South Africa's Crisis: A Contrarian's Dream in Mining, Bonds, and Energy

South Africa's economy is in the throes of a perfect storm: a public debt crisis, an energy grid on life support, and a mining sector reeling from load-shedding. Yet beneath the chaos lies a contrarian's playground. For investors willing to stomach near-term volatility, the country's structural advantages—from its critical mineral reserves to its G20-driven reform agenda—could yield outsized returns. Here's why now might be the time to bet against the crowd.

The Crisis Landscape: Debt, Darkness, and Disruption

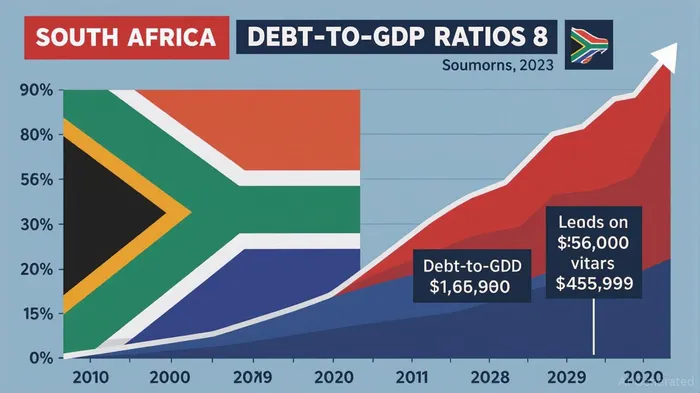

South Africa's gross government debt hit 74% of GDP in 2025, with R385 billion annually siphoned off to service debt—a figure larger than the entire GDP of Kenya.  . The National Treasury's reliance on long-dated inflation-linked bonds (ILBs) to lock in low rates has reduced refinancing risks, but the 10.5% yield on 10-year bonds (vs. 3.8% for U.S. Treasuries) reflects deep-seated skepticism about fiscal sustainability.

. The National Treasury's reliance on long-dated inflation-linked bonds (ILBs) to lock in low rates has reduced refinancing risks, but the 10.5% yield on 10-year bonds (vs. 3.8% for U.S. Treasuries) reflects deep-seated skepticism about fiscal sustainability.

Meanwhile, Eskom's energy crisis has crippled the mining sector. Load-shedding at Stage 6—cutting 6,000 MW from the grid—forced giants like Sibanye-Stillwater and Impala Platinum to halt operations, slashing production and jobs. Yet the government's aggressive reforms—including breaking Eskom into three entities and fast-tracking renewable energy projects—could turn the lights back on by 2026.

The Contrarian Opportunity: Mining as the New Green Gold

South Africa's mining sector is a poster child for value traps turned value plays. The iShares MSCI South Africa ETF (EZA), down 18% in 2025, trades at a 30% discount to its 5-year average price-to-book ratio, with mining stocks like Sibanye-Stillwater (SBGL) and Anglo American (AGL) languishing at multiyear lows. .

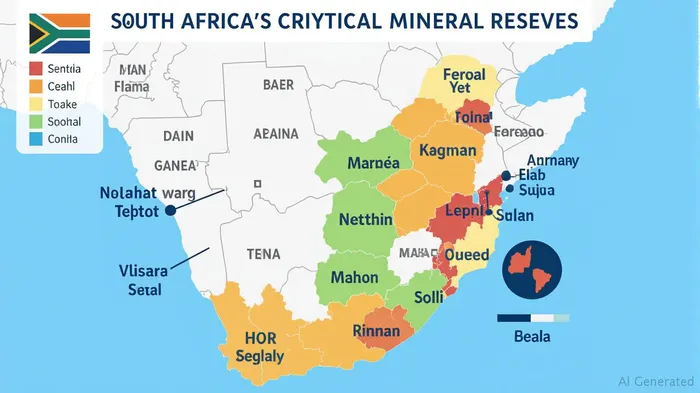

But here's the twist: South Africa sits atop 75% of global platinum group metal (PGM) reserves, critical for hydrogen fuel cells and EV catalytic converters. The government's 2025 Critical Minerals Strategy aims to position the country as a linchpin of the energy transition, with $2.1 billion in pledged FDI for green metals projects. Sibanye-Stillwater, for instance, is investing R4.2 billion in a lithium refining plant—a move that could unlock $10 billion in untapped value from its existing reserves.

The risk? Labor strikes and infrastructure bottlenecks. But with the rand trading at R18.39/USD (up 2% in May) and global PGM prices hitting $1,200/oz, the sector's undiscounted upside—if reforms stick—could easily offset near-term headwinds.

Bonds: A Hedge Against Chaos

For income-seeking contrarians, South Africa's long-dated sovereign bonds (2046–2050) offer a compelling 6.8% yield on inflation-linked securities—a deal in a world where cash earns nothing. . The National Treasury's focus on ultra-long tenors reduces rollover risks, while the July 2025 SARB rate decision (potentially cutting rates below 7%) could boost bond prices further.

The catch? A potential credit downgrade to sub-investment grade. Yet the market already prices in this risk: yields have already surged to reflect a worst-case scenario. For a conservative allocation, pairing 5-year bonds (yield: 9.2%) with puts on the rand could offer asymmetric upside.

The Risks: Politics, Power, and the Rand

No free lunch here. South Africa's 32% unemployment rate and a fracturing coalition government pose existential risks. The Democratic Alliance's threat to withdraw from the National Dialogue could destabilize fiscal plans, while Eskom's R400 billion debt remains a ticking time bomb.

Yet the reform momentum is real. The G20 presidency has given Ramaphosa a platform to push for global financial reforms, including lowering Africa's 500% cost-of-capital premium over multilateral loans. If even half of these initiatives succeed, the risk-reward calculus flips: a 10% rand appreciation or a 200-basis-point bond yield drop would handsomely reward early investors.

Final Call: Go Contrarian, But Stay Cautious

South Africa's crisis is real—but so are its underappreciated assets. For the brave, a 30% allocation to EZA with 20% in long-dated ILBs and 5% in rand puts could form a balanced contrarian portfolio. Focus on companies like Sibanye-Stillwater (exposure to PGMs and lithium) and Eskom's transmission spinoff (when listed), while hedging currency risk.

The key: avoid betting on Ramaphosa's political survival. Instead, bet on South Africa's geopolitical importance as a critical minerals hub and its structural reform tailwinds. The payoff? A country transitioning from crisis to contrarian gold.

.

.

Joe's Bottom Line: South Africa isn't a buy for the faint-hearted. But for investors with a 3–5 year horizon, the asymmetry here is rare: high yields, undervalued miners, and a reform blueprint that could turn the ship around. Just don't blink—this storm won't last forever.

Comentarios

Aún no hay comentarios