Strategic Buying Opportunities in U.S. Equities Amid Geopolitical Volatility

The interplay between U.S. trade policies and global capital flows has created a complex landscape for investors in 2025. As reciprocal tariffs and geopolitical realignments reshape supply chains, international demand for U.S. equities has oscillated between panic selling and strategic accumulation. This volatility, however, has also uncovered asymmetric opportunities for investors willing to navigate the turbulence.

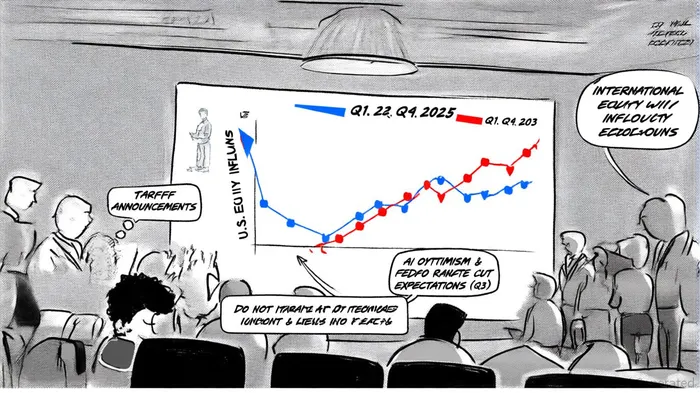

A Tale of Two Phases: Panic and Optimism

The year began with a dramatic sell-off in U.S. equities as global fund managers reacted to the imposition of steep reciprocal tariffs. By Q1 2025, inflows to U.S. stocks had plummeted, with energy, technology, and basic materials sectors bearing the brunt of the selloff [1]. However, this pessimism reversed sharply in Q3 as optimism around AI-driven productivity gains and expectations of Federal Reserve rate cuts reignited demand. By late 2025, U.S. equities were attracting record inflows, outperforming European and Japanese markets, particularly in small-cap stocks [2]. This rebound, while heartening, has raised concerns among analysts who draw parallels to the 2000 dotcom bubble, warning of potential overvaluation in AI-centric sectors [1].

The Rise of International Equities as a Diversifier

Amid U.S. policy uncertainty, international equities have gained traction as a strategic diversifier. European markets, for instance, have outperformed U.S. counterparts by a significant margin in 2025, supported by undervalued valuations and fiscal stimulus packages aimed at bolstering defense and infrastructure [3]. The weakening U.S. dollar has further amplified their appeal, making foreign assets more accessible to U.S. investors while enhancing returns for those holding dollar-denominated positions [4]. Advanced economies have also seen a 70% reduction in foreign direct investment (FDI) flows to China, redirecting capital toward Europe and other regions [5].

Sectoral Vulnerabilities and Defensive Opportunities

Sectoral preferences among international investors have diverged sharply in 2025. Energy and technology stocks, heavily exposed to global trade, saw cumulative losses of 7–9% in the immediate aftermath of tariff announcements [6]. Conversely, defensive sectors like healthcare and utilities experienced smaller declines, reflecting their resilience to macroeconomic shocks [6]. Financials, particularly in high-exposure countries, underperformed due to fears of credit risk and macroeconomic spillovers [6]. These trends suggest that investors should prioritize sectors with less trade dependency and robust cash flows, such as healthcare and utilities, while remaining cautious about overexposed industries.

Strategic Buying Opportunities in a Polarized Market

The current environment presents a unique opportunity to capitalize on mispricings in both U.S. and international markets. For U.S. equities, the post-tariff selloff has undervalued small-cap stocks and defensive sectors, which are now trading at attractive valuations relative to their long-term growth potential [2]. Meanwhile, international equities—particularly in Europe—offer compelling entry points for investors seeking to hedge against U.S. policy risks. The MSCI EAFE Index, representing 21 developed markets, trades at a notable discount to U.S. benchmarks, suggesting potential for re-rating as global supply chains stabilize [7].

However, investors must balance these opportunities with macroeconomic risks. A U.S. dollar rebound or a Fed policy reversal could temporarily dampen international equity gains. Similarly, a correction in AI-driven sectors could trigger broader market jitters. Diversification across geographies and sectors remains critical, with a focus on companies positioned to benefit from long-term trends such as industrial automation and semiconductor innovation [5].

Conclusion

The 2025 trade tensions have created a bifurcated market landscape, where U.S. equities oscillate between panic and euphoria while international assets gain traction as diversifiers. For strategic investors, the key lies in leveraging sectoral mispricings and geographic diversification to mitigate geopolitical risks. While U.S. small-cap and defensive sectors offer near-term value, international equities—particularly in Europe—present a compelling case for long-term growth. As always, vigilance against overvaluation and macroeconomic headwinds will be essential in navigating this volatile environment.

Comentarios

Aún no hay comentarios