Stablecoin Infrastructure and Institutional Adoption: Strategic Positioning in the Evolving Crypto Payments Landscape

The crypto payments landscape in 2025 is no longer a frontier market-it is a fully integrated component of global capital infrastructure. Institutional adoption of stablecoin ecosystems has reached a critical inflection point, driven by regulatory clarity, yield optimization, and the urgent need for frictionless liquidity. As asset managers, hedge funds, and corporate treasurers reallocate capital into digital ecosystems, the strategic positioning of stablecoins as both a settlement layer and a yield-generating asset class is reshaping traditional finance.

The Institutional Hierarchy: Compliance, Liquidity, and Innovation

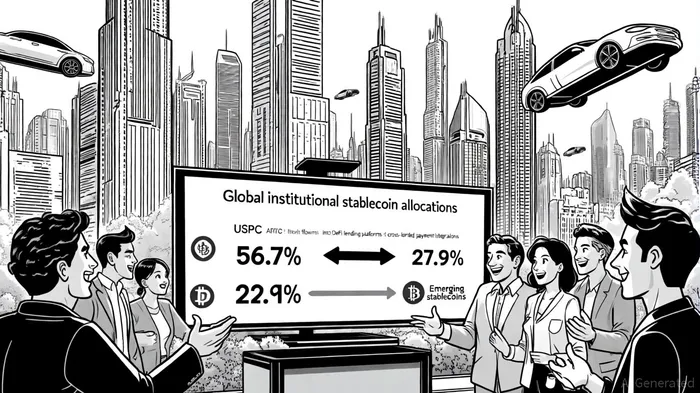

According to the Stablecoin Insider report, institutional allocations to stablecoin infrastructure have surged to $47.3 billion in Q3 2025, with USDCUSDC-- dominating the market at 56.7% share. This dominance is not accidental but a calculated response to regulatory alignment. Circle's USDC, with its transparent reserves and compliance with the GENIUS Act-a landmark piece of legislation designed to harmonize stablecoin oversight with traditional financial frameworks-has become the de facto bridge between TradFi and DeFi, the report argues.

Meanwhile, Tether's USDTUSDT-- retains 27.9% of the institutional market, a testament to its entrenched role in cross-chain liquidity and legacy crypto networks. However, the rise of compliant alternatives like PayPal's PYUSD-growing at 140% quarter-over-quarter-signals a shift toward institutional-grade stablecoins that balance innovation with regulatory guardrails, according to the Stablecoin Insider report.

Yield, Liquidity, and the Blurring of Financial Boundaries

Data from Alpha Stake Fund reveals that 68% of institutional stablecoin allocations are funneled into yield-generating strategies, spanning decentralized lending protocols, automated aggregators, and centralized finance (CeFi) platforms. AaveAAVE--, for instance, commands 22.4% of institutional DeFi lending, while Yearn Finance's algorithmic yield optimization appeals to passive institutional strategies, the Stablecoin Insider report notes. Centralized platforms like CoinbaseCOIN-- Prime and Binance Institutional have further lowered barriers to entry, offering tailored solutions that mirror the risk management frameworks of traditional asset classes, the report adds.

The strategic value of stablecoins extends beyond yield. Corporate treasurers are now tokenizing U.S. Treasuries as digital proxies, enabling real-time settlement and reducing counterparty risks, Alpha Stake Fund documents. In parallel, stablecoins are embedded into global payment rails. Visa and Stripe's integration of stablecoin-based cross-border solutions has cut settlement times from days to seconds, while emerging markets-famously constrained by inflation and capital controls-are adopting stablecoins as a de facto reserve currency, as Forbes reports.

Regulatory Tailwinds and the Path to Mainstream Adoption

The GENIUS Act's role in this transformation cannot be overstated. By establishing a clear framework for stablecoin issuers and custodians, the legislation has alleviated institutional concerns about regulatory arbitrage and operational risk, Forbes notes. This clarity has catalyzed a wave of hybrid financial products, where stablecoins serve as both a liquidity buffer and a gateway to decentralized markets. For example, hedge funds are now allocating portions of their portfolios to stablecoin-backed derivatives, while venture capital firms are leveraging stablecoin vaults to fund blockchain-native startups, Alpha Stake Fund observes.

Yet challenges persist. The rapid growth of institutional stablecoin infrastructure has outpaced some legacy systems, creating friction in interoperability and data transparency. As Forbes notes, institutions are increasingly demanding real-time auditing tools and granular risk analytics to navigate this complex ecosystem.

Strategic Implications for Investors

For investors, the institutionalization of stablecoin infrastructure represents a paradigm shift. Stablecoins are no longer speculative assets but foundational components of a reimagined financial stack. Strategic positioning here requires a dual focus:

1. Allocation to Compliant Ecosystems: Prioritize stablecoins and platforms aligned with evolving regulations, such as USDC and PYUSD.

2. Yield Infrastructure Exposure: Invest in protocols (Aave, Yearn) and CeFi players (Coinbase Prime) that facilitate institutional-grade capital efficiency.

Conclusion

The institutional adoption of stablecoin infrastructure is not a passing trend but a structural realignment of global finance. As stablecoins bridge the gap between traditional and digital ecosystems, their role in payments, yield, and liquidity will only deepen. For institutions and investors alike, the question is no longer if to participate-but how to position strategically in a landscape where speed, compliance, and innovation converge.

Comentarios

Aún no hay comentarios