Is Starbucks (SBUX) a Sell or a Strategic Buy Amid Earnings Pressure and Valuation Disparity?

The Contrarian Case for Starbucks: Navigating Earnings Headwinds and Valuation Gaps

Starbucks Corporation (SBUX) has long been a bellwether for consumer discretionary stocks, but its recent financial performance has sparked a heated debate among investors. With earnings momentum under pressure and valuation metrics diverging from industry norms, the question looms: Is StarbucksSBUX-- a sell amid its struggles, or a strategic buy for contrarian investors?

Earnings Momentum: A Tale of Two Metrics

Starbucks’ Q3 FY2025 results underscored a stark duality. While consolidated net revenues rose 4% year-over-year to $9.5 billion, driven by store expansion and currency effects [1], earnings per share (EPS) plummeted. GAAP EPS fell 47% to $0.49, and non-GAAP EPS dropped 46% to $0.50, primarily due to one-time investments in its “Back to Starbucks” strategy, including labor and leadership initiatives [1]. This divergence between top-line growth and bottom-line contraction reflects a broader trend: margin compression.

The company’s operating margin for FY2024 stood at 14.95%, down from 16.32% in 2023 [5], as inflationary pressures and rising labor costs—exacerbated by unionization efforts—eroded profitability. U.S. comparable store sales declined 2% in Q3, with a 4% drop in transactions partially offset by a 2% increase in average ticket [1]. These figures suggest a shift in consumer behavior, potentially influenced by macroeconomic factors like the rise of GLP-1 drugs, which may suppress demand for high-calorie offerings [3].

Valuation Disparity: Overpriced or Undervalued?

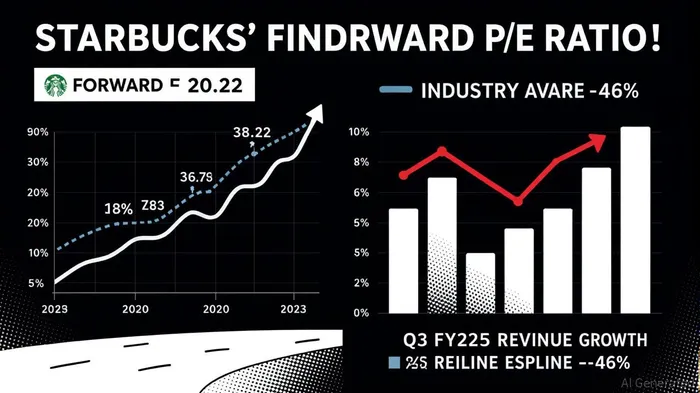

Starbucks’ valuation metrics tell a conflicting story. As of September 2025, the stock traded at a forward P/E ratio of 38.8, significantly above the industry average of 20.22 [2]. This premium suggests the market is pricing in future earnings growth, despite current headwinds. However, contrarian analysts argue that the stock is undervalued when viewed through a discounted cash flow (DCF) lens. Morningstar’s adjusted P/E ratio of 20.3x implies a 30% discount to the current forward P/E, hinting at potential upside if earnings stabilize [3].

The Price-to-Sales (P/S) ratio further complicates the narrative. Starbucks’ P/S ratio of 2.73 in August 2025 [4] trades below the industry average of 3.81 [6], indicating that the market values each dollar of sales more conservatively than its peers. This discrepancy could reflect skepticism about the company’s ability to convert revenue into sustainable profits, particularly in the U.S., where same-store sales have declined for three consecutive quarters [5].

Strategic Buy or Sell? A Contrarian Lens

For contrarian investors, Starbucks presents a paradox. On one hand, the stock’s elevated P/E ratio and declining earnings suggest overvaluation. On the other, the company’s strategic initiatives—such as menu simplification, a four-day return-to-office policy, and the 2026 innovation pipeline—could catalyze a turnaround. Brian Niccol, CEO, has emphasized that Green Apron Service and operational efficiency measures are already improving customer satisfaction and store performance [5].

Analyst forecasts, however, remain mixed. The consensus EPS for FY2025 has dropped to $2.20, down from $2.70 in prior estimates [3], while 2026 projections hover around $2.81 [3]. These downward revisions reflect concerns about labor costs, inflation, and competition. Yet, some bullish forecasts project a 9.53% stock price increase to $101.91 by 2026 [4], assuming successful execution of the “Back to Starbucks” strategy.

The Verdict: A High-Risk, High-Reward Proposition

Starbucks’ valuation disparity and earnings momentum create a compelling case for both sides. A strategic buy thesis hinges on the belief that the company’s investments in operational efficiency and innovation will reverse declining trends, particularly in the U.S. and China. Conversely, a sell argument emphasizes the risks of margin compression, unionization challenges, and macroeconomic headwinds.

For contrarian investors, the key lies in timing. If Starbucks can stabilize its earnings and demonstrate clear progress in Q4 FY2025, the current valuation gapGAP-- may close, unlocking upside potential. However, patience is required: The path to recovery is unlikely to be linear.

Source:

[1] Starbucks Reports Q3 Fiscal Year 2025 Results [https://investor.starbucks.com/news/financial-releases/news-details/2025/Starbucks-Reports-Q3-Fiscal-Year-2025-Results/default.aspx]

[2] Starbucks (SBUX) Stock Dips While Market Gains: Key Facts [https://finance.yahoo.com/news/starbucks-sbux-stock-dips-while-233308452.html]

[3] Starbucks Bottom-Line Expected to Remain Pressured Through 2026 – OppenheimerOPY-- [https://www.moomoo.com/news/post/55949249/starbucks-bottom-line-expected-to-remain-pressured-through-2026-oppenheimer]

[4] SBUXSBUX-- - Starbucks Corp Stock Price Forecast 2025, 2026, ... [https://stockscan.io/stocks/SBUX/forecast]

[5] Starbucks CorporationSBUX-- Financial Update & Strategic Analysis [https://www.monexa.ai/blog/starbucks-corporation-latest-financial-and-strateg-SBUX-2025-07-14]

[6] Starbucks P/S 2025 | US8552441094 | SBUX [https://eulerpool.com/en/stock/Starbucks-Stock-US8552441094/PE]

Comentarios

Aún no hay comentarios