Strategic Entry Point for Junior Copper-Gold Producers in a Rising Commodity Cycle: The La Verde Opportunity

The junior mining sector is on the cusp of a golden era, and Hot Chili Limited's La Verde Cu-Au Porphyry project in Chile's Atacama region is a prime example of why investors should be paying attention. With diamond drilling now underway at this high-potential site, the project is poised to capitalize on a commodity supercycle driven by surging demand for copper and gold. Let's break down why this is a strategic entry point for junior producers—and why it could pay off handsomely for investors.

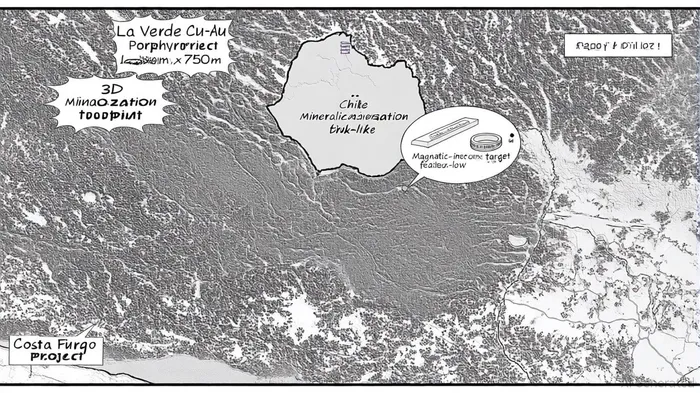

A Porphyry Powerhouse in a Prime Jurisdiction

Hot Chili's La Verde project has already delivered a game-changing discovery. Phase-one reverse circulation (RC) drilling confirmed a massive copper-gold footprint spanning 1,000 meters by 750 meters and extending 400 meters vertically, with notable intercepts like 389 meters grading 0.4% Cu and 0.1 g/t Au[1]. Over half of the initial drill holes ended in significant mineralization at the limit of RC depth, leaving the porphyry system open at depth and laterally[2]. Now, phase-two diamond drilling is targeting deeper expansion, with one rig operating on a double-shift basis to accelerate results[3].

What makes this even more compelling? The Atacama region is a global copper powerhouse, and Chile remains one of the most stable jurisdictions for mining. Regulatory applications for further drill access are nearing final approval, which will unlock lateral extensions and nearby targets[4]. Crucially, geophysical and geochemical data have identified three “look-alike” porphyry targets adjacent to La Verde, suggesting the potential for a district-scale cluster[5]. This is not just a single deposit—it's a system with the potential to redefine the region's resource base.

Commodity Tailwinds: Copper in a Supply-Deficient World

Copper is the new oil, and the market is screaming for more. According to a report by Bloomberg, global copper demand is projected to outpace supply by 300,000–500,000 metric tonnes in 2025, creating a structural deficit that will drive prices higher[6]. The green energy transition is the primary catalyst, with copper consumption in renewable energy and electric vehicles expected to surge. J.P. Morgan forecasts a further price decline to $9,100/tonne in Q3 2025 but anticipates stabilization at $9,350/tonne by year-end as inventory imbalances unwind[7]. Meanwhile, BMI Research has revised its 2025 average price target to $10,000/tonne, factoring in geopolitical risks and the U.S. Federal Reserve's monetary policy[8].

Junior producers like Hot Chili are uniquely positioned to benefit. With a 50% tariff on semi-finished copper products in the U.S. and a 129% YoY surge in refined copper imports through May 2025, the global supply chain is in flux[9]. La Verde's shallow oxide and sulfide mineralization could be rapidly converted into open-pit material, extending the mine life of Hot Chili's Costa Fuego project and improving financial metrics. This is exactly the kind of project that thrives in a tightening market—low-cost, high-grade, and scalable.

Gold's Role in the Commodity Cycle

While copper is the star, gold remains a critical tailwind. Although 2025 forecasts suggest a moderation in gold prices compared to 2024, the metal is still at an inflection point. Central bank purchases have slowed, but retail demand—exemplified by $56.5 billion in ETF inflows in 2024—shows no signs of abating. For projects like La Verde, which host both copper and gold, this dual-metal exposure provides a buffer against volatility and enhances project economics.

Why This Is a Strategic Entry Point

Junior mining stocks are historically cyclical, and we're entering a new up-cycle. Improved investor sentiment, increased exploration funding, and a focus on domestic supply chains in North America are creating fertile ground for juniors. La Verde's recent A$14M rights issue to fund its resource estimate and strategic partnering process signals management's confidence—and gives investors a clear path to value realization.

The key here is timing. With phase-two drilling already underway and a maiden resource estimate on the horizon, Hot Chili is at a critical inflection point. The company's ability to expand the porphyry footprint and unlock nearby targets could attract strategic partners or off-take agreements, accelerating development. For investors, this represents a low-cost entry into a project with district-scale potential in a jurisdiction that matters.

Risks and Considerations

No investment is without risk. Copper prices could underperform if Chinese demand weakens further or if global inventories normalize faster than expected. Additionally, junior producers often face liquidity challenges, and Hot Chili's rights issue may dilute existing shareholders. However, the current macroeconomic environment—marked by a green energy transition and geopolitical tensions—strongly favors metals like copper and gold.

Conclusion: A High-Conviction Play

In a rising commodity cycle, projects like La Verde don't come along often. With a robust mineralization footprint, a stable jurisdiction, and a favorable macroeconomic backdrop, Hot Chili is positioned to deliver outsized returns for early investors. As the world races to electrify its future, copper—and the juniors that produce it—will be at the center of the action.

Comentarios

Aún no hay comentarios