Strategic Opportunities in Home Equity Financing Amid Federal Rate Cuts

The Federal Reserve's cautious approach to interest rates in 2025 has created a pivotal moment for homeowners and investors to capitalize on falling borrowing costs. With the federal funds rate holding at 4.25%–4.50% and projections for two rate cuts this year, strategic financing moves—such as refinancing mortgages or securing Home Equity Lines of Credit (HELOCs)—could unlock significant savings while mitigating risks. This article explores how to navigate this environment effectively.

The Current Rate Landscape

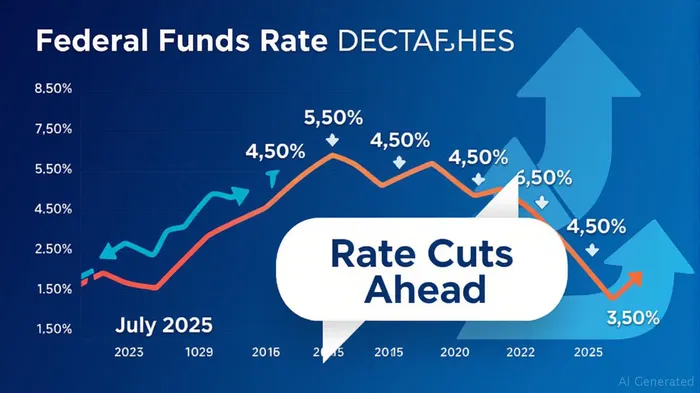

The Fed's June 2025 decision to maintain rates at 4.25%–4.50% reflects uncertainty around trade policies and inflation. However, two rate cuts are expected by year-end, potentially lowering the funds rate to 2.25%–2.50% by 2027. For homeowners, this means borrowing costs are nearing a multiyear trough, offering a window to lock in favorable terms.

Mortgage Rates: The average 30-year fixed rate has dipped to 6.59%–6.675%, down from peaks over 7% earlier in 2025. While still elevated compared to pandemic lows (2.65% in 2021), these rates are now competitive for long-term financing.

HELOC Rates: Variable HELOC rates average 8.90% post-introductory periods, tied to the prime rate (7.50% as of July 2025). Introductory rates as low as 6.49% (for 6 months) provide temporary relief, but borrowers must prepare for rate hikes after the promotional period.

Refinancing: A Low-Risk Opportunity

Why Refinance Now?

- Lock in Historic-Low Rates: While mortgage rates remain above 2021 lows, the Fed's path to cuts makes this the best time in years to secure fixed rates.

- Debt Consolidation: Use equity to replace high-interest debt (e.g., credit cards at 18%) with cheaper HELOC or mortgage financing.

- Cash-Out Refinance: Access equity for home improvements or investments while maintaining a low-cost, tax-deductible loan.

Action Steps:

1. Shop for Rates: Compare lenders aggressively. For example, Bank of AmericaBAC-- offers 6.59% on 30-year mortgages, while VA loans drop to 6.29%.

2. Time Your Move: Act before the Fed's September meeting, where the first cut is anticipated. Delaying could mean missing the window for lower rates.

3. Avoid Jumbo Loans: Opt for conforming loans (≤$970,800) to avoid higher rates (6.89% for jumbos).

HELOCs: Flexibility with Caution

HELOCs offer liquidity for variable needs (e.g., education, medical expenses) but require careful management.

Pros:

- Introductory Rates: 6.49% for 6 months (Bank of America) vs. 12.36% for unsecured loans.

- Tax Deductions: Interest is deductible if funds are used for home improvements.

Risks:

- Rate Volatility: Post-intro rates rise by 2–3%, and the prime could climb if the Fed delays cuts.

- Equity Exposure: HELOCs are secured against your home; default risks foreclosure.

Mitigation Strategies:

- Lock in a Fixed Rate: Convert part of the HELOC to a fixed-rate loan during the introductory period.

- Budget for Rate Increases: Assume the full variable rate (8.90%) when calculating affordability.

- Use for Short-Term Needs: Repay the principal during the low-rate window to avoid long-term exposure.

Risk Management in a Volatile Environment

While falling rates present opportunities, geopolitical risks (e.g., tariffs, political leadership shifts) could disrupt the Fed's timeline.

Key Risks to Monitor:

- Inflation Persistence: If core PCE remains above 2.5%, rate cuts may stall.

- Political Interference: Trump's potential Fed chair replacements (Warsh/Hassett) could destabilize policy consistency.

Diversification Tips:

- Blend Fixed and Variable: Use a mortgage for stability and a HELOC for flexibility.

- Build a Cash Cushion: Rate hikes post-2025 could strain budgets; maintain 6–12 months of expenses.

Investment Outlook

For investors, home equity financing can be a tool to boost returns:

- Equity Appreciation: Low rates may spur housing demand, increasing home values.

- Leverage for Growth: Use HELOC cash to invest in assets (e.g., dividend stocks, real estate) with higher yields than borrowing costs.

Conclusion

The confluence of falling rates and political uncertainty creates a nuanced landscape. Homeowners should prioritize refinancing mortgages now to lock in fixed rates, while cautiously leveraging HELOCs for short-term needs. Diversification and contingency planning will be critical to navigate potential rate volatility ahead. As the Fed's cuts unfold, those who act decisively stand to gain long-term financial resilience.

Investment Advice: Act by September 2025 to capitalize on projected rate cuts. Compare lenders for the lowest mortgage/HELOC terms, and ensure 20% equity buffer to avoid over-leverage.

Comentarios

Aún no hay comentarios