South Korea's Precarious Balancing Act: Trade Vulnerability and Fiscal Constraints Under U.S. Pressure

South Korea stands at a crossroads in 2025, its economy buffeted by U.S. geopolitical pressures, domestic fiscal constraints, and global trade headwinds. The country's trade surplus, once a pillar of stability, has become a fragile shield against a perfect storm of external shocks. While robust semiconductor exports and a current account surplus of $14.27 billion in June 2025[5] offer temporary relief, deeper vulnerabilities loom. These include a swelling external debt of $735.57 billion as of June 2025[5], a depreciating won, and the Trump administration's demands for $350 billion in U.S.-based investments to offset tariffs[1]. For investors, the question is whether South Korea can navigate these pressures without triggering a crisis akin to its 1997 Asian crisis-era collapse.

Trade Vulnerability: A Double-Edged Sword

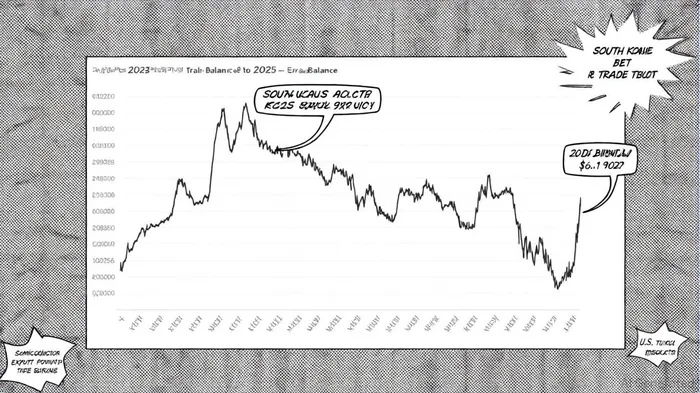

South Korea's trade dynamics in 2025 reflect both resilience and fragility. A 27.1% year-on-year surge in semiconductor exports pushed the trade surplus to $6.51 billion in August[3], while the current account surplus hit a record $14.27 billion in June[5]. Yet these gains mask structural weaknesses. U.S. tariffs on automobiles, steel, and aluminum—key South Korean exports—have eroded competitiveness, with automakers already reporting a six-month decline in U.S. shipments[2]. The OECD now forecasts GDP growth to weaken to 1.0% in 2025[4], down from an average of 2.1% in prior years, as tariff uncertainty deters business investment.

The Trump administration's demand for $350 billion in direct investments to reduce tariffs[1] has further complicated matters. While South Korea agreed to a preliminary deal in July 2025, reducing tariffs from 25% to 15% contingent on investment, the timeline for implementation remains murky. This ambiguity has fueled won volatility, with the currency hitting a 16-year low of 1,487.3 to the dollar in April[2]. The Bank of Korea (BOK) has held its policy rate at 2.75% to stabilize the currency[3], but analysts warn this could exacerbate household debt risks under accommodative conditions.

Fiscal Constraints: A Delicate Juggling Act

South Korea's fiscal strategy in 2025 underscores the tension between stimulus and prudence. The government allocated $467.4 billion in its 2025 budget, prioritizing economic revitalization and national security[3], while projecting a debt-to-GDP ratio of 48.1%[4]. To cushion businesses from tariff shocks, an additional $8.6 billion in emergency spending was proposed[2]. However, these measures risk inflating the national debt to $884.03 billion[4], with the government aiming to keep the fiscal deficit within 3% of GDP by year-end—a target now looking optimistic.

The challenge is compounded by external debt trends. South Korea's external debt rose 9.7% year-on-year to $735.57 billion in June 2025[5], driven by corporate borrowing and foreign portfolio inflows. While the current account surplus and $411.3 billion in foreign exchange reserves as of July 2025[2] provide some buffer, the reserves have fallen to a five-year low, reflecting aggressive market interventions to prop up the won. This depletion raises concerns about South Korea's ability to defend its currency if capital outflows accelerate—a scenario amplified by U.S. monetary policy.

U.S. Monetary Policy and Capital Flow Volatility

The Federal Reserve's tightening cycle has had asymmetric effects on South Korea. Unlike past tightening periods (e.g., 2014–2019), the current cycle has triggered significant capital outflows, with foreign investors reducing exposure to emerging markets, including South Korea[1]. The BOK's reluctance to raise rates aggressively—prioritizing currency stability over inflation control—has exacerbated this trend. While Fitch maintains South Korea's sovereign rating at "AA-" with a stable outlook[3], the agency cautioned that prolonged capital flight or a sharp fiscal deterioration could trigger a downgrade.

Moreover, U.S. monetary policy spillovers are no longer confined to interest rate differentials. Natural rate shocks—driven by structural factors like aging populations and supply chain shifts—have altered transmission channels, making South Korea's export-dependent model more vulnerable[4]. For instance, the Trump administration's "friend-shoring" agenda, which pressures South Korean firms to invest in U.S. manufacturing, risks distorting global supply chains and reducing the efficiency that underpinned Korea's export boom.

Implications for Investors

For investors, South Korea presents a paradox: a high-tech economy with world-leading semiconductor exports, yet exposed to geopolitical and fiscal risks. The country's current account surplus and strong credit rating offer downside protection, but these may not offset the long-term damage from U.S. tariffs and forced capital reallocations. Key risks to monitor include:

1. Won Volatility: A further depreciation could trigger a debt spiral, particularly for firms with high dollar-denominated liabilities.

2. Fiscal Slack: With debt-to-GDP approaching 50%, South Korea's ability to implement countercyclical policies is constrained.

3. Tariff Uncertainty: Delays in tariff reductions or additional U.S. demands could derail the fragile economic recovery.

Conversely, opportunities exist in sectors insulated from U.S. pressures, such as semiconductors and green technology. However, these gains are contingent on South Korea's ability to diversify trade partners and reduce reliance on the U.S. market—a strategic shift that remains untested.

Conclusion

South Korea's 2025 economic narrative is one of resilience under strain. While its trade surplus and fiscal discipline provide a buffer, the interplay of U.S. tariffs, monetary policy spillovers, and political uncertainty creates a high-risk environment. For emerging market investors, the lesson is clear: South Korea's currency and debt risks cannot be viewed in isolation but as part of a broader geopolitical realignment. As the BOK and government navigate this treacherous terrain, the coming months will test whether Korea can maintain its economic equilibrium—or tip into crisis.

Comentarios

Aún no hay comentarios