Strategic Asset Reallocation in a Deteriorating Regional Services Outlook

The U.S. services sector, a cornerstone of economic activity, is navigating a complex landscape in late 2025. While national indices suggest resilience—such as the ISM Services index hitting a six-month high of 52.0 in August[1]—regional divergences and structural headwinds are reshaping investment dynamics. For investors, the interplay between localized slowdowns and sector-specific innovations demands a recalibration of asset allocation strategies.

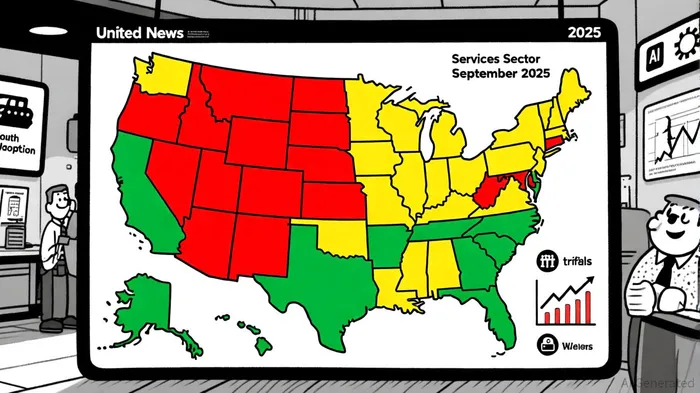

Regional Divergence and Structural Pressures

The latest data underscores a fragmented recovery. The S&P Global U.S. Services PMI dipped to 53.9 in September 2025[1], signaling a moderation in expansion, while the Philadelphia Fed's nonmanufacturing survey revealed a 19-point drop in general activity to 5.8[3]. These trends highlight a critical divide: the South remains a growth engine, driven by employment gains and AI-driven productivity in professional services[4], whereas the Northeast and West face challenges from tariffs and labor shortages[1].

Employment data further complicates the picture. The ISM Services employment index lingered at 46.5 in August[1], reflecting a third consecutive month of contraction, while part-time employment and average workweeks declined[3]. This labor market tension, coupled with elevated input costs (39% of firms reporting higher expenses[3]), suggests a sector grappling with inflationary pressures and skills gaps.

Implications for Equities: Sector Rotation and Resilience

Investors must prioritize sectors demonstrating adaptability to macroeconomic headwinds. The RSM US Business Services Outlook notes that marketing and advertising firms are leveraging AI to streamline operations[5], while staffing agencies are investing in automation and reskilling[5]. These innovations position such firms as defensive plays in a volatile environment.

Conversely, consumer-facing services—particularly those reliant on international trade—are vulnerable. The OECD Economic Outlook emphasizes the need for structural reforms to sustain growth[2], a warning for investors in hospitality or retail sectors exposed to tariff-driven demand shifts. Defensive equities in healthcare and utilities, which offer stable cash flows amid labor and cost pressures, may also gain traction[4].

Fixed Income: Hedging Against Regional Volatility

Fixed income strategies should account for regional asymmetries. Municipal bonds in the South, where employment growth outpaces national trends[4], could offer attractive yields. However, investors must remain cautious in regions with weaker fundamentals, such as the Northeast, where nonmanufacturing activity softened[3].

Corporate bond spreads are likely to widen in sectors facing cost inflation, such as logistics and professional services[1]. High-yield bonds from firms adopting AI and automation—like those highlighted in the U.S. International Trade Commission's 2025 report[1]—may provide a balance of risk and reward.

Strategic Reallocation Framework

A dual-pronged approach is recommended:

1. Equity Allocation: Overweight AI-driven services (e.g., tech-enabled staffing, digital marketing) and underweight trade-exposed consumer sectors.

2. Fixed Income: Diversify geographically, favoring Southern municipal bonds and high-yield corporate debt from innovation-focused firms.

Conclusion

The U.S. services sector's mixed performance in 2025 underscores the importance of granular analysis. While national indices mask regional fragilities, proactive investors can capitalize on sector-specific strengths and geographic opportunities. By reallocating assets toward innovation-driven equities and selectively hedging fixed income exposure, portfolios can navigate the sector's evolving challenges with resilience.

Comentarios

Aún no hay comentarios