Strategic Asset Allocation and Compounding Efficiency: Building Retirement Security Through Early Wealth Accumulation

In the evolving landscape of retirement planning, strategic asset allocation (SAA) and compounding efficiency have emerged as twin pillars for securing long-term financial stability. As market dynamics shift—marked by eroding traditional diversification benefits, persistent inflation, and behavioral challenges—investors must adopt nuanced strategies to maximize growth while mitigating risk. For those prioritizing early wealth accumulation, the interplay between disciplined asset allocation and the power of compounding offers a roadmap to retirement security.

The Evolution of Strategic Asset Allocation

Traditional static allocation models, which fix equity/bond ratios regardless of market conditions, are increasingly inadequate in today's volatile environment. A 2025 study on behaviorally adaptive optimization strategies demonstrates that dynamic SAA—leveraging tools like Monte Carlo simulations and multi-objective optimization—outperforms static approaches by preserving wealth during downturns and adapting to shifting macroeconomic signals[1]. This approach aligns with Vanguard's 2024 findings, which reaffirm the critical role of SAA in target-date funds (TDFs), where asset mix remains the primary determinant of long-term returns and risk profiles[2].

However, the structural challenges of recent years—such as positive stock-bond correlations and fiscal imbalances—have forced a reevaluation of diversification. BlackRock's 2025 analysis highlights the need to incorporate uncorrelated assets like liquid alternatives, commodities, and international equities to enhance risk-adjusted returns[3]. Morgan StanleyMS-- similarly advocates broadening portfolios beyond U.S. equities and bonds, emphasizing non-U.S. equities and credit products to address valuation extremes and diversify risk[4].

Compounding Efficiency: The Early Advantage

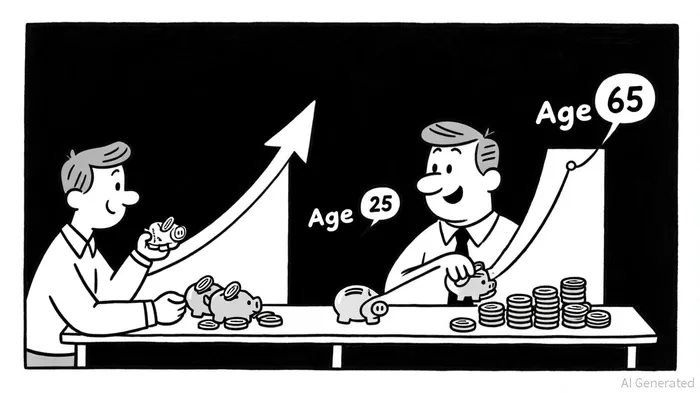

The power of compounding is magnified when harnessed early. Consider a hypothetical investor contributing $5,000 annually starting at age 25 versus 35. At a 7% annual return, the former accumulates $1.1 million by age 65, while the latter reaches only $566,000[5]. This underscores the exponential impact of time on wealth growth. For early retirees, who face extended horizons and inflation risks, strategic allocation becomes even more critical.

Quantitative studies reveal that a 60/40 stock-bond allocation historically delivered a 9.85% annualized return over 50 years, with a median ending balance of $1.224 million in distribution mode[6]. However, the convergence of correlations and underperformance of international assets since 2000 has challenged diversified portfolios. To adapt, investors must integrate low-volatility strategies and multi-factor frameworks. A 2025 paper on macro factor investing shows that aligning SAA with economic cycles—using data spanning a century—can enhance resilience across market environments[7].

Bridging SAA and Compounding: Practical Strategies

- Dynamic Withdrawal Flexibility: Research by the Financial Planning Association highlights that adjusting withdrawals based on portfolio performance reduces the risk of depletion during retirement[8]. For early retirees, this flexibility—paired with a bucket strategy (segmenting assets into short-, medium-, and long-term buckets)—can balance liquidity needs with growth objectives[9].

- Tax-Efficient Reinvestment: Placing stocks in taxable accounts (to leverage favorable capital gains treatment) and bonds in tax-deferred accounts optimizes compounding[10]. Case studies like Mike and Jessica's $3 million portfolio illustrate how Roth conversions and withdrawal sequencing further amplify after-tax wealth[11].

- Leveraging Low-Volatility Assets: The 2024 paper Leveraging the Low-Volatility Effect argues that incorporating low-volatility equities—potentially with leverage—can enhance risk-adjusted returns without sacrificing growth[12].

Conclusion

For investors prioritizing early retirement, strategic asset allocation is not merely about balancing risk and return—it is about architecting a framework that capitalizes on compounding's exponential potential. As markets evolve, the fusion of dynamic SAA, behavioral adaptability, and tax-efficient strategies will define long-term success. The data is clear: starting early, diversifying intelligently, and rebalancing relentlessly are not just best practices—they are imperatives in an era of uncertainty.

Comentarios

Aún no hay comentarios