Strategic Attraction of the 5-Year U.S. Treasury in an Inverted Yield Curve Environment

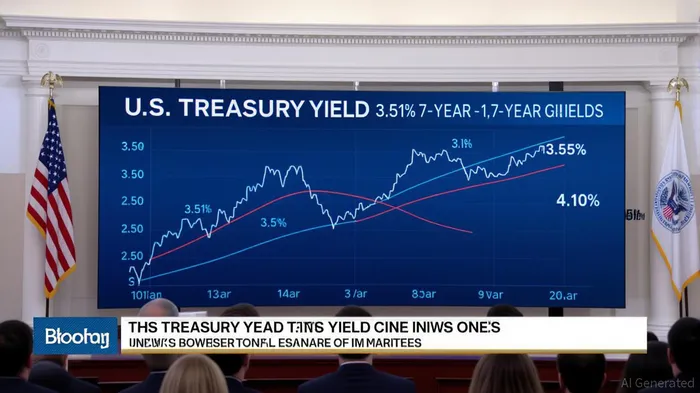

The U.S. Treasury yield curve has entered an inverted configuration, with long-term rates lagging behind short-term rates. As of September 5, 2025, the 10-year Treasury yield stood at 4.10%, while the 2-year yield hit 3.51%, reflecting a historically bearish signal for economic growth[1]. Amid this inversion, the 5-year Treasury yield—currently at 3.57%—emerges as a strategically attractive segment for investors, balancing yield potential, duration risk, and historical performance during similar market conditions[4].

The 5-Year Yield: A Sweet Spot in a Flattening Curve

The 5-year Treasury yield sits at the intersection of short- and long-term dynamics. While the 3-year yield languishes at 3.47%[2], the 5-year offers a 10-basis-point premium, outpacing shorter maturities. Simultaneously, it trails the 7-year yield of 3.80%[6], avoiding the heightened duration risk associated with longer-term bonds. This positioning makes the 5-year segment a natural hedge against both near-term volatility and the uncertainty of prolonged economic stagnation.

Historically, 5-year bonds have demonstrated resilience during inverted yield curve periods. For instance, during the 2006 inversion, 5-year Treasuries outperformed equities in 2007 and continued to deliver strong returns as the 2008 financial crisis unfolded[2]. Investors who held these bonds benefited from rising prices driven by increased demand for safe-haven assets amid economic uncertainty. Similarly, in 2000, the 5-year yield curve inversion preceded a recession by 13 months, providing a window for strategic reallocation into fixed income[3].

Economic Fundamentals Bolster Strategic Appeal

The Federal Reserve's cautious approach to monetary policy and the anticipation of two rate cuts by year-end further enhance the 5-year's attractiveness[2]. With slower U.S. growth and a weakening dollar boosting international fixed-income returns[2], the 5-year yield's current level of 3.57% offers a compelling carry trade. This yield implies an annualized return of approximately 3.57% over the next five years—a figure that, while lower than the 4.69% cited in some third-party analyses[2], remains competitive given the inverted curve's bearish implications.

Moreover, the 5-year segment benefits from the Treasury's updated monotone convex spline methodology for yield curve derivation, ensuring greater accuracy in pricing and risk assessment[1]. This technical refinement reduces the likelihood of mispricing, making the 5-year yield a more reliable benchmark for portfolio allocation.

Risk Mitigation in a Recession-Prone Environment

The inverted yield curve's predictive power cannot be ignored. The 10-2 yield curve spread turned negative in recent months, aligning with historical patterns preceding recessions[2]. As of August 2025, the probability of a recession within the next year stands at 25.7%[5], underscoring the need for defensive positioning. The 5-year Treasury's moderate duration—shorter than 10-year bonds but longer than 2-year notes—provides a buffer against both rate hikes and liquidity crunches, making it a versatile tool for risk management.

Conclusion: A Strategic Allocation for 2025

In an environment marked by inverted curves and looming recession risks, the 5-year U.S. Treasury yield offers a unique combination of yield, stability, and historical performance. Its position between the underperforming 3-year and the duration-sensitive 7-year/10-year segments makes it an optimal choice for investors seeking to balance income generation with capital preservation. As the Federal Reserve navigates a path of cautious easing, the 5-year segment stands out as a cornerstone for fixed-income portfolios in Q4 2025.

Comentarios

Aún no hay comentarios