Strategic Minerals Plc: Intrinsic Value Analysis Amid Global Mineral Demand Surge

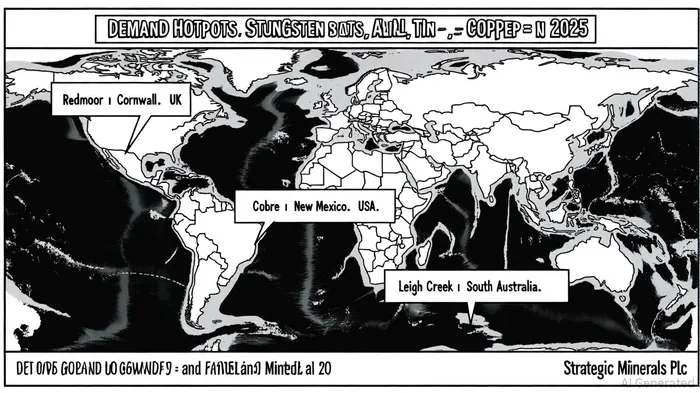

The valuation potential of Strategic Minerals Plc (LON:SML) hinges on its ability to capitalize on a confluence of global mineral demand trends and its strategic positioning in critical resource markets. As geopolitical tensions and industrial modernization drive surges in tungsten, tin, and copper demand, the company's portfolio of high-grade projects-Redmoor, Cobre, and Leigh Creek-positions it to benefit from tightening supply chains and rising prices. However, its intrinsic value must be assessed through a lens that balances operational risks, capital allocation, and macroeconomic tailwinds.

Financial Foundations and Operational Resilience

Strategic Minerals' H1 2025 unaudited results reveal a mixed but cautiously optimistic picture. Revenue fell to US$2.001 million, down 6.3% year-on-year, due to a 10-day wildfire-induced shutdown at its Cobre magnetite operation in New Mexico[2]. Yet, the company expects to offset this loss in H2 2025, with Q3 sales already showing recovery. Pre-tax profit declined to US$568,000, reflecting one-off costs from board restructuring and U.S. tax settlements, as well as increased exploration spending at Redmoor[2]. Despite these headwinds, unrestricted cash reserves rose to US$1.532 million by June 30, 2025, up 147% from December 2024, signaling improved liquidity[2].

The Cobre operation remains Strategic Minerals' cash cow, with a target of 48,000 tonnes of annual production and post-tax revenue of ~US$1.25 million[4]. While Q2 2025 sales dipped to US$818,000 due to the wildfire disruption, Q1 sales hit US$1.18 million-a 41% year-on-year increase[4]. This resilience underscores the asset's importance in funding higher-risk, higher-reward projects like Redmoor.

Redmoor: A Strategic Bet on Tungsten's Golden Age

The Redmoor Tungsten-Tin-Copper Project in Cornwall is Strategic Minerals' most promising asset. With inferred resources of 11.7 million tonnes grading 0.56% tungsten trioxide (WO₃), 0.16% tin, and 0.50% copper[2], it is touted as Europe's highest-grade undeveloped tungsten deposit. The project has secured £764,000 in UK government grants and £1.0 million in equity financing, fully funding a 5,300-meter diamond core drilling program expected to yield a JORC-compliant resource estimate by Q1 2026[3].

Tungsten's 2025 price surge-APT at $430/ton-degree, up 30.3% since January[1]-reflects structural supply constraints. China, which controls 82% of primary tungsten supply, has tightened export restrictions while boosting production of finished goods[5]. This creates a window for Western producers like Strategic Minerals to fill gaps, particularly as Europe's "Celestial Law Program" accelerates military modernization, driving demand for tungsten in armor-piercing munitions and cutting tools[5].

However, Redmoor's intrinsic value depends on its ability to transition from exploration to pre-feasibility. Current inferred resources lack a definitive production capacity, and the project's capital intensity-US$378,000 invested in H1 2025[2]-requires disciplined execution to avoid dilution.

Global Demand Dynamics and Strategic Positioning

The broader market backdrop is favorable. Tungsten demand is projected to grow at 8.7% CAGR through 2033[2], driven by both traditional (cutting tools) and emerging (robotics, defense) sectors. Tin, used in 50% of solder production for electronics, faces a looming structural deficit[1], while copper demand is set to rise 40% by 2040, outpacing supply constrained by 25-year mine development lead times[4].

Strategic Minerals' diversified portfolio-tungsten, tin, and copper-positions it to benefit from these trends. The Leigh Creek Copper Mine, though currently non-operational, holds a 5.4 million-tonne JORC resource at 0.7% copper[1], with a six-month call option that could unlock A$5.9 million in proceeds[2]. This liquidity could accelerate Redmoor's development or fund acquisitions in a fragmented market.

Valuation: Near Fair Value or Undervalued?

A two-stage DCF model estimates Strategic Minerals' intrinsic value at UK£0.012 per share, slightly above its current price of UK£0.011[2]. This assumes a 10-year free cash flow forecast and a terminal growth rate aligned with global mineral demand trends. While the stock trades near fair value, upside potential exists if Redmoor's resource upgrades to measured or indicated status, or if Cobre's production stabilizes post-wildfire.

Risks include geopolitical shifts (e.g., China easing export controls), exploration underperformance at Redmoor, and capital market volatility. However, the company's focus on critical minerals-designated as "strategically advantageous" in the UK's 2024 Criticality Assessment[3]-suggests policy tailwinds could offset some operational risks.

Conclusion

Strategic Minerals Plc is a speculative play on the global critical minerals boom, with its intrinsic value tied to the successful execution of Redmoor's exploration and the resilience of Cobre's cash flow. While current valuations reflect a discount to fair value, the company's alignment with supply-constrained, high-demand commodities offers compelling long-term potential-provided it navigates near-term operational and capital challenges. Investors with a 3–5 year horizon may find SML attractive as a satellite holding in a diversified resource portfolio.

Comentarios

Aún no hay comentarios