The Strategic Case for Extending Duration in Bonds Before the 4% Yield Threshold Vanishes

The U.S. 10-year Treasury yield has lingered near the 4% thresholdT-- for much of 2025, a level that has historically marked inflection points in bond markets and macroeconomic trajectories. With the yield currently at 4.05% as of September 15, 2025, and 4.12% as of October 2, 2025, investors face a critical decision: Should they lock in current yields before the threshold disappears, or wait for further Fed action and inflation trends? The answer lies in understanding macroeconomic momentum and yield curve positioning-a framework that has historically justified duration extension as a strategic tool.

Current Macroeconomic Momentum and Yield Curve Positioning

The U.S. economy remains in a delicate balancing act. While GDP growth has slowed due to higher borrowing costs and geopolitical tensions-particularly tariff escalations on Chinese imports, which could add 0.4–0.6% to core inflation by Q3 2025-the Federal Reserve has maintained a "modestly restrictive" policy stance to counter inflationary risks, according to a Financial Times analysis. This has delayed rate cut expectations, keeping the 10-year yield stable despite a subdued housing market and mixed labor data.

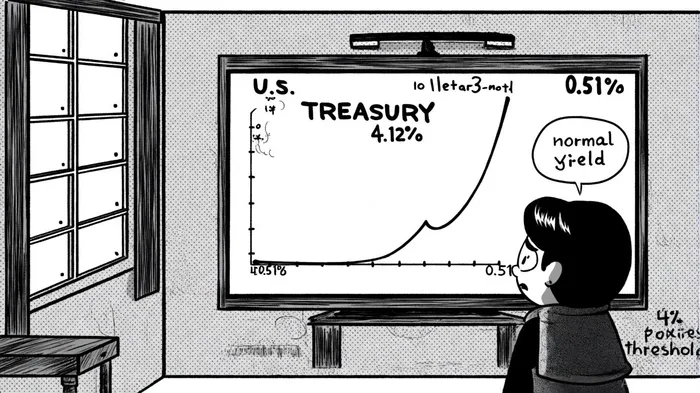

The yield curve, as of October 2, 2025, remains normal, with a 10-year-3-month spread of 0.51%, as noted in a CEPR column. This suggests moderate expectations of future economic growth but also hints at vulnerability. A steeply inverted curve has historically preceded recessions, typically within two to two-and-a-half years, according to a CME Group analysis. However, the current curve's normalcy reflects confidence in the broader economic framework, even as inflation expectations remain elevated.

Historical Precedents for Duration Extension

Historical data underscores the potential rewards of extending duration near 4% yield thresholds. In the 1990s, investors who extended fixed-income duration during upward-sloping yield curves were rewarded, according to an AQR study. Similarly, during the 2020s, bond strategies near 4% were shaped by inflation and growth trends. For instance, the 2022 inflation peak (6.6%) forced the Fed to tighten aggressively, penalizing long-duration bonds. Yet, as inflation moderated to 3.9% by 2025, the Fed's cautious approach has created a window for duration extension, as noted by the CME Group analysis.

A key insight from history is the role of yield curve momentum. Short-term Treasury returns exhibit autocorrelation: months with positive returns are followed by higher excess returns, while negative months produce near-zero returns, a pattern explored in the CME Group analysis. This momentum effect, though less pronounced in long-term bonds, suggests that trend-following strategies-such as overweighting long-term Treasuries after months of positive returns-can be profitable.

The Case for Strategic Duration Extension Today

Extending duration now offers several advantages. First, the Fed's delayed rate cuts mean yields are unlikely to rise sharply in the near term, reducing the risk of price declines in long-term bonds. Second, the yield curve's normal shape indicates no immediate recession risk, which would typically trigger aggressive rate cuts and benefit shorter-term bonds. Third, historical patterns show that duration extension can act as "insurance" if the Fed begins cutting rates, as it did during past downturns (e.g., 500 bps cuts in 2008 and 2020), a point emphasized in the CME Group analysis.

However, risks persist. If inflation surprises to the upside or geopolitical tensions escalate, short-term rates could rise, inverting the curve and penalizing long-duration bonds. Investors must also consider reinvestment risk: locking in current yields forgoes opportunities to reinvest at higher rates if the Fed eventually tightens further, a dynamic discussed in the CEPR column.

Conclusion

The 4% yield threshold is not a static benchmark but a dynamic signal of macroeconomic forces. Given the Fed's cautious stance, moderate inflation, and a normal yield curve, extending duration now offers a strategic edge. While risks remain, historical precedents and yield curve momentum suggest that investors who act decisively before the threshold vanishes may reap significant rewards. As always, diversification and careful monitoring of macroeconomic indicators will be essential to navigating this complex landscape.

Comentarios

Aún no hay comentarios