Southern Company's Stability Makes It a Wise Hold Right Now

Southern Company SO is a leading U.S. electric utility that provides regulated electricity and gas services across the Southeast. The company also operates power generation and transmission assets, focusing on stable, long-term infrastructure investments. SO’s regulated business model supports consistent earnings and dividends, making it a reliable player in the defensive utilities sector.

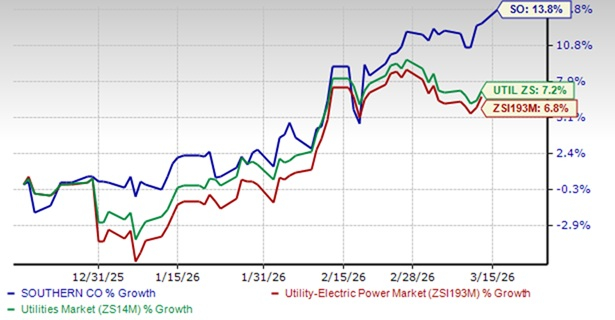

Over the past three months, Southern Company stock rose approximately 13.8%, significantly outperforming both the Zacks Utility-Electric Power sub-industry (ZSI193M), which gained 6.8%, and the Utilities Sector (ZS14M), which increased 7.2%. This strong performance highlights SO’s resilience and investor preference compared with its peers in the utility Sector.

3-Month Share Price Performance Comparison

Image Source: Zacks Investment Research

Investors, both current and prospective, face a key decision: is now the right time to add more SO’s shares, or should they continue holding their current investments? Let’s examine why the company has outperformed the sector and the sub-industry, highlight strengths and explore potential challenges it may encounter going forward.

Forces Behind SO’s Growth

Transformative Growth in Large Load Demand: SO has secured 10 gigawatts (“GW”) of signed contracts with large load customers, a 2 GW increase from the prior quarter. This demand, driven by data centers and industrial expansion, is not speculative. These projects are under construction and provide a highly visible, multi-year revenue stream that underpins the company's long-term financial outlook.

Superior Contractual Protections for Investors: The company employs a disciplined, bilateral contracting approach for large loads. Contracts feature minimum 15-year terms with "take-or-pay" style provisions designed to cover 100% of incremental costs, including generation investment and cost of capital. Substantial collateral requirements and termination payments provide an additional layer of security for investors.

Significant Increase in Long-Term Earnings Guidance: SO’s management has provided a multi-year earnings outlook, projecting adjusted EPS growth of 8% to 9% from 2026 through 2028. They established initial guidance for 2027 ($4.85-$4.95) and 2028 ($5.25-$5.45). This rare, multi-year visibility demonstrates high confidence in the durability of their growth strategy.

Massive and Expanding Capital Investment Plan: The company unveiled an $81 billion five-year base capital plan (2026-2030), a 30% increase from the prior year's forecast. With 95% allocated to state-regulated utilities, this investment directly supports a projected 9% rate base growth, creating a clear and regulated pathway to earning the returns embedded in their financial predictions.

Obstacles in the Market That May Affect SO’s Rise

Dependence on a Concentrated, Emerging Industry: A significant portion of the projected 10% annual sales growth is tied to a single customer segment, large loads, particularly data centers. A slowdown in the tech sector, a shift in data center building trends or a technological breakthrough that reduces their power needs could severely impact growth.

Interest Rate Sensitivity and High Financing Costs: Interest expense was a significant headwind in 2025 and is projected to remain elevated. With $34.1 billion in new debt planned through 2028, the company is highly sensitive to interest rate fluctuations. Higher-for-longer rates would increase financing costs, directly pressuring net income and earnings per share.

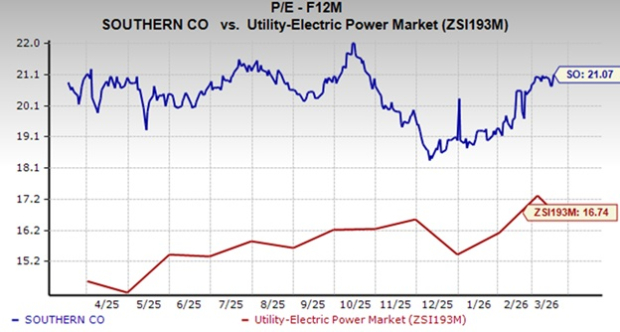

Valuation May Limit Upside: Southern Company stock likely already reflects its ambitious growth plan and raised guidance. With a price-to-earnings ratio of 21.07x — well above the 16.74x Zacks Utility-Electric Power sub-industry average — the stock appears elevated. This high valuation suggests the market may be overly optimistic, potentially limiting future returns if growth falls short of expectations. Investors should exercise caution, as the stock may be priced ahead of its fundamental earnings potential.

Image Source: Zacks Investment Research

Competition From Alternative Energy and Distributed Resources: The long-term demand for utility-scale power could be challenged by advances in technology. The proliferation of customer-sited generation (like rooftop solar and battery storage) and energy efficiency, mentioned as a risk factor, could eventually erode sales growth if it becomes more economical for large customers.

Final Verdict on SO Stock

SO shows strong long-term growth potential, driven by 10 GW of signed large-load contracts, disciplined 15-year agreements with take-or-pay provisions and a robust $81 billion five-year capital plan primarily in regulated utilities. Management projects 8-9% adjusted EPS growth from 2026 through 2028, indicating confidence in its durable earnings strategy.

However, the company faces risks from heavy reliance on large-load customers, high interest expenses with $34.1 billion in planned debt, elevated valuation relative to peers and potential competition from alternative energy and distributed generation. Given this mix of strengths and potential challenges, investors should wait for a more opportune entry point instead of adding this stock to their portfolios.

SO’s Zacks Rank and Key Picks

Currently, SO has a Zacks Rank #3 (Hold).

Investors interested in the utility sector might look at some better-ranked stocks like Atmos Energy ATO, Duke Energy DUK and FirstEnergy FE, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Atmos Energy is worth approximately $31.2 billion. The company is one of the largest natural gas-only distributors in the United States, serving over 3 million customers across more than 1,400 communities in eight states. Atmos Energy focuses on safely delivering reliable energy, investing in infrastructure and maintaining strong operational and financial performance.

Duke Energy is worth approximately $103.55 billion. The company is a major American electric power holding company that provides electricity and natural gas services to millions of customers across the United States. Duke Energy focuses on generating, transmitting and distributing energy while investing in renewable resources and modernizing its energy infrastructure.

FirstEnergy isworth approximately $29.57 billion. It is a diversified electric utility company that serves millions of customers in the Midwest and Mid-Atlantic regions of the United States. FirstEnergy focuses on generating and distributing electricity, maintaining reliable grid infrastructure, and investing in modernization and clean energy initiatives.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

See Our Newest 5 Stocks Set to Double Picks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Southern Company (The) (SO): Free Stock Analysis Report

FirstEnergy Corporation (FE): Free Stock Analysis Report

Duke Energy Corporation (DUK): Free Stock Analysis Report

Atmos Energy Corporation (ATO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Comentarios

Aún no hay comentarios