U.S. Stocks Edge Higher at the Open as Investors Weigh Fed Stagflation Risks and AI Optimism

What history tells us about bull markets after the 3-year mark 👇

U.S. equities opened modestly higher Wednesday morning as investors balanced cautious signals from the Federal Reserve about inflation and labor-market risks against continued optimism around artificial intelligence spending and select pockets of risk appetite.

At the opening bell, the Dow Jones Industrial Average was at 48,177.7, up 63.47 points, or 0.13%. The Nasdaq Composite rose 17.46 points, or 0.08%, to 23,128.9, while the S&P 500 added 2.22 points, or 0.03%, to 6,802.5. The Russell 2000 advanced 0.42 points, or 0.17%, to 250.32. All index levels and moves reflect opening-bell readings from the provided dashboards.

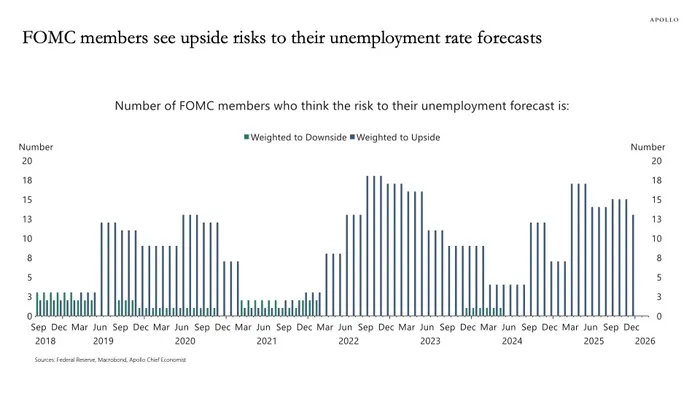

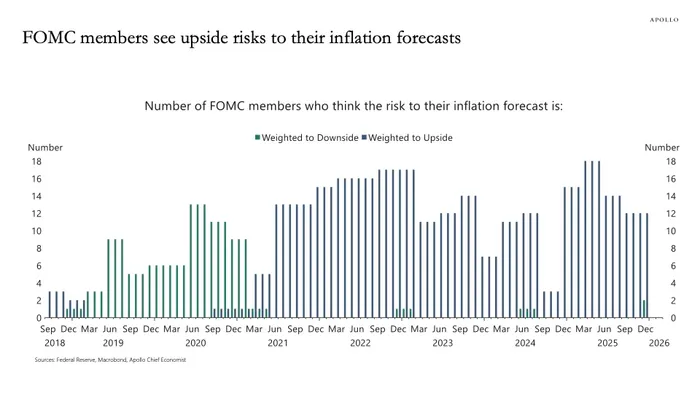

Markets opened amid heightened macro uncertainty following new analysis of Federal Open Market Committee forecasts. According to charts compiled by Torsten Slok, chief economist at Apollo Global Management, a growing number of Fed policymakers see upside risks to both inflation and unemployment, an unusual combination that points to rising concern about stagflation risks in 2026. The data show that, in recent projections, more FOMC members view inflation risks as skewed to the upside while simultaneously seeing higher risks that unemployment could rise, reinforcing the Fed’s challenge as it balances price stability against labor-market softness .

Those concerns were reflected across asset classes early Wednesday. Market volatility eased, with the CBOE Volatility Index falling to 16.03, down 0.45 points, or 2.73%, signaling reduced near-term demand for equity protection despite the macro backdrop. In digital assets, BitcoinBTC-- traded at $87,809.92, up $934.84, or 1.08%, continuing to attract inflows as investors look for alternative stores of value amid policy uncertainty.

In commodities trading, U.S. crude futures rose 1.45% to $55.93, while February gold futures gained 0.71% to $4,362.90, reflecting a mix of geopolitical hedging and sensitivity to real-rate expectations at the open. Prices are based solely on the provided market screenshots.

Equity investors are also digesting longer-term structural themes, particularly in technology. In recent research note Wedbush Securities argued that the artificial intelligence investment cycle remains in its early stages and is “a 1996 moment, not a 1999 tech bubble moment.” The firm said AI infrastructure spending built throughout 2025 is expected to translate into “transformational monetization opportunities into 2026 and beyond,” with Big Tech capital expenditures projected in the $550 billion to $600 billion range next year. Wedbush analysts added that less than 5% of U.S. enterprises have fully embarked on AI-driven strategic deployments, suggesting substantial runway remains .

Outside of technology, pressure is building in more rate-sensitive corners of the market. The U.S. homebuilding sector remains under strain as affordability challenges persist. Recent results from Lennar highlighted how builders are maintaining volume through aggressive incentives at the cost of sharply lower margins, reinforcing investor concerns that earnings pressure could extend into 2026 .

For now, early trading suggests markets are attempting to look through near-term macro risks, leaning on easing volatility and long-term growth narratives to support equity prices. Whether that balance holds will likely depend on how incoming economic data and Fed communications clarify the trajectory for inflation, employment, and interest rates into the new year.

Comentarios

Aún no hay comentarios