Sterling Infrastructure's Valuation Dislocation and the Path to Long-Term Growth

Sterling Infrastructure (STRL) has underperformed relative to broader market indices in 2025, despite the global infrastructure sector's resilience amid macroeconomic volatility. This dislocation raises questions about valuation misalignment and the company's long-term growth prospects. By analyzing STRL's financial metrics against sector and market benchmarks, and contextualizing the UK infrastructure industry's challenges and opportunities, we can assess whether this underperformance reflects overvaluation or a temporary mispricing.

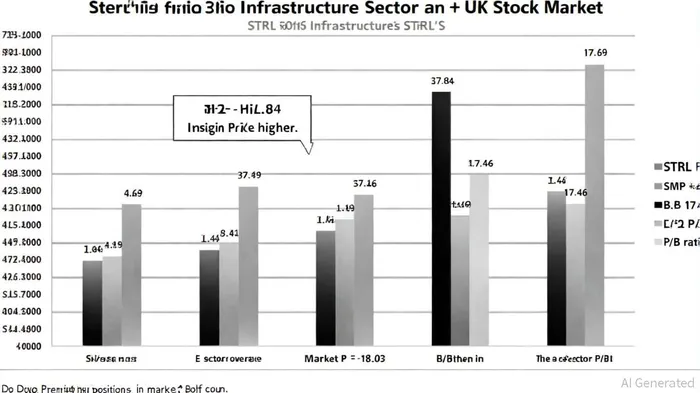

Valuation Dislocation: A Premium Too Far?

Sterling Infrastructure's trailing price-to-earnings (P/E) ratio of 37.84 and forward P/E of 35.08, according to StockAnalysis statistics, place it well above the S&P 500 Infrastructure sector's average P/E of 17.46, according to WorldP/E sector data, which itself is classified as "overvalued" relative to its 5-year average of 12.40. Its price-to-book (P/B) ratio of 12.03, per StockAnalysis, further underscores this premium, far exceeding typical valuations for capital-intensive infrastructure firms, which often trade at lower P/B ratios due to their stable cash flows and tangible assets.

In contrast, the broader UK stock market, as represented by the FTSE 250, has a P/E ratio of 18.69, according to WorldP/E UK data, significantly higher than its 5-year average of 14.95. While this suggests a generally expensive market, STRL's metrics remain outliers even within this context. The lack of specific data for the FTSE 250 infrastructure sector, as shown by the FTSE Infrastructure Index, complicates direct comparisons, but STRL's valuation appears to diverge sharply from the sector's historical norms.

Sector Challenges: A Fragile Foundation

The UK infrastructure sector itself is navigating a fragile landscape. Construction output grew modestly by 0.2% in July 2025, according to the Gleeds Q3 2025 report, but new orders contracted sharply in Q2, particularly in infrastructure and industrial projects. Regulatory delays, labor shortages, and rising insolvency rates-construction accounted for 16.3% of UK insolvencies in Q2 2025, per the Gleeds report-add to cost pressures. Freelance and trade wages in construction have risen 3–5% annually, squeezing margins for firms like STRLSTRL--.

These challenges are compounded by weak consumer confidence and macroeconomic uncertainty. While private infrastructure fundraising in H1 2025 reached $134 billion, according to the CBRE Infrastructure Quarterly, driven by renewables and digital infrastructure, public-sector projects remain constrained by fiscal caution. The UK government's push for public-private partnerships offers some optimism, but execution risks persist.

Long-Term Growth: A Sector on the Cusp

Despite near-term headwinds, the infrastructure sector's long-term fundamentals remain compelling. Private infrastructure deal activity in H1 2025 hit $520 billion, with renewables and digital infrastructure growing by 48% and 33%, respectively, according to CBRE's analysis. Investors increasingly view infrastructure as a hedge against inflation, a trend that could benefit STRL if it aligns with these high-growth subsectors.

Moreover, global infrastructure indices, such as the FTSE Infrastructure Index, highlight the sector's resilience. While STRL's specific metrics lack direct comparables, its high valuation may reflect investor optimism about its exposure to future demand in energy transition and digital infrastructure.

Conclusion: Balancing Dislocation and Potential

Sterling Infrastructure's current valuation appears disconnected from both sector and market averages, raising concerns about overvaluation. However, the UK infrastructure sector's long-term growth drivers-particularly in renewables and digital infrastructure-suggest that STRL's premium could be justified if it successfully pivots to these areas. Investors must weigh the company's ability to navigate near-term challenges against its potential to capitalize on structural trends. For now, STRL's underperformance may reflect a correction in overextended valuations, but its future hinges on execution in a sector poised for transformation.

Comentarios

Aún no hay comentarios