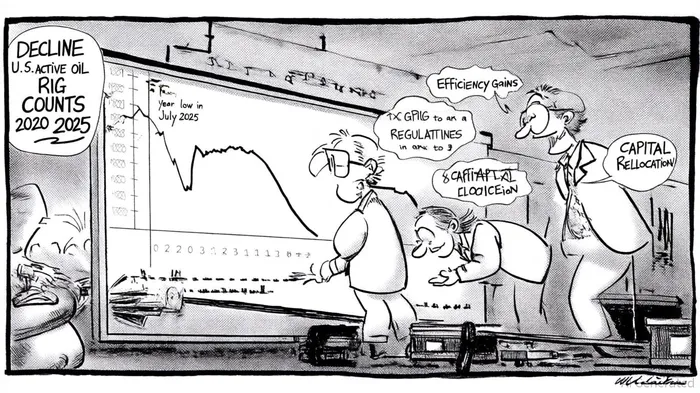

Stabilizing U.S. Rig Counts: A Signal of Sector Maturity or Resilience?

The U.S. energy sector is at a crossroads. Rig counts have stabilized near a 3-year low, with 539 active rigs as of July 2025, and oil-focused rigs at 425, according to the Baker Hughes count. This decline, coupled with a Dallas Fed survey that recorded a business activity index of -6.5 in Q3 2025, raises a critical question: Are these trends signaling a maturing sector or a resilient one adapting to new realities? The answer lies in dissecting capital allocation strategies and investment readiness across oil, gas, and renewables.

Rig Count Trends: Efficiency, Saturation, or Strategic Shifts?

The U.S. rig count has fallen by 10–20% year-to-date, with Oklahoma's rigs dropping to 43 in a single week, per the Baker HughesBKR-- count. While some attribute this to market saturation-operators scaling back after a post-pandemic rebound-others point to strategic recalibration. The Dallas Fed survey notes that 77% of energy executives expect shale oil to become viable internationally within a decade, suggesting a long-term focus on cost efficiency over aggressive expansion.

Meanwhile, the EIA projects a 3% decline in U.S. refinery capacity by year-end 2025, reported in an OGJ article, driven by tightening margins and U.S. tariffs on Canadian crude. Yet, production efficiency gains-falling input costs and AI-driven drilling-have offset some of these pressures, the OGJ article notes. This duality of contraction and optimization complicates the maturity vs. resilience debate.

Capital Allocation: Oil vs. Renewables

The sector's capital reallocation reveals a stark divide. Major oil companies-ExxonMobil, ChevronCVX--, BPBP--, ShellSHEL--, Equinor, and TotalEnergies-are projected to spend $108–112 billion in 2025, with 80% of that directed toward traditional oil and gas operations, the OGJ piece reports. BP and Shell, for instance, have cut renewable budgets by 50% and relaxed carbon reduction targets, and Equinor reduced its renewable investment plan from $10 billion to $5 billion, according to the same reporting.

In contrast, U.S. utilities are projected to invest over $790 billion from 2025 through 2027, according to an S&P Global analysis, with 36% of 2023 utility capex allocated to grid resilience and climate adaptation per Resilient by Design. Renewable energy investments alone are expected to exceed $30 billion annually in 2025 and 2026, that S&P Global analysis projects, driven by state mandates and the Inflation Reduction Act. This divergence highlights a sector bifurcation: majors retreating to core hydrocarbons while utilities embrace the energy transition.

Maturity or Resilience?

The stabilizing rig count reflects both maturity and resilience. Maturity is evident in the sector's shift toward consolidation and efficiency. M&A activity has reduced U.S. E&P companies from 50 to 40, with 42% of 2024 acquisitions targeting unproved properties to build future inventory, the OGJ reporting shows. This suggests a focus on optimizing existing assets rather than speculative growth.

Resilience, however, is underscored by strategic adaptability. The Permian Basin's dominance-accounting for 65% of tight oil growth since 2010-demonstrates a pivot to high-margin, high-productivity regions. Similarly, midstream investments in pipelines like Energy Transfer's $5.3 billion Desert Southwest expansion show infrastructure modernization to meet evolving demands, including LNG exports and data center energy needs, as noted in industry reporting.

Yet, the sector's resilience is tested by an $18 trillion capital gap for net-zero goals and a projected $500 billion shortfall in grid hardening by 2050, estimates from the Resilient by Design analysis indicate. While utilities are addressing these gaps through smart grid tech and battery storage, the retreat of oil majors from renewables risks stalling the energy transition.

Implications for Investors

For investors, the key is balancing short-term sectoral shifts with long-term decarbonization trends. Oil and gas majors offer stable returns amid disciplined capital allocation, but their reduced focus on renewables may limit upside potential. Conversely, utilities and renewables present growth opportunities, albeit with regulatory and technological risks.

The U.S. rig count's stabilization is not a binary signal of maturity or resilience-it is a reflection of a sector in flux. As energy companies navigate policy shifts, market volatility, and climate imperatives, the ability to adapt will determine which firms thrive.

Comentarios

Aún no hay comentarios