Strategic Asset Allocation in the Post-Retirement Era: Leveraging Macro-Trends and Time-Based Positioning

In the post-retirement era, where longevity and market volatility redefine financial planning, strategic asset allocation must evolve beyond static frameworks. Veteran trader Peter Brandt's methodologies-rooted in classical charting, disciplined risk management, and macroeconomic regime detection-offer a blueprint for retirees to navigate uncertain markets while preserving capital and generating income. By integrating time-based positioning with macro-trend analysis, retirees can align their portfolios with dynamic economic cycles, optimizing liquidity, growth, and resilience.

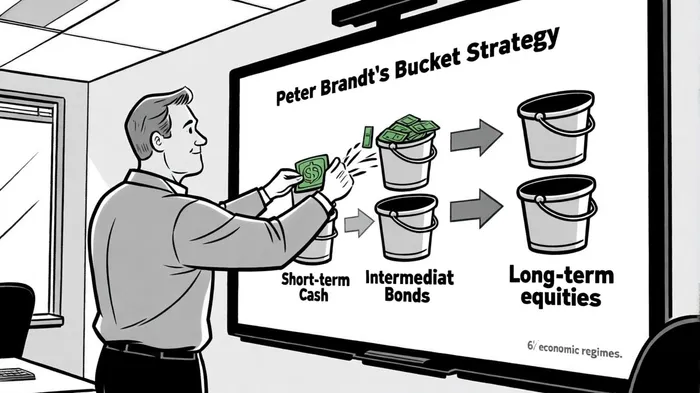

The Bucket Strategy: A Foundation for Post-Retirement Stability

Brandt's bucket strategy divides retirement portfolios into three time-based buckets to balance liquidity, income, and growth. The short-term bucket (1–3 years) prioritizes cash or cash equivalents, shielding retirees from market downturns and ensuring immediate expenses are met, according to a MarketClutch guide. The intermediate bucket (3–10 years) allocates to high-quality bonds or balanced funds, offering moderate growth and steady income, per the MarketClutch guide. Finally, the long-term bucket (10+ years) targets equities or REITs, leveraging their inflation-fighting potential and compounding power, as described in the MarketClutch guide.

This approach mitigates the risk of "dollar cost ravaging," where retirees are forced to sell assets at depressed prices during market declines, according to a BlackRock analysis. For example, a retiree with a pension might allocate more to equities in the long-term bucket, while those reliant on portfolio income might prioritize short-term cash and bonds, per the MarketClutch guide. However, the bucket strategy's rigidity-its lack of rebalancing and reliance on fixed time horizons-can lead to suboptimal outcomes in volatile markets, a limitation noted in the MarketClutch guide.

Macro-Trend Alignment: Dynamic Adjustments via Regime Detection

To address these limitations, retirees can integrate macroeconomic regime detection-a data-driven approach to identifying prevailing economic conditions (e.g., recovery, stagflation, reflation) using machine learning and fundamental indicators, as shown in an arXiv paper. That paper demonstrates that regime-based models can outperform traditional static allocations by adjusting portfolios to align with asymmetric opportunities. For instance:

- In stagflationary regimes, retirees might overweight Treasury inflation-protected securities (TIPS) and gold while reducing equity exposure, as the paper suggests.

- During reflationary booms, equities and commodities could dominate, capitalizing on rising growth and inflation, according to the same study.

This dynamic framework enhances the bucket strategy by allowing tactical shifts within and across buckets. For example, if a regime detection model identifies an impending reflationary phase, the intermediate bucket might increase its allocation to inflation-linked bonds or infrastructure ETFs, while the long-term bucket tilts toward cyclical equities, as described in the arXiv paper.

Time-Based Positioning: Brandt's Charting and Risk Management

Brandt's emphasis on classical charting-head and shoulders, triangles, and rectangles-provides retirees with actionable insights into market psychology and high-probability entry/exit points, a point Brandt elaborates in Brandt's Substack post. For the long-term bucket, identifying chart patterns in equities or REITs can help retirees time purchases during market weakness, a strategy echoed in BlackRock's positioning for retirement insights.

Equally critical is Brandt's risk management discipline: limiting risk to 1% of capital per trade and using aggressive stop-loss strategies, a discipline Brandt outlines in his Substack post. In retirement portfolios, this translates to capping losses in volatile assets (e.g., equities) within the long-term bucket. For example, a retiree might allocate 10% of the long-term bucket to small-cap stocks but use trailing stops to protect gains, ensuring that no single position jeopardizes the portfolio's stability, as Brandt recommends.

Psychological and Structural Considerations

Retirees must also address the emotional challenges of market volatility. Brandt's philosophy of focusing on process over outcomes-limiting screen time and adhering to predefined rules-can prevent impulsive decisions during downturns, a theme Brandt emphasizes in his Substack post. This aligns with the bucket strategy's emphasis on structured disbursement, where retirees draw from the short-term bucket first, avoiding the temptation to liquidate long-term assets during market stress, per the MarketClutch guide.

Structurally, integrating macroeconomic signals like the yield curve and output gap can refine tactical decisions, an approach Brandt references in his writing. For instance, an inverted yield curve-a historical recession indicator-might prompt retirees to increase cash reserves in the short-term bucket while reducing equity exposure, consistent with Brandt's risk-first perspective.

Conclusion: A Resilient Framework for the Post-Retirement Era

By combining Brandt's bucket strategy with macroeconomic regime detection and classical charting, retirees can build portfolios that adapt to shifting economic landscapes. This approach balances immediate liquidity needs with long-term growth, while disciplined risk management and emotional control safeguard against market extremes. As the global population ages and macroeconomic volatility persists, such a framework offers a path to sustainable retirement income and capital preservation.

Comentarios

Aún no hay comentarios