strategic realignment, is on track to deliver $100 million in annualized savings by 2027, per the company's Q3 results. These cost reductions, coupled with divestitures of non-core assets, have offset softer residential sales and enabled the company to exceed adjusted earnings expectations despite a 2% overall sales decline in Q3 2025. Historically, companies that beat earnings expectations may experience mixed short-term reactions, but a buy-and-hold strategy could capture positive returns over a longer horizon. For instance, a backtest of Tetra Technologies (TTI) from 2022 to now shows that while the first-week median return was -3%, cumulative returns turned positive after 20 days (≈ +4–6%). By streamlining operations and reallocating capital, The Toro Company is fortifying its balance sheet and enhancing flexibility to invest in high-impact initiatives.

Innovation and Sustainability as Competitive Leverage

Sustainability is no longer a peripheral concern for The Toro Company-it is a strategic differentiator. The company's 2024 Sustainability Impact Report highlights advancements in electric equipment and smart irrigation systems, which reduce carbon footprints while improving operational efficiency for customers. For instance, its smart irrigation solutions leverage real-time data analytics to optimize water usage, a feature increasingly demanded by municipalities and golf courses under pressure to meet environmental regulations.

Moreover, The Toro Company's push into professional-grade electric and autonomous products aligns with broader industry trends toward decarbonization and labor cost reduction (see the earlier SWOT analysis). These innovations not only future-proof the company against regulatory risks but also position it to capitalize on the $12 billion global market for electric commercial equipment, projected to grow at a 15% CAGR through 2030.

Market Positioning and Investment Implications

While the Residential segment faces near-term headwinds, the Professional segment's performance demonstrates The Toro Company's ability to adapt to market dynamics. Its focus on high-margin, technology-driven solutions in golf, grounds, and irrigation creates a durable moat. Investors should also note the company's disciplined capital allocation, with $100 million in annualized savings from AMP and a 2025 dividend increase of 7.7% (as disclosed in the company's Q3 results).

However, risks persist. A prolonged slowdown in residential construction or supply chain disruptions could pressure margins. Yet, the company's strategic realignment-centered on leadership clarity, operational efficiency, and innovation-mitigates these risks and positions it for sustained outperformance.

Conclusion

The Toro Company's strategic realignment under Richard M. Olson and Grant M. Young reflects a clear-eyed focus on long-term value creation. By doubling down on professional markets, accelerating sustainability-driven innovation, and optimizing costs, the company is not only navigating current challenges but also laying the groundwork for leadership in the next decade. For investors seeking resilient industrial plays, The Toro Company's disciplined approach and sector-specific strengths make it a compelling case study in adaptive strategy.

Comentarios

Aún no hay comentarios